Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineA differentiated way to play the healthcare space

There are many reasons why investors are attracted to the healthcare space including the chance to back companies which are making a big change to people’s lives as well as finding the next wonder drug and potentially enjoying large profits from its commercialisation.

Investing in this space can be very risky as it can take companies many years to put their drugs through trials to get them approve, and that costs money and no promise of success. As such, we believe it is important to only back companies with lots of products so you enjoy diversification benefits. An alternative is to use a fund with stakes in multiple healthcare companies.

International Biotechnology Trust (IBT) is one of the funds that stands out from the crowd. It has been managed by SV Health Managers since 2001, one of the world’s leading life science investors.

The managers believe the biotech sector is currently undervalued as expressed through a forward price-to-earnings ratio of 9.9-times, the lowest rating since 2009.

HOW IT DIFFERS FROM THE REST

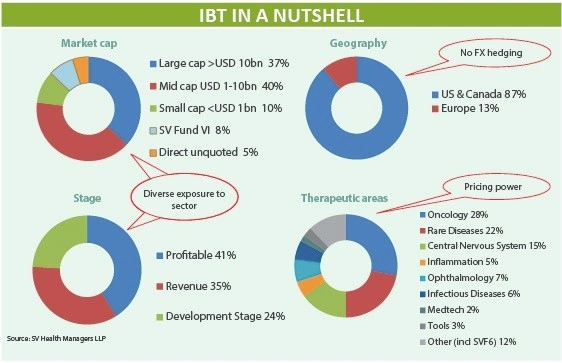

International Biotechnology Trust has a differentiated approach from most of its rivals. Given the risky nature of the sector, the managers employ some interesting risk mitigation techniques to reduce the volatility and risk of the portfolio.

For example the managers deliberately tilt the portfolio towards research areas that have demonstrated pricing power, such as oncology (cancer), rare diseases and the central nervous system.

In aggregate two thirds of the portfolio is exposed to segments with pricing power, giving the fund protection against possible future regulatory pressure.

Most of the companies in the portfolio generate revenue and make a profit, while only 24% are early stage, developmental businesses.

Another interesting risk mitigation tactic used by the managers is that they actively reduce their holdings in companies which have ‘event risk’ related to the results of clinical trials. The team acknowledges that they would be competing with specialist hedge funds that speculate on the success or otherwise of a binary event.

The managers will look to increase exposure again once the results of the trial are known and assuming the investment case and valuation still stack up.

HOW DOES IT PICK STOCKS?

International Biotechnology Trust has access to a panel of specialists, who are used not for medical opinions, but for their statistical expertise and analysis of how patient studies should be conducted. The idea is to get an understanding of how the US Food & Drug Administration (FDA) thinks and the chances of approval.

The team conduct their own discounted cash flow analysis as a sense check on valuations of companies in the portfolio, lightening up when shares have ‘run ahead’ of the fundamentals.

Finally, the managers can draw upon the experience of the wider SV Health group which manages $2.9bn of assets across seven private venture capital funds and boasts a 25 year track record.

US HEALTHCARE DEBATE

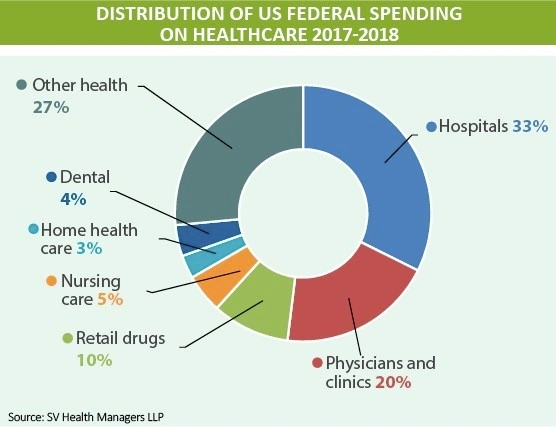

Some 87% of the portfolio is exposed to the US and the healthcare debate will be a key issue in the 2020 elections. Prescription drugs represent only 10% of health spending in the US, while the real problem area is the intermediaries that take around 41% of the spending.

If reform to the US system is forthcoming then intermediaries are likely to be the hardest hit, while innovative companies will face far less disruption to their business models.

The manager believes that innovative drugs that address unmet medical needs will continue to command premium prices which explains the current portfolio positioning.

GROWTH DRIVERS

International Biotechnology Trust believes the factors driving growth in the sector are not sensitive to economic cycles and are able to withstand medium-term political challenges.

Populations are expected to grow by a third to 9.7bn by 2050, which would imply an ‘elderly’ population of 2.1bn people, all of which would result in increased healthcare demand.

Elderly people account for disproportionately high healthcare spending and drug companies are developing more drugs to keep pace.

In an effort to encourage more innovation the FDA has streamlined the approval process including fast-tracking certain drugs. Evidence of this can be seen in the rising trend of approvals, which reached 59 in 2018, up from 20 in 2010.

SHARES SAYS: We rate this investment trust as a good way to play the healthcare space. It has a very impressive track record and has delivered a five-year cumulative return in net asset value (NAV) of 96.8% compared to 70% for the Nasdaq Biotechnology Index and 29.3% for the FTSE All-Share.

The trust is unusual in that it pays a dividend equal to 4% of the NAV, a policy introduced in 2016 in an attempt to narrow the discount. Prior to this the shares traded at a consistent discount to NAV despite share buybacks.

The cash comes from the capital value of the fund, rather than dividends paid by companies inside the fund. The idea is to pay a fixed percentage of the value of the fund, which means that the actual cash paid will move up or down in line with the NAV. The team expect the long-term capital growth rate to average around 10% per year.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.