Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe case for and against US stocks and shares

After all of the hullaballoo surrounding their flotations, most investors will be aware Lyft is in need of a boost and Uber is stalling immediately after their respective initial public offerings (IPOs).

Whether such huge deals ‘call the top’ or not remains to be seen, even if experienced investors may be looking back to some uncanny parallels with the final stages of the technology, media and telecoms bubble of 1998-2000.

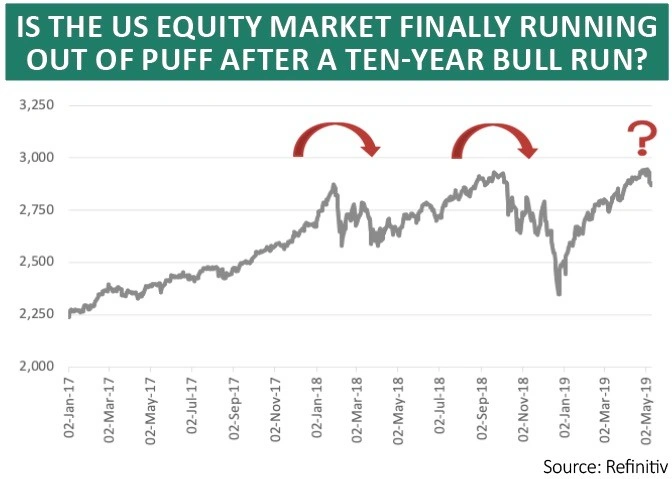

This is because one wobbly week, owing to an escalation in the trade dispute between the US and China, leaves the S&P trading no higher than it did in January 2018, despite a 20%-plus rally from the December low and the S&P 500’s attainment of a new all-time high of 2,946 on 30 April.

That overall lack of progress is quite surprising given the bullish tone which has characterised the US equity market for the last 17 months (and more) and chartists may be tempted to argue that a ‘triple-top’ pattern is emerging in the benchmark S&P 500 index.

Whether investors have any truck with technical analysis is up to them, but the current chart does at least give pause for thought, if you keep in mind the old adage that ‘market tops are a process, market bottoms are an event’.

REASONS TO BE CHEERFUL

The US stock market has stumbled many times since it hit bottom in March 2009 and bulls of US stocks are unlikely to be concerned, especially as the S&P 500 trades within 2% of its recent new peak.

Supporters of US exposure will argue that American equities are far from excessively valued on around 18 times earnings for 2019, based on consensus analysts’ forecasts, for three good reasons:

– The economy looks like one of the best performers in the Western World.

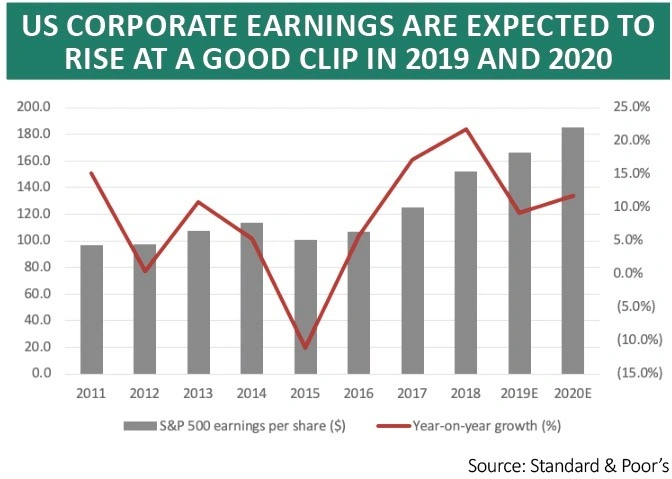

– US corporate earnings are forecast by analysts to rise 9% this year and 12% next year.

– The Federal Reserve is running very accommodative monetary policy, with interest rates held at just 2.5% (below the first quarter’s annualised GDP growth rate of 3.2%) and quantitative tightening due to come to a halt in the autumn.

GROUNDS FOR CONCERN

There are counterarguments:

– Profit forecasts for 2019 are back-end loaded. Earnings growth is expected to surge from 3% to 4% year-on-year in the first three quarters to 26% in the fourth. Some allowance must be made for the base effect created by the December 2017 Trump tax cuts but this may be why markets think the trade talks with China are so important.

