Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

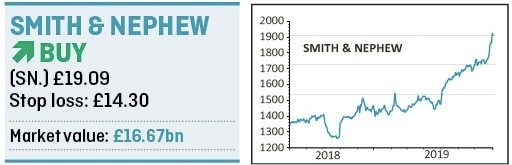

magazineBuy Smith & Nephew as the FTSE 100 company is finally going places

Diversified medical devices maker Smith & Nephew (SN.) operates in growth markets and owns very competitive products, putting it in an enviable market position.

What’s let shareholders down in the past has been business execution and a failure to exploit the growth opportunity. That is now changing.

The shares aren’t cheap on 21.4 times forecast earnings, yet we feel there is a good chance that earnings are now in an upgrade trend which should fuel interest in the stock.

New chief executive Namal Nawana came aboard in May 2018 and has since radically altered the culture of the company, which culminated in re-organising the business into three global franchises: orthopaedics, sports medicine and advanced wound management.

This simplified structure has reduced duplication of effort and made reporting responsibilities clearer with better accountability. The company is now is a better position to leverage its end-markets and product portfolio.

MORE ATTRACTIVE NUMBERS

The recent half year results gave a glimpse of the potential financial benefits of a sharpened commercial focus. The company reported underlying revenue growth of 3.9% and a higher operating margin, up 60 basis points to 21.4%.

Accompanying the positive update was an upgraded guidance for revenue growth of half a percent to 3% to 4%.

Other fund managers have spotted the opportunity for the company to maximise its potential, including Stephen Yiu of Blue Whale, who told Shares in March that ‘expectations are pretty low, the medtech business is fairly high quality and corporate optionality via M&A is high’.

THREE GLOBAL FRANCHISES

Orthopaedics is the largest franchise, representing 44% of revenue. It essentially involves making replacement hips and knees. Every year over 2m patients receive total or partial replacements. The hip and knee market is thought to be worth $14.5bn, and four players control 86% of the total market, making it relatively consolidated.

Smith & Nephew has a 12% share behind Stryker, Johnson and Johnson and market leader Zimmer Biomet with 33%.

There is a smaller market outside the replacement market related to treating people who have suffered bone fractures, and in this segment the company supplies various plates, screws, rods and nails.

In addition there is a market for treating deformities. These two markets were worth $6bn according to the company.

Johnson & Johnson and Stryker have a combined 70% share, while Smith & Nephew has 8% and Zimmer Biomet has 11%.

The company has competitive and innovative hip products, for example its knee technology system is unique and the only one with a 30 year wear performance claim that has been approved by the FDA (US Food & Drug Administration).

Recent data showed that patients implanted with its proprietary hip technology demonstrated lower readmission rates in the first 90 days after the operation, while cutting post-operative care costs by 10%.

TREATING SPORTS INJURIES

The second largest franchise is sports medicine and football

fans will be familiar with some of the products that make up this $5bn market. They include cruciate ligament ruptures and meniscal tears, which seem to have become more common since football boots have become less sturdy.

The company produces implants to treat such injuries as well as mechanical devices and radiofrequency machines used to repair soft tissue around joints. The four top players control around 81% of the market with Smith & Nephew holding 26%, just behind leader Arthrex.

The market for repair products is growing strongly, with the key driver being an increasingly active older population and rising obesity. Think of slightly overweight 40-something’s taking their sports activity a little too seriously.

The World Health Organisation (WHO) says that obesity has tripled since 1975, and is a major risk factor for contracting diseases such as diabetes and joint problems.

Sedentary lifestyles may lead to an even greater incidence of diabetes and related health conditions that will support demand for the company’s products.

OTHER AREAS OF EXPERTISE

Advanced wound management is the company’s third global franchise and is estimated to be worth $9bn. The company makes various dressings, tropical treatments and devices used to manage wounds.

One of the more interesting segments is the active healing or bioactives market. Wound bioactives are materials which have intrinsic healing properties that release antibodies, antiseptics, plant extracts or insulin in order to aid the healing process.

This segment is estimated to be growing 10% annually and has a potential revenue value of around $1bn. As might be expected for a market in the early stages of growth, it is relatively fragmented with lots of different players.

FINANCIAL AND OPERATING LEVERAGE

A feature often overlooked by investors is operating leverage. Theoretically Smith & Nephew’s profit should grow by a greater amount than revenue due to its high fixed costs.

Broker Berenberg’s base case is for 4.9% compound annual growth rate (CAGR) in revenues for the next five years, but this translates into 12.8% CAGR in operating profits, due to the operating leverage effect.

Nawana has stated that he would like to make further acquisitions in faster growing areas and is targeting 2.0 to 2.5 times net debt-to-earnings before interest, depreciation and amortisation (EBITDA) in order to achieve it. This implies $1.5bn of headroom to make further deals.

Berenberg thinks the market hasn’t fully appreciated the financial benefits that future acquisitions could bring to shareholders. On top of this, the company has said that it will return excess cash to shareholders via share buybacks, boosting earnings per share.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.