Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy bonds have been #1 this year

Investors have piled into bonds in 2019 at the expense of equities, with more than £8bn inflows into UK bond funds and over £4bn flowing out of equity funds in the first eight months of the year according to the Investment Association. Data from the US show similar patterns.

This might be caused by investors responding to fears about a slowing global economy amid fractious trade talks between the US and China as well as Brexit worries. But some of the trend might also be related to investors chasing performance.

One of the cornerstone assumptions underpinning capital markets is that investors behave rationally to maximise profit. But according to Bloomberg there’s now around $17trn of bonds which, if held to maturity will result in owners losing money.

This fierce inflow of money into bonds has pushed up prices and pulled down yields.

Many investors are buying products where they could lose money if the bonds are held to maturity. They are buying these bonds for capital gains, hoping that the price will keep rising (and yields keep falling) so they can sell for a profit before the bond’s fixed term matures.

In Europe 69% of the €8.18trn Eurozone government bond market has a negative yield (we elaborate on this concept later in the article), up from 40% at the beginning of the year, according to Tradeweb.

Roughly half of the €3.4trn of investment grade corporate debt has a negative yield, up from 12% at the start of the year.

HOW A BOND WORKS

Before we consider what’s going on, it is worth a quick lesson to understand the world of bonds.

A bond is like an ‘IOU’ – a government or company borrows money from an investor by issuing bonds in exchange for cash. They then pay a fixed amount of interest over a specific time period; at maturity the investor cashes in the bond for its original face value (also known as ‘par’).

You often see people discuss bonds in terms of their yields. This can be confusing given that stocks are discussed in terms of share prices. You just need to understand that bond yields move in the opposite direction to the price. So when someone says a bond’s yield is falling, the price is actually rising.

Investors can buy UK government bonds called gilts with various maturities from one year up to 30 years, paying fixed rates of interest (also known as a ‘coupon’). The name ‘gilts’ comes from the fact that the original certificates had gilded edges.

NEGATIVELY YIELDING BONDS

If you buy a bond or gilt that is trading above par there are some important points to consider.

Let’s say you buy at a premium to par at £140. On maturity you will only receive back par at £100 and therefore make a capital loss of 29%.

You need to account for the interest payments received over the life of the bond and if the yearly coupon were 2% that would be equivalent to 20% over a 10-year period.

In this example, even after adding back the interest payments, you would end up with an overall loss which is why this bond example would be called a negatively-yielding bond.

WHY WOULD AN INVESTOR DELIBERATELY LOCK IN A LOSS?

The answer turns out to be more nuanced than one might assume. As incredible as it sounds, it might mean that yields become even more negative (as prices keep going up).

Bond fund manager Mike Riddell of Allianz Global Investors says: ‘Given that a five or 10 year government bond yield is essentially the market’s expectations of where central bank rates are going in the next five or 10 years, then if central banks have further to cut, bond yields can go much more negative, which would give bond investors a capital gain.’

Fund manager Andrew Mulliner at Janus Henderson is thinking along the same lines, commenting: ‘Negatively yielding bonds are not a mystery at all, but a rational consequence of the European Central Bank’s (ECB) negative interest rate policy as well as bank regulation.’

Since the financial crisis in 2008 central banks have embarked on quantitative easing (QE) to alleviate stress in the banking sector. That meant buying government bonds from banks which increased their reserves and encouraging them to make more loans. That was the theory.

The ECB decided it needed to go further and started charging banks that parked excess money with it in the hope that the banks would be incentivised to increase loans and provide credit to the economy.

All of these actions lowered interest rates on everything from mortgages to corporate debt. It also had the effect of pushing up the price of existing government bonds (and pulling down the yield).

BUYING AT ANY PRICE

Since the financial crisis banks have been forced by regulators to hold more capital against their loans, in case they went bad. The banks use a risk-weighted assets calculation to determine how much capital they need, which in turn determines how many loans they can make.

The riskiest assets such as corporate loans carry a higher weighting which increases the amount of regulatory capital that banks have to hold. Importantly, sovereign bonds are considered ‘risk free’. This means that banks can lower their risk capital requirements by simply buying and holding government bonds. In other words, negatively yielding government bonds are very attractive to banks and they are not particularly sensitive to the price they are willing to pay.

Insurance companies are in a similar predicament in that they are mandated to hold enough capital to cover their obligations to policy holders for at least 12 months.

Given that the capital is needed to cover potential liabilities, it is normally held in the safest instruments. You guessed it, they have a preference for high quality, liquid assets and government bonds fit the bill.

Wherever an institution is required by a regulator to hold a minimum amount of capital or collateral, there is a demand for bonds that have a low or zero risk-weighting. This seems perfectly rational from the banks’ and insurance companies’ perspective.

NEGATIVE BONDS AREN’T NECESSARILY CHEAP

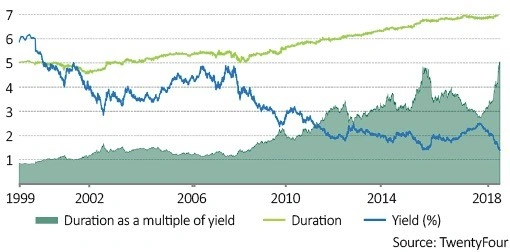

The risk of capital loss increases when yields fall because the price of the bond becomes more sensitive to a rise in interest rates. The blue line on the chart shows the bond yield for the total market. It has fallen from over 6% in 1999 to 1.5%.