– If they go wrong, tariffs are applied, China retaliates and global growth slows then those second-half forecasts could look exposed and leave US stocks looking expensive.

– US corporate profits stand at a record high, so US stocks could start to look very expensive very quickly if there is a surprise economic slowdown or loss of momentum in corporate earnings growth.

– Also note that US corporate profits as a percentage of GDP peaked in 2012 to suggest that some margin pressure, in the form of wage growth, is already creeping in.

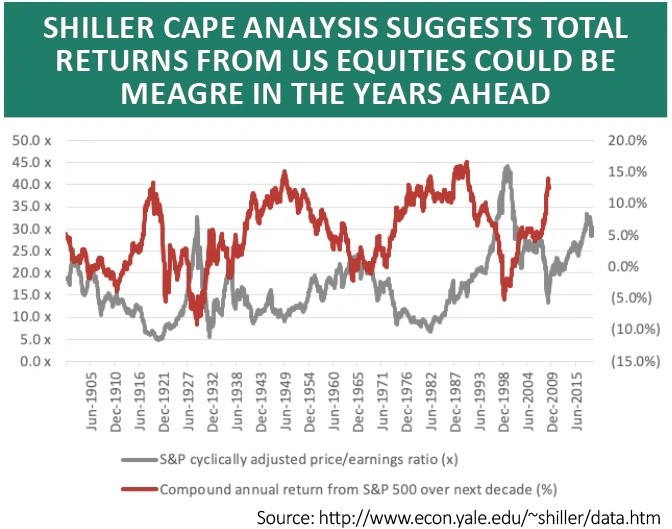

– Robert Shiller’s cyclically-adjusted price-to-earnings (CAPE) ratio puts US stocks on 30 times earnings. They have only been more expensive twice in their history and those episodes – 1929 and 2000 – did not end well for investors. Those who doubt Shiller’s data argue that CAPE is a poor market-timing tool. In the short term they are right but on 10-year view lofty CAPE ratios have consistently warned of poor future returns.

FINAL THOUGHTS

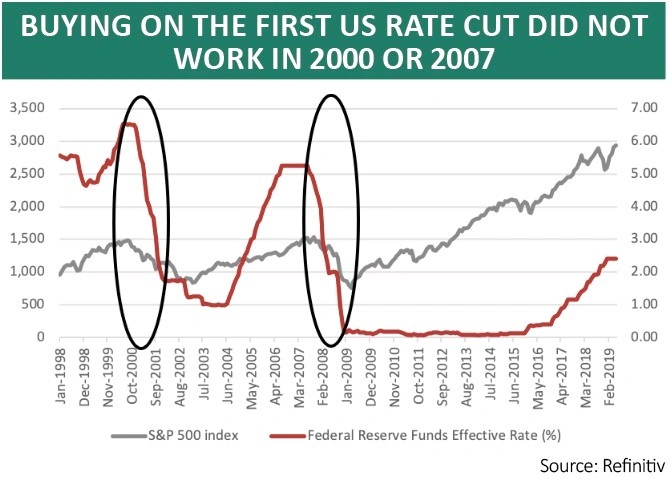

It is tempting when all else fails to rely on Federal Reserve, especially as the US central bank’s policy U-turn in January, when it stopped promising higher interest rates, followed some hefty stock market falls.

But even a cursory glance at the 2000-03 and 2007-09 bear markets shows that the Fed cut rates aggressively and it initially made no difference. Share prices still collapsed because valuations were stretched, earnings were disappointing and the economy was tipping over.

Ultimately a bear market needs three things to start, if history is any guide:

– Rich valuations. These are arguably now prevalent.

– An economic slowdown. There is no sign of this as yet, but the Fed does seem twitchy.

– Earnings disappointments. The first quarter reporting season has been fine, but 2019 estimates rely on a big acceleration in the second half.

This means the July second quarter reporting season could be particularly informative as it is likely to set the tone for the rest of 2019 and some time beyond.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.