Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

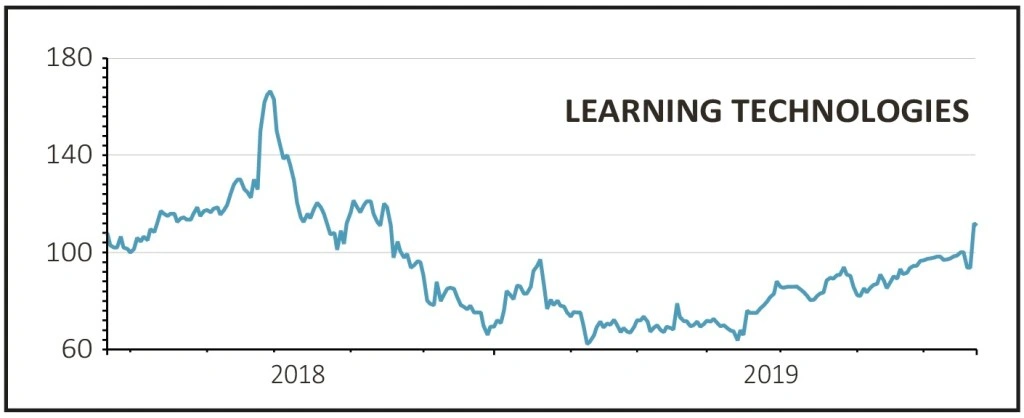

magazineLearning Technologies keeps on growing

LEARNING TECHNOLOGIES (LTG:AIM) 114.8p

Gain to date: 53%

Original entry point: Buy at 75p, 25 April 2019

Corporate online trainer Learning Technologies (LTG:AIM) is knocking it out of the park this year and investors are jumping in for the ride.

In just three months since our original Great Idea at 75p, the stock has soared an impressive 53% and analysts, like Shares, believe there is more to come.

On 22 July the £767m business announced that earnings before interest and tax, otherwise referred to as operating profit, would be ‘materially ahead’ of market expectations.

Forecasts had been pitched at £35.3m operating profit on approximately £128m revenue. Analysts now see £38m to £40m operating profit this year.

This is largely because of cost efficiencies being driven out of past acquisitions, including NetDimensions and PeopleFluent, thereby boosting profit margins. Operating profit margins shot up from 26.3% to around 32% in the half year to 30 June, according to the trading update.

That’s the good news. The really good news is that there are extra value levers still to pull, particularly within PeopleFluent, a business that had been run for cash but is starting to get a new lease of life.

SHARES SAYS: Keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.