Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIncome alert: will car insurers put the brakes on big dividends?

Motor and home insurance stocks have generated significant returns for investors over the past decade with the FTSE All-Share non-life insurance index almost trebling between 2009 and the middle of 2018.

However increased competition, rising claims – and the need to hold more capital to meet future claims – together with tighter regulation mean that the party may be coming to an end.

While the sector pays attractive dividends, are these high yields enough to compensate for the increased risk? We believe there is a significant threat to future dividend payments which means investors may have to think twice about holding these stocks.

SIZE ISN’T EVERYTHING

The UK is the world’s fourth largest insurance market after the US, China and Japan. In 2017 total premium income was £220bn, of which roughly 40% or £90bn was non-life business according to the Association of British Insurers (ABI).

While this is a sizeable market, premiums have actually shrunk slightly since 2015 due to rising price competition spurred by regulatory changes, including sweeping reforms to the personal injury compensation system, and consolidation among the various players.

There are further changes coming with the way in which the size of large personal injury claims is calculated (known as the Ogden rate) due to take effect this year and the Civil Liability Act (2018) coming into effect next year. These are likely to reduce profits and increase the amount of capital the insurers need to keep to meet future claims.

BATTEN DOWN THE HATCHES

After a series of extreme weather events in 2013 and 2015, the UK had a fairly benign time weather-wise in 2016 and 2017 in contrast with much of the rest of the world.

That all changed last year when the Beast from the East caused £328m of weather-related claims in March, causing some insurers to

use up their full year’s weather reserves in the first quarter.

This was followed by record-breaking summer temperatures and minimal rainfall which caused a surge in subsidence claims with both the volume and value of the claims at the highest level for several years.

A recent paper from the Environment Agency predicts that climate change will mean more extreme weather and flooding for the UK and that costs for the banking and insurance industries could rise dramatically with losses on mortgages potentially trebling.

A previous report from the Committee on Climate Change estimates that in 50 years up to 1.5m properties in England could be in areas of ‘significant’ flood risk.

While the insurers might be able to charge higher prices to offset some of the increased risk, more frequent flooding and extreme weather events mean they will need greater reserves of capital than in the past to meet higher claims.

MOTOR INSURERS GETTING BOXED IN

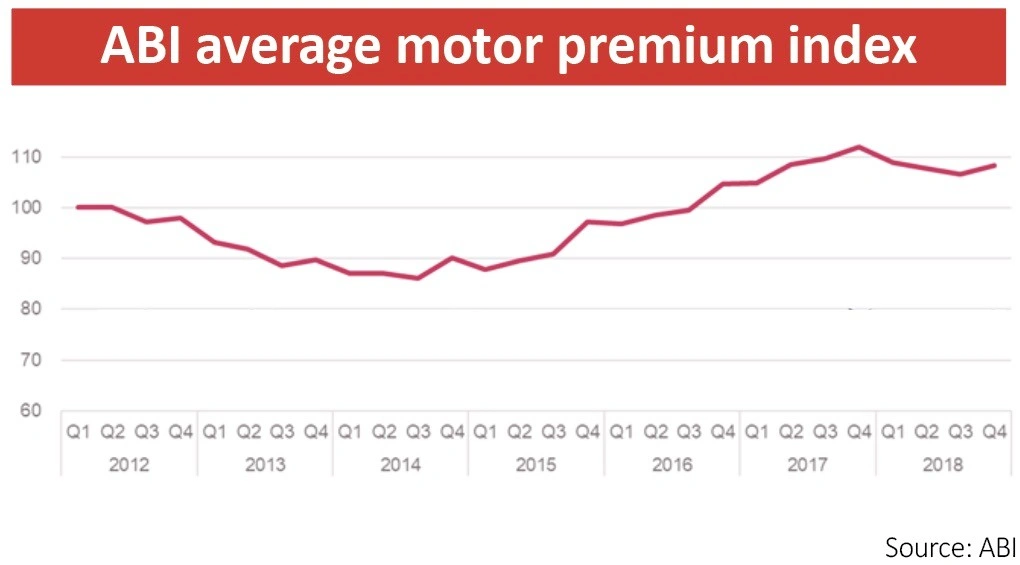

The motor insurance market has become markedly more competitive in the last 12 months with premiums falling around 5% during the course of 2018 as providers fight to retain customers.

