Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

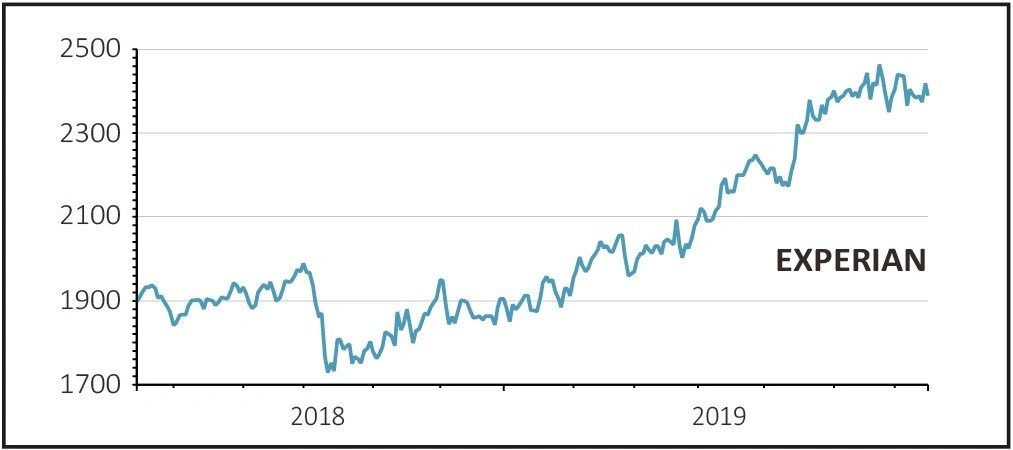

magazineExperian shares are up 26% since we said to buy last summer

EXPERIAN (EXPN) £23.65

Gain to date: 26.5%

Original entry point: Buy at £18.69, 9 August 2018

The first quarter update from information services company Experian (EXPN) shows the company can still grow revenues at a respectable pace (6% organic, or like-for-like) despite strong growth in the same quarter last year following major contract wins.

North America continues to be the main driver with 8% organic revenue growth, helped by the recent acquisition of AllClear ID. Alongside the business-to-business (B2B) operations, the consumer side traded well with 9% organic growth.

Latin America had a strong start to the year with 9% organic growth thanks to strong demand in Brazil for both business and consumer services.

Europe and Asia saw a dip in organic growth due to a strong comparison with last year although India was a stand-out performer and total revenues rose thanks to the acquisition of Compuscan in South Africa.

The UK was a mixed picture with encouraging growth in data services but overall B2B revenues were flat and consumer revenues were marginally higher.

The company has confirmed its guidance for this year and we continue to like its ‘economic moat’ which allows it to generate organic growth and substantial free cash flows without substantial risk of new entrants coming into the market.

SHARES SAYS: Experian’s shares are just off their all-time highs but we would stick with them and add on any weakness.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.