Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe star performer among Europe-focused investment trusts

Risks to growth across Europe appear skewed to the downside given the impact of global trade-war rhetoric on sectors including autos and industrial chemicals.

However, investors shouldn’t dismiss a select band of niche growth companies making profitable progress under their own steam, yet which just happen to be Europe-based.

Within the investment trusts sector, professionally-managed exposure to this region is offered by the likes of Fidelity European Values (FEV), Henderson European Focus (HEFT) and Jupiter European Opportunities (JEO).

We really like BlackRock Greater Europe Investment Trust (BRGE), the sector’s best one-year performer in share price total return terms, and the second best performer over five and 10 years, according to the AIC.

Since its 2004 launch, BlackRock Greater Europe’s net asset value (NAV) has increased 423.5% (as at 30 June 2019) versus 266.5% for the FTSE World Europe ex-UK index.

And while capital growth is the focus for this fund, BlackRock Greater Europe’s annual distributions have increased every year since inception.

The trust has been co-managed by Stefan Gries since the summer of 2017. Since then, there has been a notable uptick in performance. The German national and fluent Spanish speaker has strengthened the investment philosophy, shifted to higher conviction positions and opportunistically used debt to try and enhance returns.

ONE TRUST, TWO TEAMS

BlackRock Greater Europe offers exposure to high-quality, niche businesses trading at a discount to their estimated intrinsic value.

Gries focuses on companies in developed European markets whereas his colleague Sam Vecht specialises in emerging market opportunities.

‘We think BlackRock Greater Europe is a little bit unique in the sense that it gives you access to two teams that are part of the fundamental equity platform at BlackRock,’ enthuses Gries.

Investing across the market cap spectrum, the trust aims to generate long term capital growth from a relatively concentrated book of 35 to 45 European equities, carefully selected from an investable universe of around 2,000 companies.

Currently there are 34 positions – 30 in the developed European bucket and four in the emerging European bucket – and Gries says his charge is ‘marginally geared’ right now, referring to the use of debt to support further investment in the markets.

WHAT DOES THE TRUST LOOK FOR?

The trust has four primary investment criteria: a quality management team with a record of value creation; a unique aspect such as a product, brand or contract structure; a high and pred ictable return on capital with strong free cash flow conversion, typically a sign of clean accounting; and the ability to invest for future growth.

Companies considered for inclusion undergo thorough fundamental analysis and company management meetings form a key element of the research process. Positions may be sold if the original ‘buy’ thesis no longer holds true, if the investment case has played out or if a superior investment opportunity is identified by stock pickers Gries and Vecht.

Gries’ job is to boil down the investable universe to the most compelling investment cases that Europe has to offer.

He seeks out businesses with characteristics that lend themselves to wealth creation over the medium to long term.

‘We often call them “giants in niches” – businesses operating in a part of the market that is quite “nichey”, where there is a dominant player with high market share and they have pricing power and therefore the returns are shielded.

‘It is very hard to replicate what they do and there is a degree of predictability to what they do. We often find that the true earnings power of these sorts of businesses is underestimated by the market.’

Gries says every time the team look at an idea as a potential new investment, they try to establish if the stock has the qualities to be owned for at least the next three to five years.

He also explains that the majority of the trust’s outperformance has come from stock selection rather than geographic and sector allocation.

WHAT’S IN THE PORTFOLIO?

BlackRock Greater Europe’s portfolio includes enterprise software provider SAP, France-based aerospace manufacturer Safran and German sportswear giant Adidas. It also features investments in Danish insulin maker Novo Nordisk and DSV, a freight forwarding company whose recent acquisition of Swiss logistics rival Panalpina should boost scale in a consolidating industry.

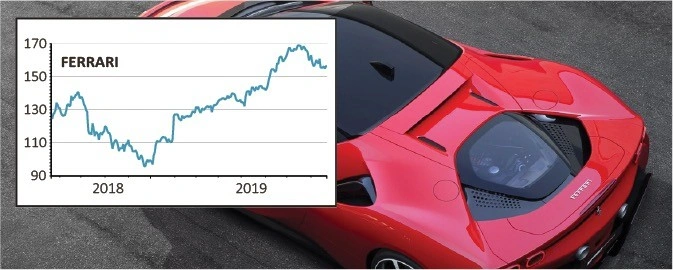

A ‘giants in niches’ example is Ferrari, the Italian sports car maker which has pricing power, expanding profit margins and a growing order book. Gries believes Ferrari’s management have understood brand power and how to create desirability.

The fund manager also hold French spirits producer Remy Cointreau in the portfolio in the belief that its earnings power is underestimated by the wider market.

SHARES SAYS: Buy this investment trust as a way of getting exposure to quality companies in Europe.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.