Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShelter from the storm: 8 funds with reassuring qualities

As investors fret over global trade wars, slowing economic growth, and inverted yield curves, which in the past have signalled recession, it’s worth looking at which investment products might be useful as ‘ports in a storm’ if and when markets decide that the path of least resistance is down.

In theory, absolute return funds should protect your capital better than traditional funds or investment trusts as they have the ability to ‘short’ the market, namely profit when share prices fall. However their recent performance has been unimpressive and investors have been pulling money out of the sector hand over fist all year.

In contrast capital preservation funds have not only lived up to their name in times of market stress but they have delivered astonishingly good returns over long periods and should be high up the list of investor preferences.

In terms of total return, funds which pay out rising dividends also have a role to play and although they haven’t delivered the same gains as capital preservation funds they have still beaten the market handsomely over the long term with no more risk than the benchmark.

ABSOLUTE RETURNS UNDERWHELM

Targeted absolute return funds, which aim to make a positive return in all market conditions, saw a surge in popularity among retail investors in recent years as AJ Bell’s Personal Finance expert Laura Suter explains. ‘Investors flooded into absolute return funds over the past few years driven by worries about global market falls and the ongoing uncertainty over Brexit,’ she says.

After being the best-selling sector in 2015 and 2016, inflows were £7.2bn in the three years to December 2018, taking the total sector size to £72bn according to the Investment Association.

However positive returns aren’t guaranteed, and that was certainly the case in 2018 when the average fund lost 2% after markets went into a tailspin in the final quarter of the year.

In fact their performance has been less than sparkling over the last three years, with an average return for the sector to last December of just 3% or less than half the rate of inflation meaning that investors have lost money in real terms.

As a result, cash has been flowing out of the sector even as flows into UK equity funds have begun to increase for the first time in years.

INVESTORS VOTING WITH THEIR FEET

Many absolute return funds use different benchmarks to mainstream funds and their asset allocation is at the manager’s discretion which, when added to the use of derivatives, means investors are sometimes hard-pressed to understand what the managers are doing.

Standard Life Aberdeen’s GARS or Global Absolute Return Strategies (B7K3T22) was the pioneer in the sector. Launched in 2008, and run by a team of managers with allocations to specific areas of the bond and equity markets, it aims to deliver a positive return in all market conditions and no less than 5% above the return on cash every year over any three-year period.

However, returns over one year, three years and five years are 3.6%, 2.5% and 4.2% according to FE Trustnet, and investors have withdrawn close to £10bn in the last 12 months, cutting assets under management to less than £8bn.

Problems at asset manager GAM related to the suspension of a star fund manager have seen the firm liquidate several of its absolute return bond funds, while the Merian Global Equity Absolute Return Fund (BLP5S80) has seen outflows of £4bn in the last year due to a one-year performance of -9.6% and a three-year performance of -0.9% according to FE Trustnet.

To be fair there have been winners in the sector. Polar Capital UK Absolute Equity Fund (BQLDRR5) has returned 3.3% over one year and 53% over three years, while the Schroder UK Dynamic Absolute Return Fund (B3N5347) is flat over one year and up 20% over three years.

Sadly these are outliers and although they are seeing inflows, the sector as a whole hasn’t covered itself in glory, especially in the final quarter of last year when absolute return as a strategy ought to have distinguished itself.

Finally, AJ Bell’s head of active portfolios Ryan Hughes warns that although absolute return funds such as Polar’s look good on paper, they may not suit everyone. ‘Polar Absolute Return takes excessive risk, has suffered big drawdowns and is more volatile than the FTSE All-Share,’ he adds.

