Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDoes taking greater risk equal greater reward with investing?

The greater the risk, the greater the potential reward is a common adage in investment. After all, if you could generate the best returns by investing in UK government bonds (also known as gilts), why would you ever think of putting any money into racier assets?

But measuring risk is difficult, and determining whether the rewards are commensurate with the level of risk you have taken is largely a matter of opinion.

Experts measure risk in a number of complicated ways. One of them is through something known as standard deviation. In investment, this figure is a way of expressing how far a fund sways from its average return. In essence, it shows how volatile the performance of a fund has been. The greater the standard deviation, the greater the swings up and down in a fund’s returns.

It’s a crude measure and by no means a perfect science, but it is one way of ascertaining how risky a fund may be.

Tom Becket, chief investment officer at Psigma Investment Management, says: ‘Investors should be compensated for taking higher risk in the form of greater returns, but whether this materialises depends on your time horizon for investing, your patience and capacity for risk.

‘Using quantitative analysis such as standard deviation can be helpful to determine how funds have performed at certain points in the investment cycle and how they might blend with the rest of your portfolio, but it shouldn’t be the main factor on which you base an investment decision.’

WHAT DO THE FIGURES SHOW?

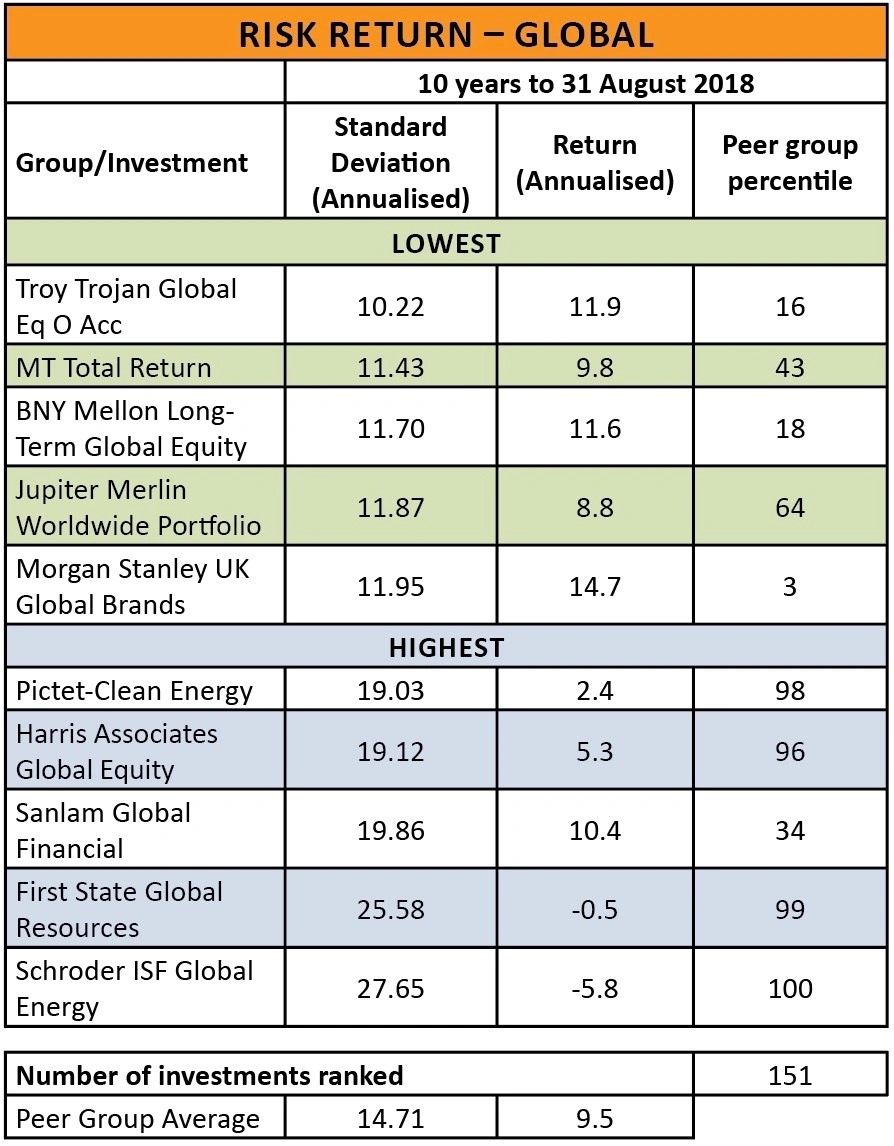

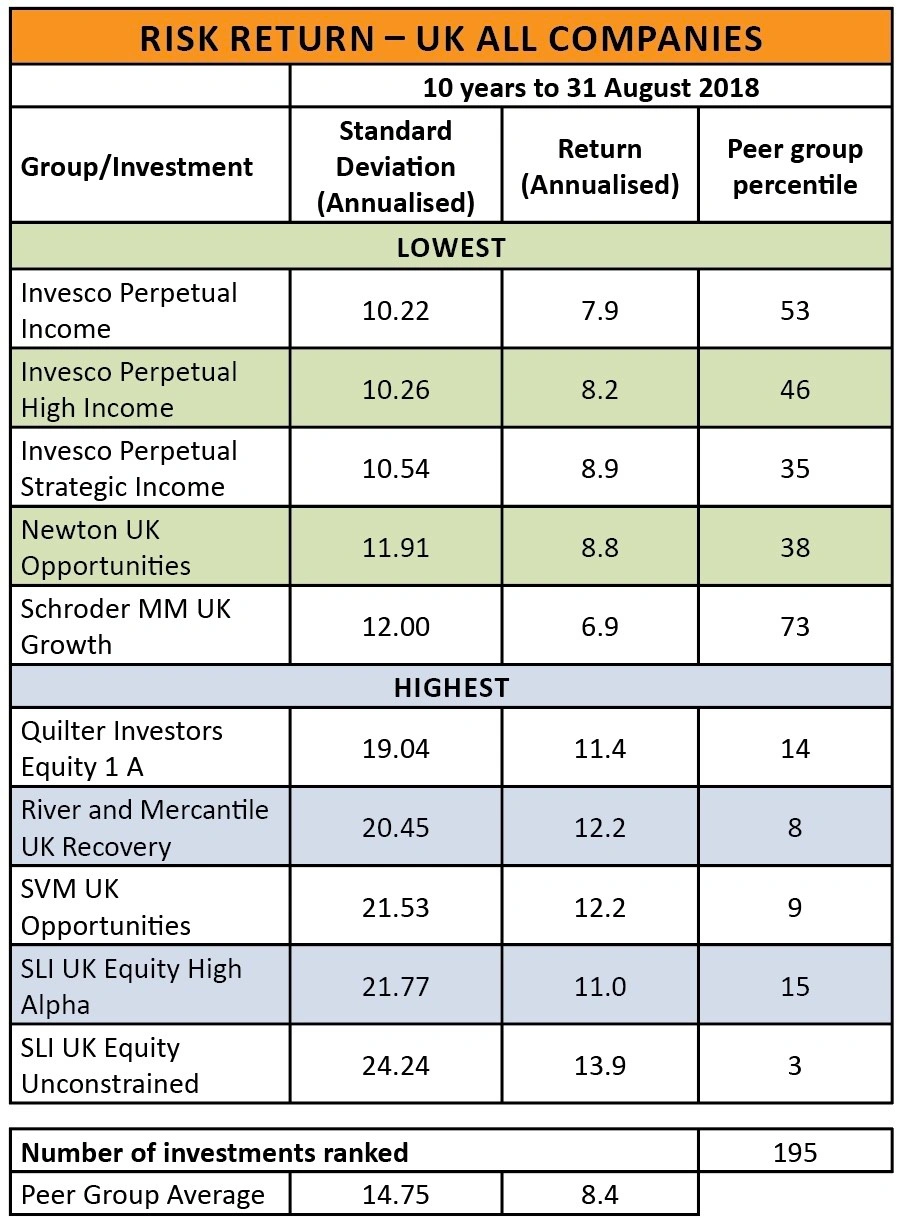

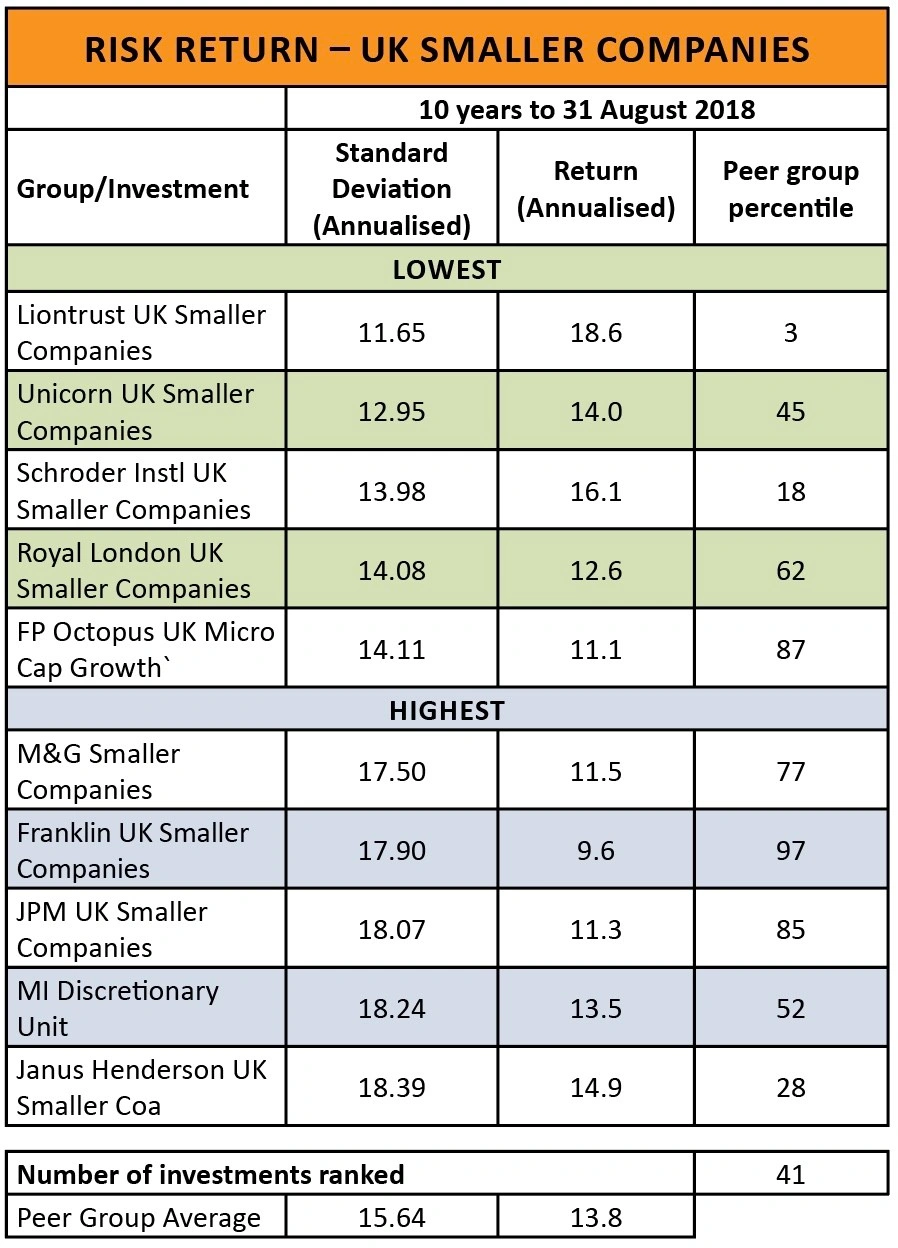

The correlation between a fund’s standard deviation and its performance is patchy at best. Analysis from stockbroker AJ Bell shows the performance of funds with a track record of at least 10 years, detailing their standard deviation and annualised return over that period, as well as the percentile ranking of the fund within its peer group.

