Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow to build a diversified portfolio with just three ETFs

One of the great things about exchange-traded funds (ETFs) is that they are often widely diversified, replicating major indices which consist of many individual securities.

From an investor’s point of view, this means you can hold fewer of them to get a wide-ranging portfolio.

But can you really get enough diversification with just three ETFs? Yes. In fact, some experts say you could even have a well-diversified portfolio with just two products.

TRULY DIVERSIFIED?

First you need to think about what sort of diversification you actually want, and select your funds accordingly, says Vanguard’s head of ETF product management Mark Fitzgerald. ‘If you’re trying to get access to global equities and global bonds, the question is do you want developed and emerging markets, or do you want to span the globe completely?

‘There are number of ways you could go about it but, in theory, an investor could choose two or three ETFs and get most of the exposure they need.’

He points to the Barclays Global Aggregate benchmark which is vast with around 23,700 fixed-income securities, for example, so an ETF tracking that index would offer wide bond market exposure. You could then take a global all-cap approach to equities with something like an ETF-tracking the MSCI World index to get a very broad, highly diversified exposure.

Equities and bonds are not the only asset classes though, so what about alternatives, gold or property? Wouldn’t you miss out on these if you held just a few ETFs in your portfolio? Fitzgerald explains that you would get exposure to these asset classes through the major indices anyway: you might hold stocks or bonds from gold miners, refiners, or even fashion companies that buy gold.

For property, you might have exposure to listed real estate investment trusts, property developers, companies that own airports, even supermarkets such as Tesco (TSCO) which owns a lot of retail space, he says.

PROS AND CONS

So what are the pros and cons of a three-ETF portfolio? ‘Many people own way too many funds’, says Deborah Fuhr, founder and managing partner of research provider ETFGI. ‘Own 10 to 15 active equity mutual funds and you are usually getting less diversification and paying higher fees because many of the funds own the exact same security. So even holding two ETFs could work, you just have to pick the ones that make sense to you.’

She notes a simple bond and equity split in two products would reflect a typical ‘Global Balanced’ portfolio: ‘If you go back in time, one of the most typical portfolios for investors was Global Balanced – just equities and bonds. If you were to buy a global equity ETF and a global bond ETF that would likely deliver better returns than trying to select active managers across the world.

‘So I think it is possible to use a small number of ETFs to deliver a balanced portfolio view.’

Ben Seager-Scott, head of multi-asset funds at financial planner Tilney, says the major advantages of this approach are simplicity, ready diversification, and reducing your rebalancing costs when it’s time to review your asset mix.

However, holding fewer funds means you have less control over your overall exposure compared to a more granular portfolio. ‘The downside is that you can’t control your underlying exposure so you are somewhat constrained by your market-cap weights so you can end up with dominance by individual country, and underlying costs can be higher for large countries than if you bought a set of individual cheaper ETFs,’ he says.

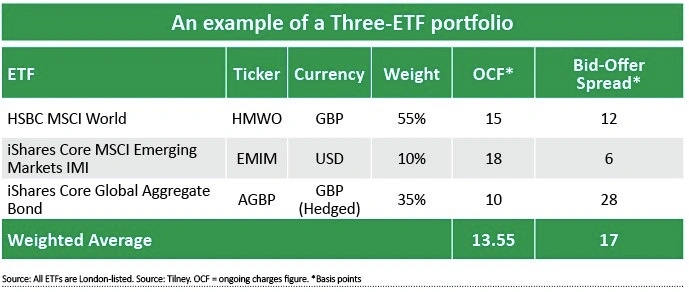

CRUNCHING THE NUMBERS

Let’s compare two model portfolios to see how the costs stack up for a three-ETF portfolio versus a larger one. Here we’ve gone for a 65%/35% split between equities and bonds. We’ve chosen examples of funds following the MSCI World and MSCI Emerging Markets indices for our equity exposure, and for bonds an iShares product which replicates the investment grade Barclays Global Aggregate Bond index.

What we see is that the ongoing charges figure (OCF) or the fees associated with the relevant ETFs are actually two basis points higher on the three-fund portfolio. The bid/offer spread, the difference between the price at which you can buy and sell an ETF, is also slightly higher.

Seager-Scott suggests this is because some of the most liquid ETF regions such as the UK and US have lower costs. ‘The ETFs are very large so you get the benefits of scale and ease of execution. Even though the same constituents are in the global funds, they also have all of the other regions in there as well, and need to be optimised.

‘The ETFs themselves aren’t quite as large, so the result of that greater complexity and being mixed in with other regions makes the weighted average cost slightly higher.’

Although the OCF is higher, where this smaller portfolio would save you money is in trading costs, assuming you review your asset allocation regularly. Rebalancing regularly is important to make sure your risk is in line with your life stage and financial goals.

Most investors pay a flat fee per trade so if, for example, you paid £9.50 per trade and rebalanced your three-ETF selection quarterly, you would pay £114 a year in trading costs, £228 less than you would pay on a nine-ETF portfolio.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.