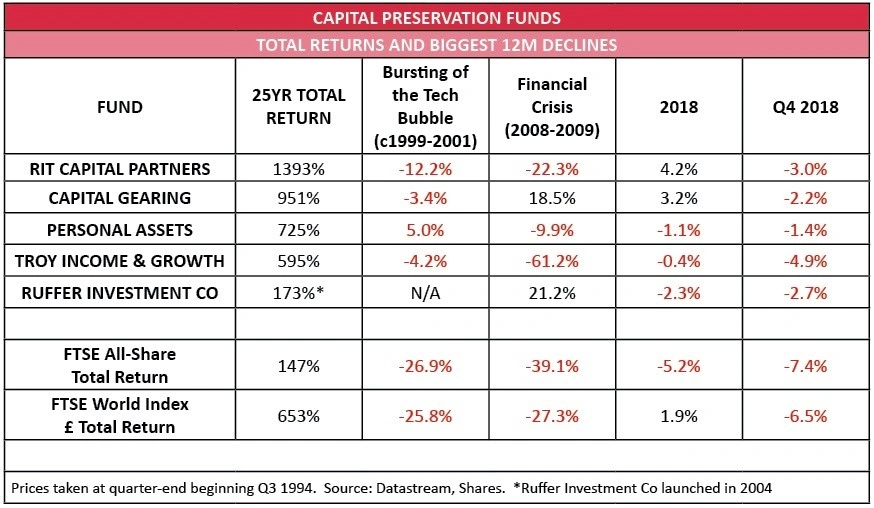

CAPITAL PRESERVATION TICKS THE BOX

One sector which held its own in the last quarter of 2018 was capital preservation funds, which as the name implies prioritise avoiding loss of capital.

They tend to invest in a broad spread of assets other than shares, including privately-owned companies, which means that their performance is less correlated with the stock market.

When markets roar ahead they may not keep up with the broad stock market indices, but typically they should fall less during a downturn sheltering your investment.

The average total return for the five capital preservation funds we follow most closely was -2.8% in the final quarter of 2018 compared with a 7.8% loss for the FSTE 100 index, so they did their job.

They also beat the market on average over the course of 2018 with two funds making a positive total return. Capital Gearing (CGT) added 3.2% last year while RIT Capital Partners (RCP) added 4.2% compared with a 5.2% loss for the FTSE All-Share Total Return Index.

With four out of five funds having been around since the early 1980s or longer, we have measured their performance over 25 years to take into account more than one market cycle.

Despite suffering drawdowns after the bursting of the ‘tech bubble’ in 2000 and/or in the global financial crisis in 2008, their performance was nowhere near as bad as the benchmarks and over the long term has been truly impressive as the table below shows.

RIT Capital Partners has generated the highest total return at just under 1,400% over the past 25 years, followed by Capital Gearing with 951% and Personal Assets Trust (PNL) with 725%. All three outperformed the index in 2000 and again in 2008 with shares in Capital Gearing actually gaining over 18%.

The ability of these funds to generate significantly above-average returns with significantly below-average declines when the market gets the wobbles should have investors queuing up to put money in if the outlook for stocks does worsen in the next year or two.

Troy Income & Growth (TIGT) performed well in 2000 but the shares had a howler in 2008, losing 61% of their value while the worst 12-month return for the FTSE All-Share Total Return Index

was -39% and for the FTSE World £ Total Return Index it was -27%.

In Troy’s defence it was only appointed manager of the trust in 2009, taking over from Aberdeen Fund Managers as it was at the time. Since taking control, the team at Troy has generated a four-fold total return for shareholders.

Newcomer Ruffer Investment Company (RICA), which was launched in 2004 and therefore only has a 15-year track record, was actually the best performer during the financial crisis adding 21.2% in the 12 months to March 2009. It also beat the market in final quarter of last year.

