Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

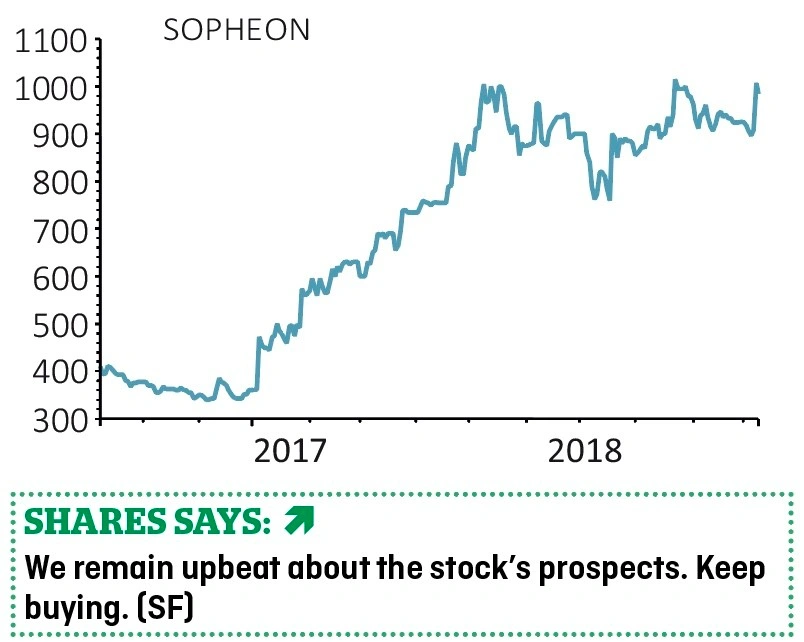

magazineSopheon raises the growth bar yet again

SOPHEON (SPE:AIM) 990p

Gain to date: 6.5%

Original entry point: Buy at 930p, 13 September 2018

It is early days with our current Great Idea on Sopheon (SPE:AIM) so investors would be wise to resist getting too carried away with this week’s upbeat trading update. That said; the business is developing quite the reputation for beating forecasts, a habit that goes back at least a couple of years.

Management are clearly being very careful about how investor expectations are handled, which is a good sign.

Innovation and product lifecycle software provider Sopheon now expects 2018 full year numbers to come in ahead of market expectations.

That prompted stockbroker FinnCap to raise its revenue estimates for this year from $31m to $32.5m and lift earnings before interest, tax, depreciation and amortisation (EBITDA) forecasts 5% higher to $8m.

What’s really interesting is that the third quarter is usually the quiet period before the fourth quarter storm. This suggests to us that perhaps some new business has been done early although we certainly couldn’t rule out future positive surprises.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Weakness in Standard Life shares is not a buying opportunity

- Watch out for storm hit at Beazley and Hiscox after Lancashire warning

- Why soaring US Treasury yields are driving down stocks around the world

- Who is looking to connect with French Connection?

- Packaging sell-off ‘way overdone’, insist analysts

- Retailer QUIZ has questions to answer after major profit warning