Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

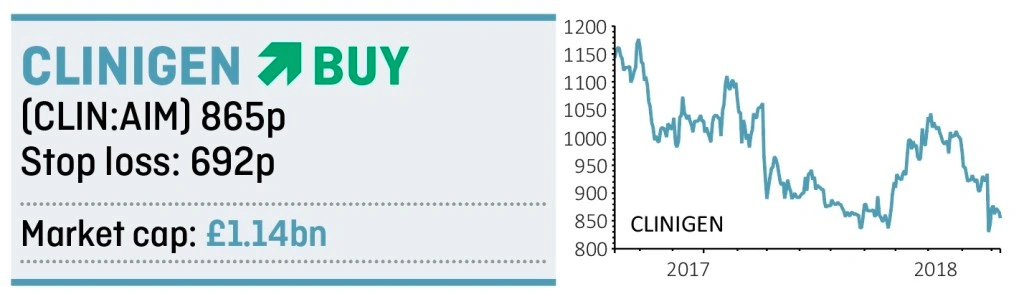

magazineBe brave and snap up Clinigen while its shares are weak

Recent share price weakness in speciality pharma firm Clinigen (CLIN:AIM) presents an attractive entry point for a business expected to deliver significant profit growth in the coming years.

Stockbroker N+1 Singer forecasts it will grow pre-tax profit from £69m in the year to June 2018 to £124m over the next three years.

While one of Clinigens’s recent acquisitions looks very expensive, the future rewards could be significant as Clinigen now has a stronger position in Europe and ‘the pieces are now coming together to create a true global platform’ says N+1 Singer contributing analyst Chris Glasper.

WHAT DOES IT DO?

Clinigen sends pharmaceutical products to hospitals around the world for patients with a high unmet medical need. It works with pharma businesses to make their drugs available for a volume-based fee or sales margin, or acquires and revitalises drugs so they can be applied to different markets than historically.

In the past financial year, the sale of unlicensed medicines comprised 45% of group profit while 44% was generated via licensed drugs. The rest came from its Clinical Trial Services (CTS) arm where Clinigen acquires drugs that will be used in clinical trials on behalf of pharmaceutical companies.

WHY HAVE THE SHARES BEEN WEAK?

Over the last year, shares in Clinigen have fallen from a one-year high of £11.77 last October to 865p. The sell-off was triggered by half-year results in February following a ‘significant divergence’ in divisional performance, according to investment bank Berenberg.

While its Commercial Medicines arm smashed forecasts of 15% growth with a 37% surge in profit, both unlicensed medicines and CTS missed expectations. The performance of unlicensed medicines has since reversed but the trend in CTS has continued.

It is important to recognise that CTS only contributes a small amount of overall profitability. Clinigen also made a management change in March to address underperformance of CTS and better position it in the US and drive future development globally.

Another share price sell-off happened in late September when Clinigen raised £80m to help buy packaging and distribution services specialist CSM. The acquisition price looks a bit rich in our view at approximately 15 times earnings before interest, tax, depreciation and amortisation (EBITDA). However, strategically it looks important to Clinigen’s desire to expand geographically.

It is now the job of the management to deliver on earnings expectations, or hopefully smash them, in order to win back the market’s favour. This is a high-risk investment given current weak market sentiment, yet we believe anyone taking the plunge could see handsome rewards in time. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Weakness in Standard Life shares is not a buying opportunity

- Watch out for storm hit at Beazley and Hiscox after Lancashire warning

- Why soaring US Treasury yields are driving down stocks around the world

- Who is looking to connect with French Connection?

- Packaging sell-off ‘way overdone’, insist analysts

- Retailer QUIZ has questions to answer after major profit warning