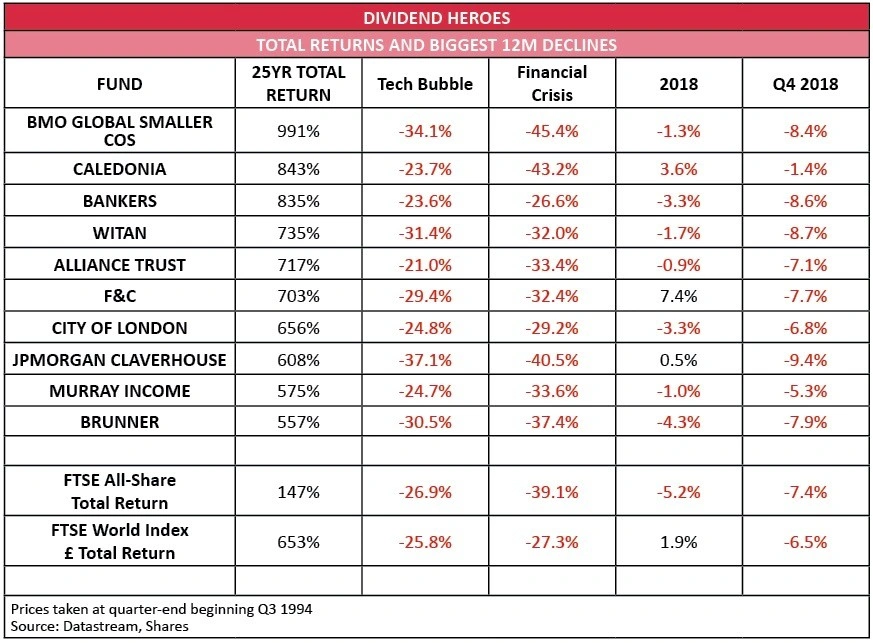

RISING DIVIDENDS OFFER PROTECTION

A key element of the total return calculation is dividends as a steadily rising income stream can help mitigate falls in share prices.

Using data from the Association of Investment Companies, we have tracked the total return of the 10 most seasoned ‘Dividend Heroes’ or trusts which have raised their pay-out for 20 or more years consecutively.

Three of them, Alliance Trust (ATST), Bankers (BNKR) and City of London (CTY), have raised their dividend each year for the last 52 years. The first two were founded in 1888 and the third in 1891 so they have serious pedigree.

The oldest investment trust, F&C (FCIT), was launched in 1868 and last year raised its dividend for the 48th consecutive year.

The average total return of all 10 funds over the last 25 years, including reinvested dividends, is 746% with a range of 575% to 1,046%.

Investment trusts are allowed to set aside up to 15% of their earnings each year which they can add to reserves. As Nick Britton of the AIC explains, this discipline of ‘counter-cyclical’ provisioning for the future is key to the trusts’ ability to keep increasing their dividends even when markets are in turmoil.

‘The ability of investment companies to retain some of their income in good years to supplement their dividends in leaner ones means that even through such intense market downturns as the bursting of the tech bubble and the global financial crisis, investors in any of the dividend heroes would have seen their dividends continue to increase year-on-year.’

For most of the 10 funds, around half of the total return over the last 25 years has come from reinvested dividends. It’s worth noting there are a couple of outliers: for BMO Global Smaller Companies (BGSC), dividends represented just 30% of the total return, while for City of London and Murray Income (MUT) it was closer to 70% of the total return.

TRADE-OFF BETWEEN RETURN AND RISK

As with the capital preservation funds, we examined the performance of the Dividend Heroes post the tech bubble, during the global financial crisis and over the course of 2018, and measured their maximum 12-month decline. This exercise shows that higher total returns typically come with higher risk.

BMO Global Smaller Companies has the best total return over the past 25 years, which mostly come from capital appreciation rather than dividends. However its small-company bias means that in times of market stress losses can be much higher than the benchmark or the rest of the sector, as the table shows.

Meanwhile Caledonia (CLDN), which has the second-best return, invests mainly in unquoted companies and private equity funds meaning that valuations are based on prices determined by financial models rather than on a widely available market price.

Its performance during the financial crisis was also significantly worse than the market and its peers. Many private equity trusts came under severe pressure during the crisis due to the fact that although valuations were falling they had to honour their commitments to continue funding their investments.

With the current concerns over liquidity in unquoted companies raised by issues at Woodford Equity Income Fund (BLRZQ62), we would question whether now is the time for retail investors to be taking on this kind of exposure, although the private equity sector has learned from past mistakes and such forward funding commitments are less prevalent.

Two trusts which have generated significant outperformance versus the benchmark but didn’t suffer unduly large 12-month declines or disgrace themselves last year are Alliance Trust and Bankers.

These two look to have an acceptable level of risk for the returns they are capable of generating, and reassuringly in both cases roughly half of the returns have come from reinvested dividends and half from capital appreciation.

Investors should note that good historical data doesn’t guarantee a fund will continue to do well in the future, so don’t buy a trust simply based on how it has done in the past expecting similar returns in the future. However, it is still important to consider past performance as it provides proof of how well a fund has done in both good and bad times.

We believe both Alliance Trust and Bankers are worth buying as they provide diversified global exposure in a careful, considered manner. We also favour Capital Gearing, Personal Assets and RIT Capital Partners among the capital preservation funds. Furthermore, we believe F&C, Witan and JPMorgan Claverhouse (JCH) are among the standout investment trusts classified as Dividend Heroes.

WANT MORE INFO ON OUR TOP PICKS?

Click on these links to read more detailed articles on the following trusts.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.