Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSeven trusts on bargain ratings: which ones to buy?

We’ve spotted quite a few investment trusts trading at unusually large discounts to net asset value (NAV). There are good reasons why some of them are out of favour. Other situations are more perplexing which suggests investors could potentially snag themselves a bargain if we assume the discount could revert back to normal levels or even disappear.

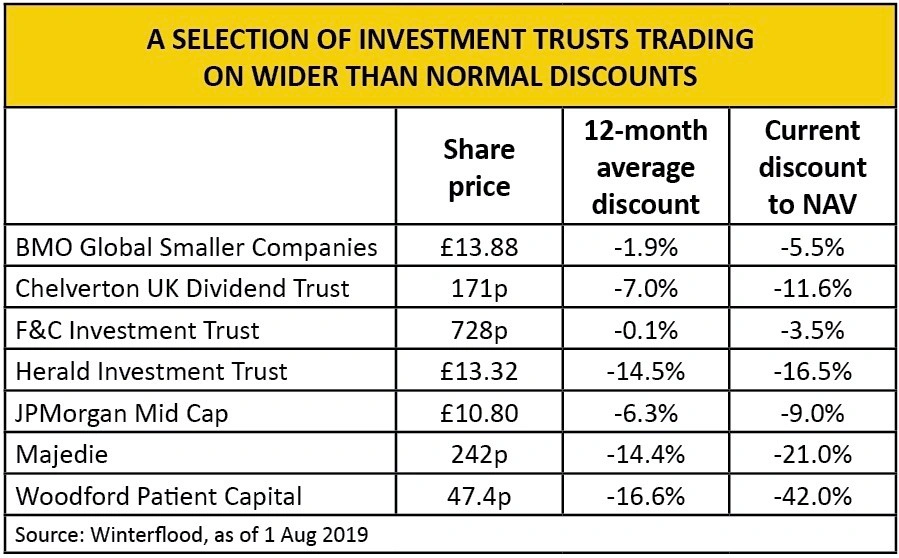

The list includes BMO Global Smaller Companies (BGSC), F&C Investment Trust (FCIT), JPMorgan Mid Cap (JMF) and Woodford Patient Capital (WPCT).

MONITORING PREMIUMS AND DISCOUNTS

Many investors monitor premiums and discounts to NAV very closely as a way of spotting if there is an opportunity to buy something cheaper than the value of its underlying assets, or sell a trust if the market is overpricing it.

We’ve used data from Winterflood to look at the average discount to NAV over the past 12 months and then compared it to the share price

on 1 August.

In the global sector, the one that really stands out is Majedie (MAJE) which at 242p is trading on a 21% discount to NAV versus a 12-month average of 14.4%. It obtains exposure to listed companies around the world by investing in various funds managed by Majedie Asset Management. Just over a quarter (27.5%) of its assets are accounted for by its stake in the aforementioned asset management business.

‘Majedie is an outlier in the global market,’ says James Carthew, head of investment company research at QuotedData. ‘There is quite a big family holding in the trust and its shares don’t trade much, plus people don’t know it very well. It is the worst performing global trust over the past year and the wider discount would suggest people are voting with their feet.’

Thomas McMahon, analyst at research group Kepler, says there were fears last year of a share overhang with the possibility of shareholder Aviva (AV.) exiting Majedie along with a number of other trusts, although he says this seems to have subsided.

He views the current discount to NAV as ‘a potentially interesting way to play the undervaluation of UK equities while gaining diversified exposure to global equities’.

Weighing up discounts: What to consider

1. What’s caused the NAV discount to widen? Read the latest fund manager commentary for guidance on performance.

2. How often is the NAV updated? Be aware if you are comparing the latest share price with assets valued months ago. Ideally you’d want to compare against NAV taken on the same day, or the day before. Unfortunately some trusts don’t provide regular NAV data.

3. Do you believe the stated NAV? Some unquoted assets may be conservatively valued in the accounts and actually worth a lot more. The opposite can also apply.

WE PREFER THIS UK-FOCUSED PRODUCT

More interesting to us is JPMorgan Mid Cap which at £10.80 is trading on a 9% discount to NAV versus a 12-month average of 6.3%.

