Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineOur top picks in the UK supermarket sector

While last year saw grocery spending lifted by high temperatures, World Cup fever and a Royal Wedding, the big supermarket chains haven’t had much to celebrate this year with consumer confidence wobbly due to continued Brexit uncertainty and tough comparisons with last year’s sales bonanza.

Yet despite these headwinds, shares in Tesco (TSCO) – the biggest of the three mainstream London-listed supermarkets by market value and by market share, and Shares’ pick of the bunch – have performed well this year, racking up a 26% gain.

The market hasn’t been as kind to Tesco’s rivals, with shares in WM Morrison (MRW) down 8% year-to-date and Sainsbury (SBRY) down 19% after the failure of its planned merger with arch-rival Asda.

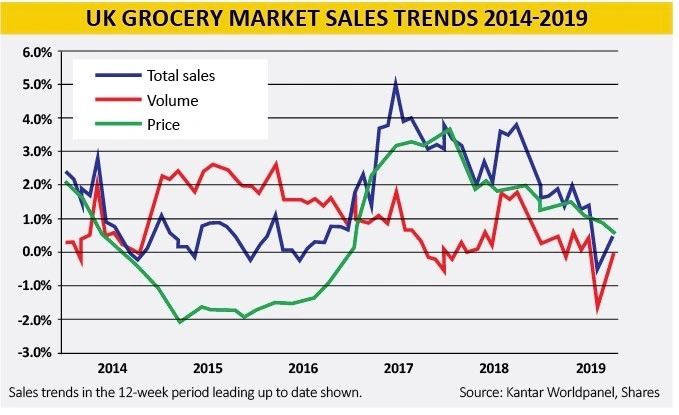

SALES FIGURES SHOW PRICE IS KEY

Shares has analysed the past five years of UK grocery sales figures from market research firm Kantar Worldpanel and a clear trend emerges.

It may seem obvious but the data clearly shows that when grocery prices are falling, volumes tend to increase as we all add a few extra items to our baskets. Conversely when prices consistently rise by 2% to 3% for a sustained period, we tend to buy less.

The ‘golden period’ for UK supermarkets was late 2016 to late 2017, which saw a combination of sharply rising prices after two years of intense competition and average volume growth of around 1%.

At their peak during the summer of 2017 supermarket sales were growing by as much as 5% on an annual basis before continued price increases eventually choked off demand.

Interestingly the spike in sales last summer thanks to the heatwave was driven half by pricing and half by a recovery in volumes as we lapped up as much beer and ice cream as we could to keep cool.

The latest data from Kantar shows total sales by value increased by just 0.5% in the 12 weeks to early September, more in line with the pre-2017 average, with volumes picking up from their recent slump as price increases fade.

WINNERS AND LOSERS

Naturally there are winners and losers in the fight for market share, and the big winners are the German discounters Aldi and Lidl who in the past three years alone have grown their combined market share from 10% to over 14% thanks to aggressive store opening programmes and canny marketing.

To put this in perspective, each 1% increase in market share is worth about £1.2bn in annual sales according to Kantar.

The discounters – or limited-assortment grocery stores as they prefer to be known – successfully shed their ‘down-market’ image some time ago and are seen as combining quality, variety and value, resulting in a steadily rising share of shoppers’ weekly food spend.

They haven’t had it all their own way, however. Although each of the Big Four supermarkets has lost market share in the last three years, figures from Kantar suggest that Sainsbury’s has been particularly effective at fighting back, especially in the run-up to Christmas.

FIGHTING BACK

Following its botched attempt to merge with Asda over the summer, Sainsbury’s has gone back to the drawing board to find ways to win customers both in-store and online in a market with ‘low to no underlying growth’ as chief executive Mike Coupe put it.

Mimicking Tesco, it has reduced its ‘value’, entry-price product range and introduced what it calls ‘owned brands’ like J. James in meat, fish and poultry, and Stanford St in prepared foods, which have much more visual appeal and give the impression of heritage.

This has not only attracted new customers but existing customers are trading up from its ‘commodity’ products, meaning fewer low-value sales.

It has also reined in its level of promotions. According to Kantar, in the year to 8 September just 34% of Sainsbury’s sales were promotional against 40% at Tesco and 45% at Morrisons. Only Asda had a lower percentage of sales from promotions (33%).

While like the rest of the ‘Big Four’ it is gradually losing grocery market share to the discounters, there is still a sizeable ‘pie’ left to squabble over and Sainsbury’s has actually been outperforming its major rivals both in value and volume terms over the past four and 12 week periods.

WHOLESALE AMBITIONS

Tesco has racked up considerable success with its ‘owned brand’ Farm Foods products and its Exclusively at Tesco range with total own-brand grocery sales of £17.7bn in the 12 months to June.

However its attempt to launch its own-brand discount store concept, Jack’s, has been less successful. After a big media launch and a promise to open 10 to 15 outlets by the end of this year, ambitions appear to have been scaled back.

