Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe key reasons why you need to invest in Microsoft

While everyone will know Microsoft as a brand, the inner workings of its business are perhaps less well known among investors even though it is widely held, either directly through shares or via investment funds.

No company did more to seed the personal computing explosion in the 1980s and 1990s, and it is today the world’s largest listed business, worth $1.06trn. Windows and Excel spreadsheets are as familiar to most of us as the BBC news or PG Tips, and Bill Gates’ pullovers are legendary.

With Microsoft forecast to report nearly $125bn in revenue for the year to 30 June 2019, we now look at its growth opportunities, business challenges, dividend prospects, and the valuation investors are expected to pay for the US-listed shares.

MICROSOFT REINVENTED

This is not the company that it once was, emerging as a great example of how a fine business can lose its way and then reinvent itself, becoming stronger than ever.

Its modern success is largely down to visionary chief executive Satya Nadella who has been in the top job since 2014.

Today the company operates via several major divisions which can be split roughly into three segments; Productivity and Business Processes, Personal Computing and Intelligent Cloud.

Nadella’s crucial triumph has been to transform the company into a cloud-based software-as-a-service model, streamlining the user experience and building a vast pool of recurring revenues.

Such a transformation was a difficult process, dragging on revenue and lowering margins as profitable servicing and maintenance income slowed – and the transformation is arguably still ongoing today.

But down the line this will mean much greater visibility, increasingly sticky users as well as slashing the cost of distribution. Software updates can be rolled out across the vast user base centrally, while upgrades and up-sales are more seamless for customers, which should drive margins in time.

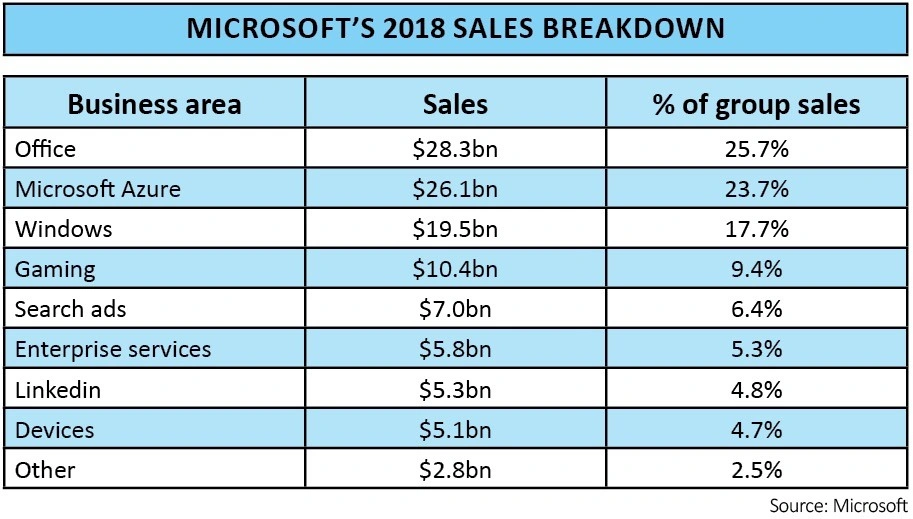

Subscription-type revenues make up about a third of Microsoft’s annual sales and are headed for 50% by 2022, according to the company. Its Azure cloud platform is now seen as its chief growth lever.

AHEAD IN THE CLOUD

In its last earnings report, the third quarter to 31 March, commercial cloud revenues (Azure, plus Office 365 and Dynamics 365) increased 41% year-on-year to $9.6bn, putting it in line for $38.4bn of annualised revenue. Azure revenue alone jumped 73%.

That compares to $30.6bn of revenue overall, up 14%. Cloud gross margins increased from 58% to 63%, underlining the profitability expansion potential we mentioned earlier.