A falling pound and fears over a no-deal Brexit will have hurt sentiment towards UK domestic stocks and by default the JPMorgan fund which has a big focus on UK-focused FTSE 250 companies.

We think the trust is worth buying at the current price in the belief that clarity over how Brexit will play out will encourage a bounce in UK equities as the ‘uncertainty’ factor is removed. However, anyone buying the shares could be in for a bumpy ride in the near term.

The portfolio includes specialist retailer Games Workshop (GAW) and paving stone maker Marshalls (MSLH), as well as some more international names like construction equipment rental expert Ashtead (AHT) and transport hub food and drink seller SSP (SSPG).

‘A change of broker in June 2019 is intended to help support marketing efforts to narrow JPMorgan Mid Cap’s discount to NAV, although we understand that the board’s reticence to use buybacks to this end reflects its belief that while the Brexit negotiations are ongoing, the UK is likely to remain out of favour,’ says McMahon at Kepler.

SMALL CAP STRUGGLES

BMO Global Smaller Companies has averaged 1.9% discount to NAV over the past year and has occasionally traded on a premium of up to 3.2% over this period. However, at £13.88 it is now trading on a 5.5% discount, perhaps because it had a bad time in June with quite of few of its holdings issuing bad news including chemicals group Scapa (SCPA:AIM) and retailers Home Group and Ted Baker (TED).

‘People are starting to get concerned that we are near the end of the economic cycle,’ says Carthew at QuotedData. ‘If you think this is true, small caps are among the things that tend not to do as well in a recession.’

Also out of favour in the small cap world is Chelverton UK Dividend Trust (SDV) which has gone from trading at a small premium in the past year to now trading at an 11.6% discount versus a 12-month average of 7%. Admittedly the discount has been as wide as 16.4% in the past year.

It looks for ‘dull but worthy’ companies which it believes are ignored by brokers and other fund managers. The trust is fairly small and so liquidity could be an issue.

Another small cap trust to trade on a wider-than-normal discount is Herald Investment Trust (HRI), a tech fund run by Katie Potts. At £13.32 it is trading 16.5% below the value of its underlying assets versus a 12 month average of 14.5%.

We believe there are better funds to play the tech theme as Herald is restricted by only focusing on the UK and in the smaller end of the market. However, Carthew is more optimistic, saying: ‘Herald hasn’t kept pace with large cap US tech stuff, but the numbers have been pretty good and the trust deserves a better rating’.

Lower premiums than normal

Some trusts regularly trade at a premium to NAV and occasionally that premium will narrow or disappear. The best current example is Lindsell Train Investment

Trust (LTI) which has gone from an incredible 100% premium to NAV earlier this year to now ‘only’ having a 31.8% premium. To put that into perspective, the 12 month average is 63.2%.

As you can see from the chart, its shares recently plummeted after investment platform Hargreaves Lansdown (HL.) removed the trust from its best-buy list to avoid any conflicts of interest. The trust has a big stake in Hargreaves. Some investors may have been spooked by losing the best-buy accolade and sold out.

WOODFORD FUND SINKING FAST

Woodford Patient Capital Trust has sunk to a 42% discount to NAV (versus 16.6% average over the past year) as the multitude of problems weighing on its asset manager have left the fund very unloved.

There is a crossover of holdings with Woodford Equity Income Fund (BLRZQ73) which is selling off assets as part of a restructuring away from illiquid investments. The market anticipates it won’t get a fair price and that is affecting the valuation of many holdings. The investment trust is also taking action to reduce debt which means selling some of its own holdings.

‘There is a clear risk that Woodford Patient Capital will have to sell the more mature assets, and these could well be at a material discount to carrying value,’ says Investec analyst Alan Brierley.

We think there is a risk of further downside for the trust so wouldn’t suggest buying it at present despite the apparent value opportunity.

Instead, we suggest you look at F&C Investment Trust whose shares at 728p represent a 3.5% discount to NAV. This trust normally trades exactly in line with the value of the underlying holdings, so now is a good time to buy. It is a multi-manager fund offering exposure to assets around the world.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.