The flagship 40,000 Rawtenstall store is closing and will reopen as a Tesco superstore, while just three new Jack’s are scheduled to open in the next six months. Whether the concept will ever move the needle in terms of contribution to sales is moot.

What has been a big success is the acquisition of the Booker wholesale business, which has taken Tesco into the convenience store and food-on-the-go market. In the first half results to the end of August, virtually all of the sales growth came from Booker.

It’s no surprise that Tesco is pushing further into wholesale with the acquisition of Best Food Logistics. For ‘a nominal consideration’, and subject to review by the competition watchdog, the deal could add £1.1bn of additional foodservice revenues. Best Food customers include sandwich chain Pret a Manger and fast-food stalwarts KFC and Burger King.

ANYTHING YOU CAN DO...

Like Tesco, Morrisons has upped its promotional activity in the retail channel and expanded in the wholesale channel with a raft of new deals this year.

Retail prices were ‘significantly reduced’ on hundreds of lines in the first half and the company says that ‘while this is having a deflationary impact relative to the market we have been pleased with the volume uplift’.

Even with this volume increase, Morrisons’ like-for-like sales in pounds and pence were down 2.4% in the second quarter after a 0.2% gain in the first quarter.

In wholesale, while like-for-like sales were lower than a year ago due to lapping last year’s aggressive roll-out to McColl’s stores, they were at least up by 0.5% in the second quarter.

Wholesale revenues topped £700m in the first half and are ‘on track for £1bn in due course’ thanks to an expansion of the relationships with Amazon and Rontec and a new deal to supply Harvest petrol station forecourt shops.

THE BATTLE MOVES ONLINE

Morrisons’ deal with Amazon allows Prime Now customers to order ‘a full Morrisons shop online’, which is picked in-store then delivered by Amazon drivers with the option of one-hour delivery being rolled out across more major cities.

This brings Morrisons into direct competition with Ocado (OCDO), its former partner in online grocery shopping and the former landlord of its Erith customer fulfilment centre.

For its part Ocado saw close to 10% growth in sales in its first half, but the really big news was the creation of a 50:50 joint venture in grocery with Marks & Spencer (MKS) which comes into operation next year.

M&S has struggled with its own online offering for years and the tie-up with Ocado – where it replaces Waitrose – makes a great deal of sense strategically as the profiles of customers at both firms are very similar. Both are relatively affluent and are willing to pay extra for what they perceive to be good-quality products.

According to market researchers Mintel, online sales of groceries in the UK hit £12.3bn last year, up 9% on the previous year, and are forecast to reach almost £20bn in 2023, a further 60% increase.

While younger customers are happy to shop for groceries online, the big trick for the grocers is to get the older generations, 45 and above, to do their weekly shop online.

Again, given their complementary customer profiles the Ocado-M&S tie-up looks sensible and could see sales grow faster than the overall market if it can succeed in attracting enough older, affluent shoppers.

HOW TO INVEST IN THE SUPERMARKET SECTOR

Five supermarkets are listed on the London Stock Exchange: Tesco, Sainsbury’s, Morrisons, Ocado and Marks & Spencer.

An alternative way to get exposure to the sector is through investment fund Supermarket REIT (SUPR) which invests in UK real estate used to house supermarkets. It makes money by charging rent to tenants which are principally Tesco, Sainsbury’s, Asda and Morrisons.

While there are no investment funds or exchange-traded funds offering a single way to access the operating businesses of the main supermarkets, there are a few funds which have one or more of the UK companies in their top 10 holdings. This would provide exposure as part of a broader diversified portfolio. Examples include (according to data from FE):

Aurora Investment Trust (ARR): 6.76% of its portfolio is in Tesco

TM Sanditon UK (BXRTP05): 4.07% of its portfolio is in Sainsbury’s

Schroder Income (B3PM119): 3.71% of its portfolio is in Morrisons

Baillie Gifford UK Equity Alpha (0585819): 5.00% of its portfolio is in Ocado

RWC UK Equity Income (BG34129): 5.00% of its portfolio is in Marks & Spencer

For investors happy to own individual company shares, our top two picks are Tesco and Ocado.

TESCO

Tesco has the financial might to continue investing in prices if needs be, to see off the threat of the discounters (who are seeing their operating losses mount).

However, if the pricing environment were to improve its market-leading position means it would be the biggest beneficiary of grocery price inflation.

At the same time its diversification into wholesale brings a new customer base and exposure to the food-on-the-go market which is growing faster than its core grocery business.

OCADO

Ocado offers direct exposure to online grocery shopping which is growing faster than in-store sales.

If successfully executed, the joint venture with M&S could see earnings rise faster than the market expects.

However the game-changer is the ‘smart platform’ which provides online retail solutions to six international players including France’s Casino, Australia’s Coles, Kroger of the US and Sobeys of Canada (combined sales last year of over $200bn).

Fees from these and other partners could grow sharply if Ocado’s software is more widely adopted by food and non-food retailers – and that is what the stock market is principally focused on.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.