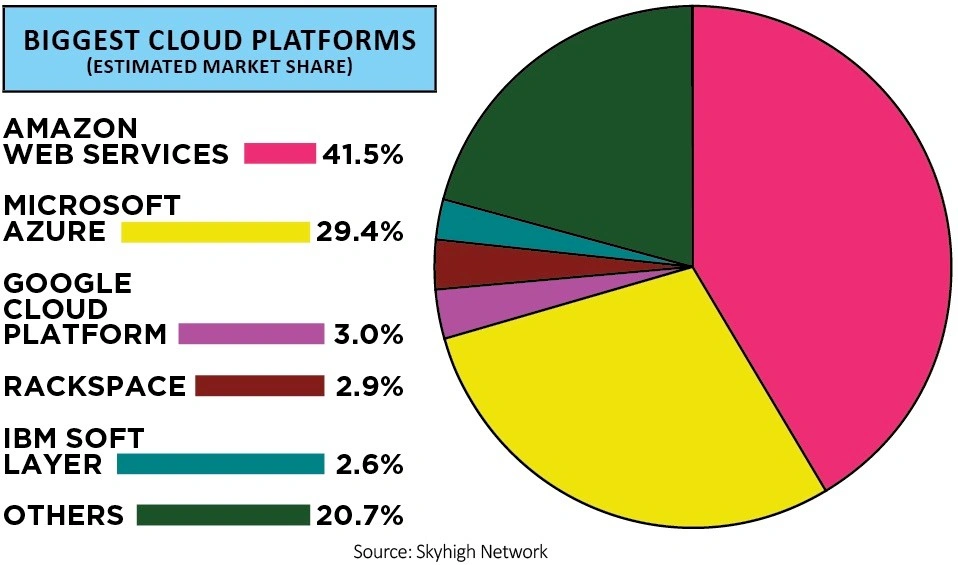

To put this into perspective, Microsoft Azure is already the world’s second biggest cloud analytics and applications platform, behind only Amazon’s AWS. Yet experts believe that cloud computing has decades of growth ahead with mainstream adoption still in its early days and with new services and applications emerging all the time.

Crucially, this means that Azure growth should remain rapid without Microsoft having to eat Amazon’s AWS lunch.

Microsoft is a company with rock solid and growing revenues, expanding margins and a solid balance sheet.

As of December 2018, Microsoft had $73.2bn of debt offset by a bulging bank account with $127.7bn cash, resulting in a $54.5bn net cash position which Morningstar calculates to be worth about $7 per share.

Net income in the June 2016 financial year was $22.3bn and, if analysts are right, that will top $35.5bn for 2019, and hit $44.7bn by 2021. Encouragingly, analysts flag Microsoft’s nifty habit of consistently beating analyst earnings and revenue projections.

Microsoft's main interests

Productivity and Business Processes – includes Office and Dynamics product lines, and LinkedIn platform

Intelligent Cloud – encompasses server products, cloud services and enterprise services offerings

Personal Computing – includes Windows licensing, Xbox-related gaming and revenue from its Surface family of products and PC accessories

CRUNCHING THE NUMBERS

At $138.99, Microsoft is trading close to all-time highs yet the shares are not overly expensive. On Reuters consensus estimates, the stock trades on a next 12 months price-to-earnings (PE) multiple of 26.6, versus 24.3-times for peers (Oracle, Apple, SAP among them).

The PE ratio falls to 24 on 2021 forecasts. Investors are also likely to get a near-$2 per share dividend over the next year, implying a decent 1.4% yield for what remains essentially a growth stock.

SHARES SAYS: The question should not be whether you should own Microsoft (the answer is ‘yes’) but how you should own it.

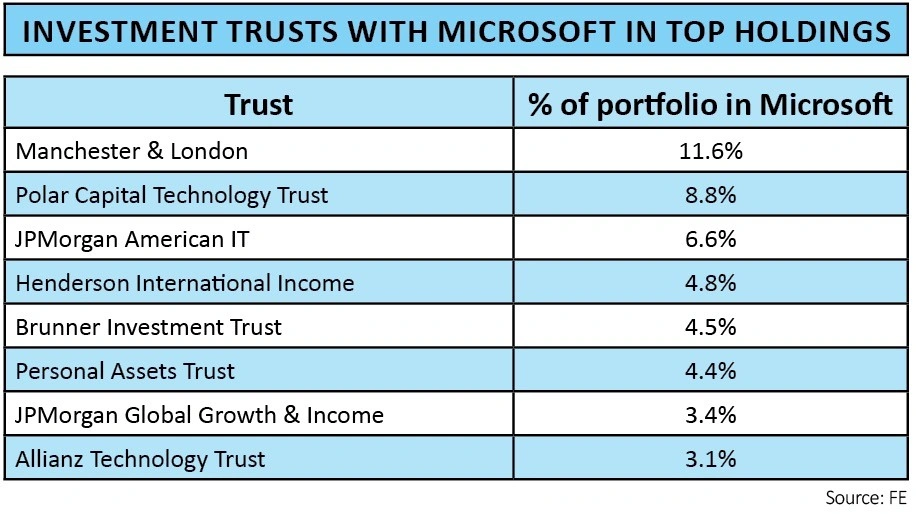

If you own any sort of global or US equities tracker then you own a bit of Microsoft. This will also be the case for investors that have actively-managed technology funds or investment trusts in their portfolios.

For many that may be enough, particularly for those wanting to avoid the extra complexity of W-8BEN tax forms that need to be filled out by UK investors buying US stocks.

The alternative of directly owning Microsoft shares looks like a very sensible option given the technology giant’s growth, income and all-round financial muscle. Creating growth opportunities in the highly competitive tech space requires proactive management and that’s exactly where Microsoft’s strengths lie.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.