Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

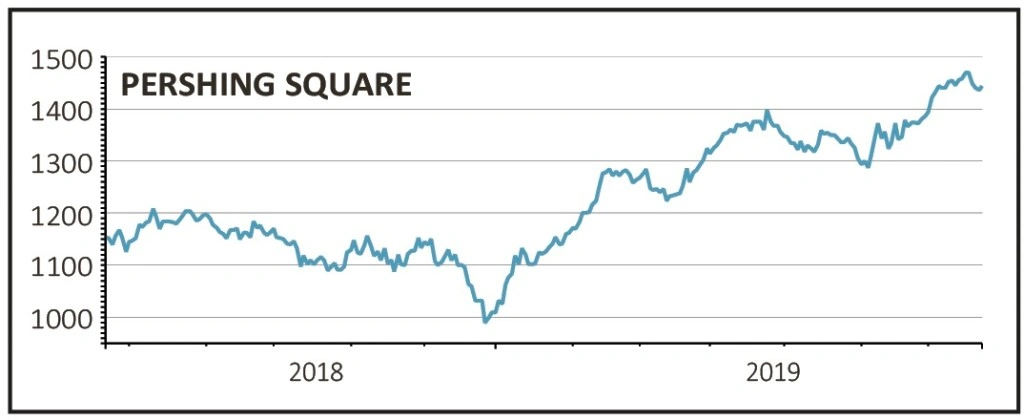

magazineWhy we’ve changed our view on Pershing Square

Pershing Square (PSH) £14.46

Gain to date: 8.2%

Original entry point: Buy at £13.36, 16 May 2019

We are executing a swift U-turn with our trade on hedge fund guru Bill Ackman’s Pershing Square (PSH) vehicle after the investment trust made plans to borrow more money to invest.

Increasing its borrowings, also known as gearing, from 18% to 25% of net assets substantially changes its risk profile and is too aggressive in our view as high levels of gearing can work against a trust in a market downturn.

Two of its biggest shareholders, Asset Value Investors and Metage, have also expressed concerns over the plan to place $400m of bonds with a coupon of 4.95%. The bond issue was scheduled to complete as this edition of Shares was published (25 July).

The investment trust team at Numis say the nervousness is justified as the move reduces the board’s ability to manage the wide discount to net asset value (NAV) and has the potential to act as a ‘poison pill’ on any potential restructuring.

Given Pershing had slowly been repairing its reputation with an improved performance in 2019, it might have been better for the trust to keep its head down for a bit longer rather than taking such a bold step.

This is particularly important when you consider it will probably be putting its newfound financial firepower to work in a US market which several observers have suggested is looking overvalued.

Ackman himself has been on record as saying he would not be surprised to see Pershing Square trade at a higher discount to net asset value if gearing were to increase – despite a recovery in the shares, the discount still stands at a smidge above 30%.

Investec says investors should sell the shares, adding that the proposed bond issue will take gearing to among the highest levels in the investment trust sector. It believes the trust would be better off accelerating share buybacks given how the stock currently trades well below the value of its underlying assets.

It adds: ‘With the S&P 500 having produced a NAV total return of 446% since March 2009 lows, the US economy now enjoying its longest economic expansion in history, and the New York Fed’s recession probability having just risen to 32.9% (with every breach of 30% since 1960 being followed shortly afterwards by a recession), the timing and quantum of this bond issue is a brave call.’

SHARES SAYS: Changing our minds on Pershing Square so quickly may look strange but reflects a significant shift in approach which we think have thrown the balance between risk and reward off kilter. Take profits now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.