Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

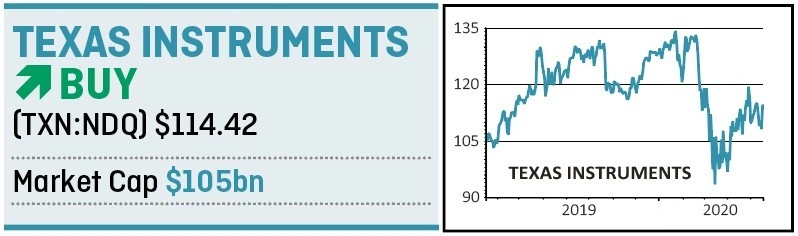

magazineTap into predictable profits from a $105bn electronics giant

A global manufacturer of the very building blocks of electronics and computing, US-listed Texas Instruments is the sort of resilient technology business for a diversified investment portfolio.

The $105bn company has been around since 1951 and is today the world’s largest manufacturer of analog microchips.

These are relatively cheap bits of kit and are vital components in all electronics as they convert real-world signals, such as sound, touch and temperature, into digital.

They are also used for power management, especially useful in batteries for mobile devices. That hints at future growth opportunities as more electronics become mobile.

We’ve already seen how mobile has transformed how we use phones, computers and even vacuum cleaners, and we will see this trend accelerate markedly if the internet of things connectivity takes off. Electric cars are another growth area.

Costing just a few cents per chip, they retain surprising pricing power because they are typically designed into new products. This means supply agreements tend to be for the lifecycle of a product while making customer switching costs prohibitive.

Texas Instruments stands out with its protected analog chip designs and intellectual property, as well as long standing manufacturing expertise. This gives the company a wide and deep economic moat, according to analysts at Morningstar. It already has the broadest range of products and longest list of customers in the industry.

Given the raging Covid-19 pandemic, it is understandable that business this year will be impacted. Earnings per share (EPS) for the year to 31 December 2020 are expected to fall 23% to $4.03. But analysts see a rapid bounce, forecasting EPS of $4.92 in 2021 and $6.55 in 2022.

Investors should be aware that accurate forecasts cannot be relied on right now, given the intense uncertainty around the global economy, but the biggest threat to Texas Instruments remains exposure to the notoriously cyclical chip industry. This will doubtless mean headwinds from time to time although a wider than most customer base and emerging market opportunities should help smooth the cycle.

It has $5.4bn cash, leaving net debt at just $400m. That’s a drop in the ocean for a company that has produced an average $5.5bn of free cash flow in the last three years.

The dividend looks fairly safe. It is expected to pay $3.61 per share this year (paid quarterly), 12% up on 2019, with mid-single digit growth expected beyond. That implies a useful income yield in the region of 3.2%.

The shares are listed on the US Nasdaq market but should be widely available on UK investment platforms.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.