Profitability is an ongoing challenge as the industry struggles with flat or falling revenues and a sharp increase in costs.

The common theme among the insurers in their 2018 results and 2019 trading updates is the record level of claims inflation, in particular bodily injury and third-party property (which in this case means vehicles).

Hastings (HSTG) recently cited high repair costs and third-party property damage costs as key issues and warned that ‘if the current premium and claims dynamics continue through the year’ the group’s loss ratio would be at the top (i.e. worse) end of its target range. The term ‘loss ratio’ is used to describe the amount of claims paid to customers in relation to the total premiums received in a year.

In a similar vein, Direct Line (DLG) reported that premiums across the market were failing to keep up with claims inflation, which it said was running at the upper end of its long-term expectations of 3% to 5%.

The increasingly sophisticated technology used in cars has reduced the volume of claims but pushed up the cost of repairing and replacing damaged parts.

Rising labour costs and rising parts costs, exacerbated by the weak pound, mean that insurers are now paying £12m a day on repair costs alone, on top of £9m a day for bodily injury claims, according to ABI estimates.

Technology has also increased the insurers’ losses on car thefts as thieves are targeting premium cars with keyless fobs by intercepting the signal between the key and the car.

The average claim for a stolen car was over £8,000 in the second quarter of last year against £3,500 five years earlier and police records show the trend of thefts increasing.

REGULATORS ARE ABOUT TO HEAP ON MORE PRESSURE

Faced with fierce competition for customers and a high levels of costs, the last thing the insurers need is public pressure to cut premiums.

However the Financial Conduct Authority (FCA) and the Competition and Markets Authority (CMA) have both announced investigations into unfair pricing in the non-life insurance market (also known as the general insurance market).

Last autumn the FCA launched a probe into what it called the ‘excessive difference between premiums charged to new customers and those renewing’, with the former getting better prices at the expense of the latter, especially in home insurance.

It promised to ensure that the general insurance market delivers ‘competitive and fair prices for all consumers’ and ‘if change is needed to make the market work well we will consider all possible remedies’ including intervening directly.

This could mean fines for misconduct, or worse, making the insurers compensate customers for past mistreatment.

There is also a risk that these ‘remedies’ spill over into the motor insurance business which for most quoted companies is much bigger than home insurance in terms of premium income.

For the avoidance of doubt, the FCA sent a ‘Dear CEO’ letter to the heads of all the general insurance firms citing the example of Carphone Warehouse which it fined £29m for mis-selling insurance.

ARE DIVIDENDS AT RISK?

Historically the general insurers have been popular with income investors as they tended to pay a dividend yield well above the market average.