With thousands of funds available to UK investors, the tables in this article show only a snapshot of the data, illustrating the five funds with the highest and the lowest standard deviation within the UK All Companies, UK Smaller Companies and Global investment sectors.

In the UK All Companies sector, greater risk certainly seems to produce greater rewards: the Standard Life UK Equity Unconstrained (B7LK223) fund has a standard deviation of 24.24 – significantly higher than the peer group average of 14.75 – and it has also produced an annualised return of 13.9% over the past decade, putting it in the third percentile of performers.

Meanwhile, the Invesco Perpetual Income (BJ04HX6) fund, which has the lowest standard deviation in the sector, has produced an annual return of 7.9% over the same period.

But, it’s the Liontrust UK Smaller Companies (B57TMD1) fund which is the standout performer in the UK Smaller Companies sector. The fund has the lowest standard deviation of its peer group at 11.65 – compared to an average of 15.64 – and has produced a stonking annualised return of 18.6% over the past 10 years, putting it in the third percentile.

Meanwhile the average UK smaller companies fund has an annualised return of 13.8% over the same period and Janus Henderson UK Smaller Companies (0744762), the fund with the highest standard deviation, achieved 14.8%.

In the Global sector, meanwhile, the two funds with the highest standard deviation have produced negative annualised returns over the past decade.

TAKING RISKS DOESN’T GUARANTEE REWARDS

Wesley McCoy, manager of the SLI UK Equity Unconstrained fund, says: ‘People think of volatility as risk and as a bad thing, but it creates the opportunity to make money. But taking risk doesn’t guarantee rewards, that isn’t how it works. If an investment is offering you a high return, there’s a reason for that. It’s rare to find a high return in something that is very certain.’

