Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

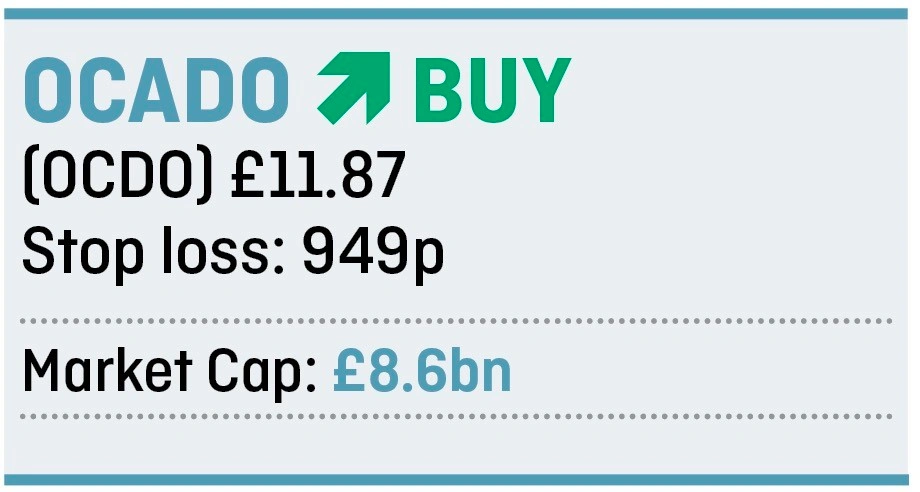

magazineTime to buy Ocado as it reaches a major turning point

The last two years have seen a transformation in Ocado’s (OCDO) business model from a grocery partner for a couple of middling UK supermarket chains – WM Morrison (MRW) and Waitrose – to a software-driven facilitator of online delivery for more than half a dozen retailers, many of which are based overseas.

The shares have re-rated dramatically, from 300p two years ago to £14 earlier this year, but we believe they are far from discounting the future value of the non-retail side of the business. Parallels with Amazon may seem premature, but many in the industry are already talking in similar terms.

Broker Peel Hunt believes Ocado has the potential to become the standard platform for the retail sector.

KEEPING IT SIMPLE

Ocado was born in 2000 out of a simple premise: that despite all the advances in technology, grocery shopping hadn’t changed since supermarkets were introduced to the UK 50 years earlier.

Thanks to its clever software, rather than customers having to drive to a supermarket and forage for food which had made its way through a long and complicated supply chain, Ocado would let them order their groceries online and deliver it directly to their front door from a central depot.

That made the customer experience easier and the distribution chain much shorter, which helped keep the fresh produce fresher.

Since forming its first branding and sourcing deal with Waitrose and starting commercial deliveries in 2002, orders have grown from 10,000 a week to over 300,000 a week in the first half of 2019.

OUT WITH THE OLD, IN WITH THE NEW

Ocado’s core retail business was originally based on sourcing products from Waitrose but this agreement expires in September 2020, at which point a new joint venture with Marks & Spencer (MKS) will take its place.

The new agreement, signed in February, sees M&S taking a 50% stake in Ocado’s UK retail business Ocado.com for £750m and supply its own-sourced and branded goods while the Ocado Smart Platform (OSP) provides solutions support and Ocado.com sells and delivers the products.

Separately, the OSP continues to provide the technology, logistics and distribution behind Morrisons’ online grocery business, Morrisons.com, and since 2016 Ocado has licensed the ‘store-pick module’ which is the software platform needed to fulfil online orders from Morrisons stores.

Morrisons operates the store-pick solution, for which it paid an upfront fee in 2017 for access, on top of an annual licence fee based on the volume of sales generated, while Ocado provides and maintains the software platform.

GLOBAL GROWTH OPPORTUNITIES

Consumers are increasingly going online to order their food which creates significant opportunities for Ocado.

While the UK still offers growth potential – online grocery sales are only 6% of the total market, which was worth £180bn in 2016, and are expected to approach 10% in the next few years – the growth opportunities are in licensing its software and solutions abroad.

Ocado already has six international partners including French hypermarket chain Casino (2018 sales: €36.6bn), US food retailer Kroger (2018 sales: $121bn), Canada’s Sobeys (2018 sales: C$24bn) and Australia’s Coles Group (2018 sales: A$29bn).

Fees invoiced to these partners almost doubled in the first half of this financial year to £46.7m, with only a tiny proportion recognised as revenues due to accounting rules, and these fees are set to grow significantly as consumer fulfilment centre deliveries ramp up and Ocado finds new partners in food and non-food verticals.

Analysts at Peel Hunt estimate that the top 100 store-based retailers around the world generated $4.33trn of revenues in 2016. Around $89bn was spent on capital expenditure, or 2.6% of average revenue for the top 10 retailers. By comparison, Ocado charges roughly double that percentage of a partner’s gross annual sales as a fee due to the cost savings it brings.

However, assuming that the addressable market is ‘just’ $90bn, of which less than half could be available for solutions which Ocado offers, and a market share of less than one third, Peel Hunt believes the revenue opportunity for Ocado is $11bn or £8bn a year. That compares with total Solutions revenue last year of £123m, so the upside potential is abundantly clear.

BETTER POSITIONED THAN EVER

In a recent presentation to analysts and investors, chief executive Tim Steiner summed up the changes within the group and the opportunities ahead.

He said: ‘2019 has seen a shift in the centre of gravity at Ocado. We have pivoted from being a pure-play online grocer in the UK with a separate Solutions business to being a technology-led global software and robotics platform business providing a unique end-to-end solution for online grocery.

‘Ocado.com is now one of eight global partners, all among the most innovative and forward-looking grocers in the world, whose online business will be enabled by the Ocado Smart Platform. We have never been in a better position to create value.’

Previous technology winners such as Amazon and Apple have followed a similar pattern on the market – their share prices have shot up (the hype cycle), come back (as reality sinks in) and then experienced a ‘lift off’ where the shares have soared. Ocado has also followed this path.

We believe the stock has much further to travel as existing partnerships become active and new opportunities are grabbed.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.