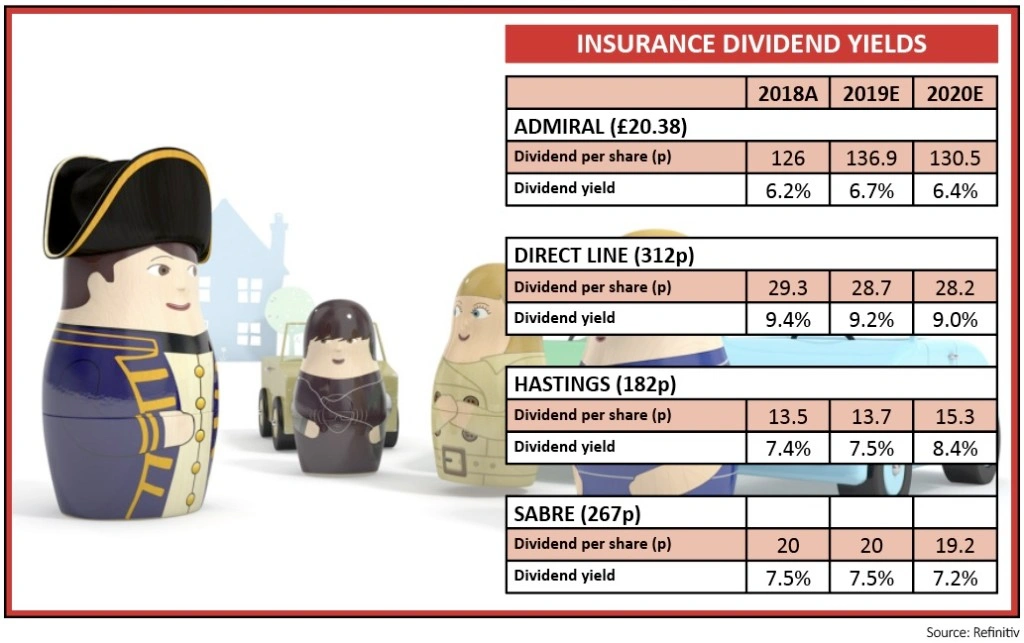

Today Direct Line is trading on a prospective yield of 9.2% and Hastings is on a yield of 7.5% so the income argument is still valid assuming that the dividends aren’t cut.

For 2019 and 2020, the consensus sees Admiral (ADM), Direct Line and specialist insurer Sabre (SBRE) paying almost all of their earnings out in dividends while Hastings is seen paying out around 70% of earnings.

Direct Line is the second-biggest player in motor insurance among the non-life players after Admiral, with just under £1.7bn of gross premiums last year, and the biggest home insurer with over £600m of gross premiums although it is worth flagging that these were down sharply last year. It is also the most profitable in both lines.

Home insurance: there may be trouble ahead

The Environment Agency has launched a consultation paper on its flood policy with the warning that climate change will lead to more extreme weather events in the UK, impacting the banking and insurance sectors.

The agency predicts that the number of houses built on floodplains will double over the next 50 years and that building flood and coastal defences will cost an average of £1bn per year.

Chairwoman Emma Howard Boyd advises that, despite improving coastal defences and contingency plans, it won’t be possible to protect everyone. She says: ‘In some places we can’t eliminate all flooding and coastal change and we need to be better at adapting to the consequences.’

Some communities which have suffered severe flooding in the past will have to decide whether to stay and risk more frequent and more damaging floods or move out of harm’s way and abandon their homes altogether.

In 2013 a tidal surge hit the east coast and the Humber estuary forcing thousands of people to abandon their homes as areas of the North Sea rose more than five metres, exceeding the levels of the infamous 1953 surge which flooded 1,000 square kilometres of land and killed over 300 people.

The 2013 floods, combined with what until then was the wettest winter on record, cost the UK insurance industry £1.2bn or an average of £31,000 per claim.

In 2015, heavy flooding cost the industry a further £1.3bn or an average payout of £50,000 per claim according to the ABI.

For Admiral and Hastings, home insurance is barely profitable. Admiral made a big push in home insurance last year increasing the number of properties it insured by 31% to 870,000 and increasing its gross premiums from £107m to £146m, yet it turned from a profit of £4.1m to a loss of £3m.

For Hastings, home premiums last year were £7m against motor premiums of £950m so it is hardly a meaningful part of the business, and Sabre only offers motor cover.

Given how exposed Direct Line is to the UK home and motor markets and how much margins are under pressure in the motor business, we would be concerned about the safety of its dividend, which includes an assumed 7p special payment on top of normal dividends.

Admiral has a large overseas motor insurance business which generated £484m of gross premiums last year and it owns a price comparison business, including the Confused.com brand, which generated over £150m of premiums.

This makes its revenue base more diversified although both units are loss-making which weighs on earnings and may put the prospective 6.7% dividend yield at risk.

Hastings is almost a pure play on motor insurance so it will feel the squeeze from softening premiums and rising claims inflation the keenest, but it also has the most leeway to maintain its dividend which at 7.5% is still well above the market average.

All these factors suggest that anyone relying on generous dividends from insurance stocks must ensure they have alternative sources of income via a diversified portfolio in case insurance sector dividends don’t grow or are cut in the short to medium term.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.