Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy China still needs a trade deal

China’s second quarter GDP growth figure of 6.2% year-on-year appears to be the source of some market angst, not least because it represents the slowest rate of increase since 1992, which is as far back as Beijing’s records go.

It is possible to argue that such a rate of advance is remarkable for what is the world’s second largest economy. If China were to maintain that growth rate for all of 2019, then its economy would, based on World Bank data, grow by $844bn this year. That is more than the entire output of Saudi Arabia, the world’s eighteenth-largest economy.

And yet economists and investors alike seem concerned. The degree of worry among the latter can be easily measured by using the Shanghai Composite as a benchmark: the index trades no higher now than it did in January 2007.

The benchmark even stands some 10% below its April high, thanks in no small part to how $7.4bn flowed out of Chinese equities in May. That was the biggest monthly outflow since June 2013, according to data from the Institute of International Finance.

Yet this bad news could be good news. The prevailing nerves about the economic outlook may persuade patient contrarians to think there is some value to be had, with Chinese equities trading on around 14 times forward earnings.

Economic jitters

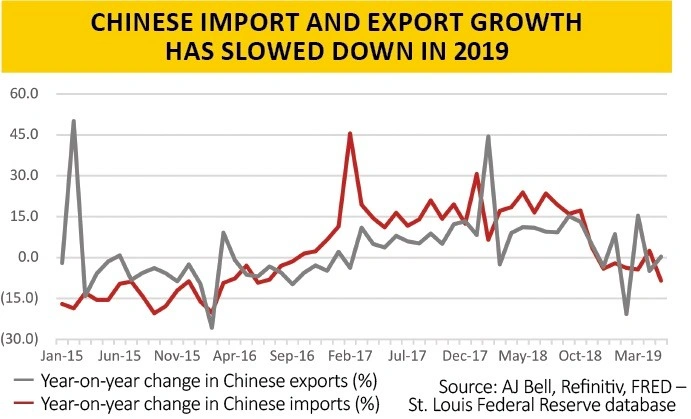

All the same, three charts make it easy to see why economists and asset allocators are a bit nervous.

The first is the marked slowdown in Chinese export and import activity. Imports have fallen year-on-year five times in the last six months and in May exports grew just 0.3% year-on-year.

The former may reflect domestic softness, the latter slower global growth but also the impact of the trade dispute with America, where there seems little sign of an immediate resolution despite the hopes raised by President Donald Trump at June’s G20 meeting in Osaka, Japan.

The second may be a spill over from the trade slowdown. Chinese producer price inflation has slowed down, raising fears that the country’s manufacturers may be sliding into some sort of supply-side glut or even a deflationary bust. Similar concerns did a huge amount of damage to the Shanghai Composite in 2015-16.

The third is car sales. China is trying to pivot away from making stuff for export and building bridges to nowhere, or at least properties where no-one lives, and toward consumption.

A slide in the auto market suggests this plan may be hitting a speed-bump with volumes set to fall for the second straight year.

Policy response

President Xi and the Communist Party are not just letting events unfold around them. The government has increased export rebates, cut corporate pension contribution requirements and trimmed taxes.

The People’s Bank of China has also done its bit in the form of interest rate cuts and a decrease in the reserves that banks are required to hold, in a bid to boost lending.

China’s government debt is relatively low at $6.5trn or 48% of GDP so there looks to be plenty left in the tank when it comes to potential stimulus. But add in financial sector debt, household debt and soaring corporate debt and those figures rise to around $40trn or nearly 290% of GDP, which looks less comfortable.

As such, the authorities in Beijing have a tricky balancing act, as they encourage growth with cheap cash and fiscal stimulus yet at the same

time stop debt-fuelled housing and financial markets from becoming too bubbly. Although in this respect it could be argued that China is no different from the US, UK, Canada, Australia or Sweden, for example.

Growth could take on more of a stop-start pattern than previously, as stimulus boosts the economy (as per 2016), only for its effect to start to wear off (as per 2018) and the authorities to then step in again (as per 2019).

But of the three issues which held back Chinese equities last year, two now look less problematic. Oil has retreated to $60 a barrel, which helps since Beijing is a net buyer of crude. The dollar may have peaked, using the DXY (‘Dixie’) trade-weighted index as a guide, as the Fed prepares to cut rates and the White House talks down the buck.

That still leaves the third issue – trade. Financial markets are working on the principle that both Presidents Trump and Xi need a deal so one will be done. The intertwined issue of technological supremacy unfortunately means that reaching an agreement may be a lot less simple than it looks, although Chinese stocks are still discounting a negative outcome from the negotiations with Washington.

Any trade deal with the US, assuming there is one, could therefore be a step on the road to a more sustainable recovery for the Shanghai stock market.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.