He says periods such as Brexit and the global financial crisis, when stock markets are at their most volatile, are when his fund has produced some of its strongest returns. He explains: ‘We’re looking for companies that are mispriced or misunderstood by the market, where a volatile share price is expressing something that won’t matter in years to come.’

He points to Ladbrokes Coral as one recent example where the stock fell out of favour amid concerns about a government crackdown on the betting industry. In the end, the share price shot up as the company was bought by GVC (GVC).

STRATEGIC MOVES

Victoria Stevens, co-manager of the Liontrust UK Smaller Companies fund, aims to reduce risk by only taking small positions in stocks that the team deem as being potentially riskier. She says: ‘This is especially important in the small cap market, where individual stocks can be very volatile.’

To limit risk the team looks for companies with strong barriers to competition as well as those where the directors have a large stake in the business. The fund veers towards quality companies, which are ‘robust, dependable and better able to weather external economic shocks’.

Becket at Psigma adds: ‘People should take any measurements such as standard deviation with a huge pinch of salt because, ultimately, they tell you about the past and not the future. Just because something has or hasn’t been volatile in the past doesn’t mean that will continue in the future.’ (HB)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Weakness in Standard Life shares is not a buying opportunity

- Watch out for storm hit at Beazley and Hiscox after Lancashire warning

- Why soaring US Treasury yields are driving down stocks around the world

- Who is looking to connect with French Connection?

- Packaging sell-off ‘way overdone’, insist analysts

- Retailer QUIZ has questions to answer after major profit warning