Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSirius, Shell, the banks and other big news

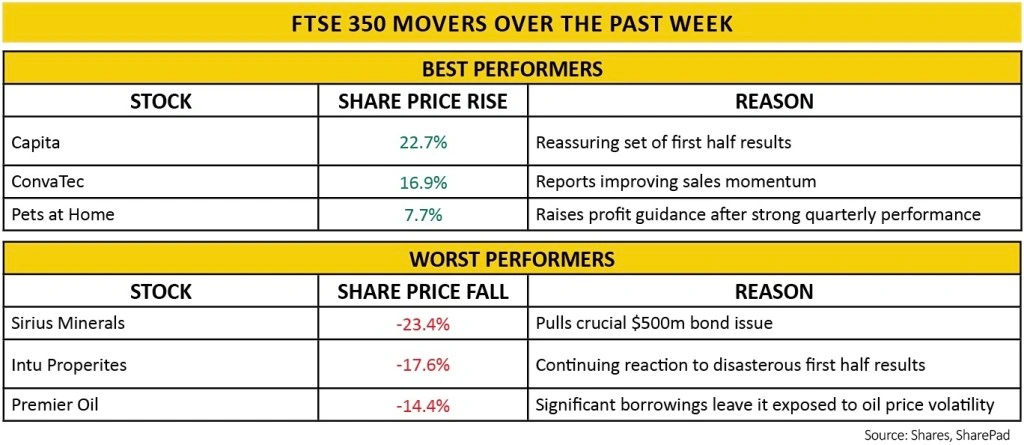

Negative news from Sirius Minerals (SXX) on 6 August was a source of particular disappointment for Shares as we had highlighted the stock as being undervalued in a recent article.

By pulling a $500m bond issue due to ‘current market conditions’ Sirius has raised serious questions about the viability of its potash project in Yorkshire.

Securing these funds by the end of September is a crucial term and condition of getting the additional $2.5bn in lending via a revolving credit facility (RCF) that JPMorgan will initially provide, which in turn is vital to being able to build the mine.

The company says it will make another attempt to get its debt away later in this quarter, but investors appeared unconvinced, with the shares losing more than a quarter of their value to trade at 10.8p in the immediate aftermath of the revelation.

On 1 August Royal Dutch Shell (RDSB) disappointed heavily with its second quarter numbers with profit around $1bn below market expectations.

This was the biggest miss the company had posted since 2016 when oil prices were in sharp decline. Shell was hit by oversupply in the natural gas market, a key area of focus for the business, as well as economic uncertainty.

The exit of Domino’s Pizza (DOM) boss David Wild (6 Aug) was initially received positively by the market following a period of turmoil for the company, the shares rising to 254p.

The announcement accompanied a mixed set of first half results, with the company continuing to be beset by disputes with franchisees and teething problems with its international expansion plan.

Banks can't escape PPI

The UK high-street banks have little to cheer about so far this year. Their first half results all showed a similar trend, with a ‘challenging income environment’ according to Barclays (BARC).

Continued margin pressure in mortgage lending meant the banks had to fall back on cost cutting. Even Lloyds (LLOY), which already has the lowest cost-to-income ratio, is aiming to cut costs further.

On the plus side bad loans are still at historically low levels, around 0.2% to 0.25% (0.9% for credit card lending), but provisions are starting to creep up, so the low point of the cycle looks to have passed.

At the same time, PPI charges – which were expected to tail off by now – are actually increasing ahead of the 31 August claims deadline.

Even after the deadline, the backlog of claims could still be in the millions according to Guy Wakeley, chief executive of Equiniti (EQN) which helps the banks deal with reparations.

On 5 August HSBC (HSBA) announced numbers which were slightly ahead of expectations, but this news was overshadowed by the surprise departure of chief executive John Flint less than two years into the job.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.