Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineMounting debt haunts rate cut bonanza

One of the most stunning aspects of the financial markets in 2019 is the U-turn in monetary policy across the world’s leading central banks.

The Federal Reserve started the trend on 4 January when chair Jay Powell strongly hinted that the American central bank’s previously metronomic, quarterly increases in headline borrowing costs would come to end this year and that the sterilisation of quantitative easing (QE) would stop in the autumn.

Powell and his colleagues on the Federal Open Markets Committee have since gone further and put interest rates reductions so clearly on the agenda that the debate has shifted on to how fast and how deep those cuts will go.

Even if it does not cut rates today (25 July) the European Central Bank (ECB) is expected to lay the groundwork for reductions in its headline deposit and refinancing rates, as well as possibly a resumption of its QE scheme, barely eight months after ECB chief Mario Draghi had announced a halt.

Financial markets currently seem happy with the prospect of this largesse. Bond markets are rallying because more QE will mean more price-insensitive buying of fixed-income instruments by central banks.

This will also likely serve to drive down yields on future issuance and make the yields available on currently-traded paper look more attractive on a relative basis.

Equity markets are rallying because lower returns on cash and falling bond yields may revive the ‘There Is No Alternative (TINA)’ argument for stocks, or in other words the offerings from bonds and other assets are so paltry, equities are the only option, especially for those investors who are hungrily seeking income.

Yet perhaps people need to ask themselves why central banks are returning to their bags of monetary policy tricks and what potential risks lie ahead, as well as the rewards that may be accrued.

About turn

According to the website cbrates.com we have had over 40 central bank rate cuts this year – with Russia, Korea, South Africa, India, Australia and New Zealand leading the way – against just 10 increases, with Norway the most prominent exponent of tighter monetary policy.

That compares to 89 increases and 47 cuts last year so the tide has turned, especially as the Fed, ECB and also Turkey have set out their stall when it comes to plans for cutting the cost of borrowing.

Perhaps markets could have seen this coming. After all, we have been here before. A succession of central banks in developed markets – Australia, Canada, Israel, New Zealand and Sweden, as well as the EU – all raised interest rates at the start of this decade. Each nation’s central bank had to quickly back-pedal and New Zealand even had another go at normalising policy without success in 2014-15.

The sextet of central banks quickly changed their minds as their currencies and borrowing costs for consumers and corporates (and governments) crimped spending, with the result that their economies slowed. It simply proved harder to move away from record-low interest rates than they had thought and central bankers have apparently come up against the same problem again in 2019.

Caught in a trap

If anything, it could be even harder to normalise interest rates now than seven or eight years ago, because global indebtedness is so much higher and no-one seems to want a strong currency (which may be why gold is back on the march).

The irony is that borrowing is higher because central banks have encouraged it, with lower interest rates and QE.

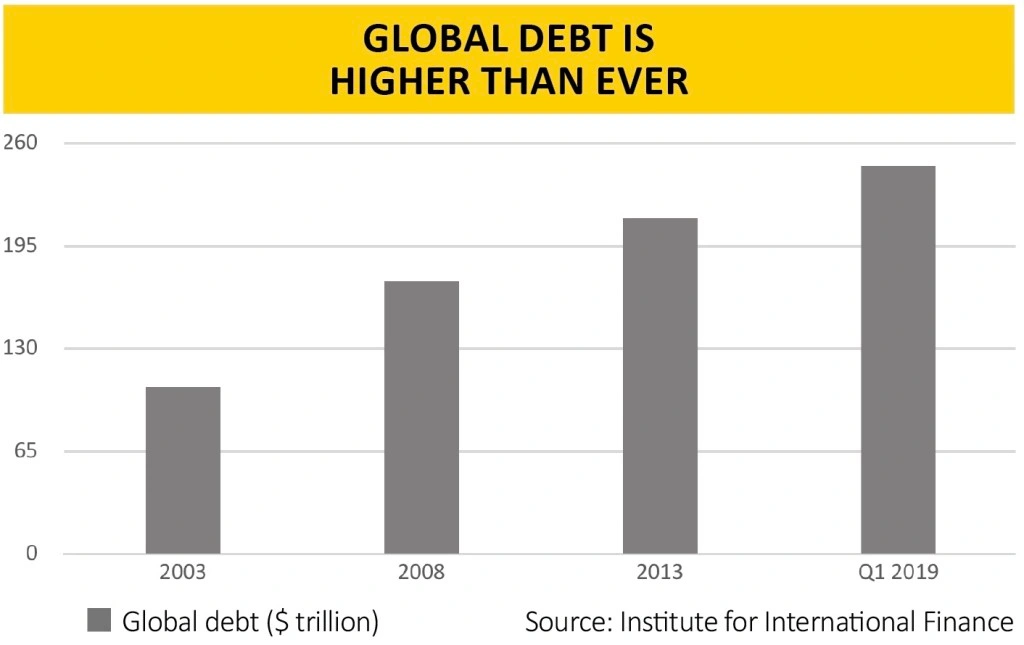

According to the Institute of International Finance (IIF), global debt ended the second quarter 2019 at $246tn, or 320% of GDP. The good news is this is $2tn below the Q1 2018 peak in monetary terms but it matches the all-time high of Q3 2016 as a percentage of GDP.

The bad news is that global debt is now some 40% higher than when the Great Financial Crisis began. The world simply cannot afford interest rates to match those seen between 2006 and 2008, when they peaked at 5.25% in the US and UK and 4.25% in the EU.

This raises the spectre of a Japan-style debt trap, to match the one that has devilled the Bank of Japan since 1989 – and remember that the Nikkei 225 still trades some 45% below the all-time high it reached right at the end of the 1980s, even after three decades of zero or negative interest rates and umpteen rounds of QE.

This suggests that Abraham Lincoln may have been on to something when he asserted that ‘You cannot bring about prosperity by discouraging thrift’.

Japan’s experience hints that interest rates in the West go a lot lower for a lot longer than we expect as central banks strive to conjure up growth and inflation by trying to encourage governments, consumers and companies to borrow and spend.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.