The green line is the duration of the market, which is a measure of how long it takes to receive back the capital value of the bond. The lower yields go, the longer it takes to earn back the capital, which increases the duration, as seen on the chart.

The shaded area on the chart is the duration as a multiple of the yield and implies that a 1% move up in interest rates will wipe out the equivalent of five years of interest payments, up from less than one year in 1999.

Chris Bowie, who manages bond portfolios at TwentyFour Asset Management, says ‘the relationship between yield and duration is as stretched as it has ever been, so in terms of the whole bond market things are looking very expensive’.

He adds: ‘In our corporate bond fund, we have more short-dated bonds than the benchmark, which means we have both a higher yield than the benchmark but also a lower duration. In our view this is the best way of producing a quality income without significant capital risks nor capital volatility.’

LOWEST YIELDING CORPORATE BOND EVER RECORDED

This may sound crazy, but central bank policy has distorted corporate credit markets so much that some companies have been able to borrow money for free.

At the end of August industrial conglomerate Siemens borrowed €3.5bn over two to five years by issuing bonds to investors that didn’t pay any interest. You might think logically that demand would be slim. You would be wrong because demand from investors was very strong.

One fund manager even lamented that he didn’t have enough cash at the time to place an order to buy the bond.

His rationale was that paying a company to lend to it for up to five years was a much better proposition than accepting negative yields on German government debt for 30 years. It was simply the ‘least bad option’.

However there is an important difference between lending to Siemens or a large company like Vodafone (VOD) and lending to a government. The UK government, for example, can print money to meet its obligations, whereas a company has to ‘earn’ future cash flows to repay its debts.

In other words, as the name suggests, lending to corporations involves taking on credit risk which makes the activity far more risky.

What are 'payment in kind' notes?

On 25 September luxury car maker Aston Martin Lagonda (AML) issued $150m of debt at an interest rate of 12% plus another $100m which would only be triggered if the company sold at least 1,400 units of its new DBX car in the next year.

What’s different and toxic about these bonds is that half of the interest is deferred until the bonds mature in 2022. These are known as ‘payment in kind’ bonds because the interest isn’t paid each year but added back (as a payment in kind) to the principal loan.

If investors are demanding a 12% interest rate when the overall junk bond market is yielding 2.8%, one has to question the chances that Aston Martin will be able to repay the loan. Worryingly, payment in kind notes were very popular leading up to the 2008 financial crisis.

MINI BUBBLE?...

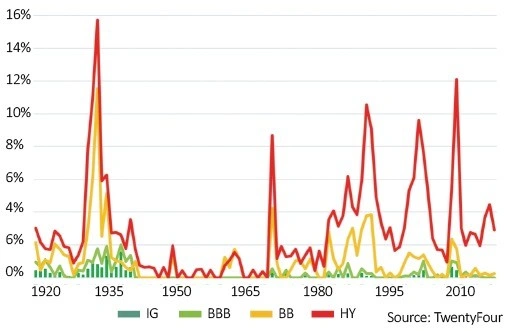

One part of the corporate credit market which receives relatively little attention is the high yield bond market, sometimes known as the junk bond market.

Companies that issue junk debt have a high chance of defaulting on their interest payments and going bust. This reflects a combination of poor business fundamentals and a high cost of servicing debts.

Historical default rates (weighted across the whole high yield universe) were as high as 15.8% during the great depression in the 1930s while in the financial crisis of 2008 they reached 12%.

For comparison high quality investment grade bonds saw less than 2% of companies going bust in the 1930s and even fewer went under, around 1%, during the 2008 banking crisis.

To reflect very high risks of default, junk bonds usually pay a high rate of interest to compensate. Rates were as high as 24% at the height of the financial crisis while 20% yields were on offer during the bursting of the tech bubble in 2001.

Junk bonds have not been immune to the low interest rate environment. Today the interest rate on the Bank of America Euro High Yield index is an incredibly low 2.8%. This level implies there won’t be any future bankruptcies in the high yield market, surely a case of hope over experience. We believe now is not the right time to own high yield bond funds.

PORTFOLIO PROTECTION

One of the historical benefits of owning government bonds is that they tend to move in the opposite direction to stocks, which gives a portfolio some protection when equities fall.

Part of the reason for the so-called ‘uncorrelated’ action is that government bonds are seen as safe relative to equities and in periods of stress investors dump some of their stocks for bonds, pushing up the price of the latter.

The bond fund managers questioned by Shares believe that bonds will continue to offer protection in a falling stock market. That’s partly because governments that have their own currency can print money to pay for its future obligations if required.

This view does present a conundrum in a zero interest rate world because it looks very much like the ‘greater fool theory’ at work.

The idea being that investors don’t really care about the price of an asset because they assume that at some point in the future there will be another investor (fool) willing to pay an even higher price.

That may very well be the case because such a downward spiral in rates and upward spiral in bond prices is potentially infinite. The current mind-set is reflected in how that poor fund manager felt about missing out on buying the negatively yielding Siemens bond.

While bond yields could fall further, boosting prices and flows, given the rising risks it seems prudent to focus on bond funds which have a wider mandate to search out global opportunities and relative value. We suggest you look at Artemis Strategic Bond Fund (B2PLJR1) and M&G Global Macro Bond Fund (B78PH60).

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.