Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

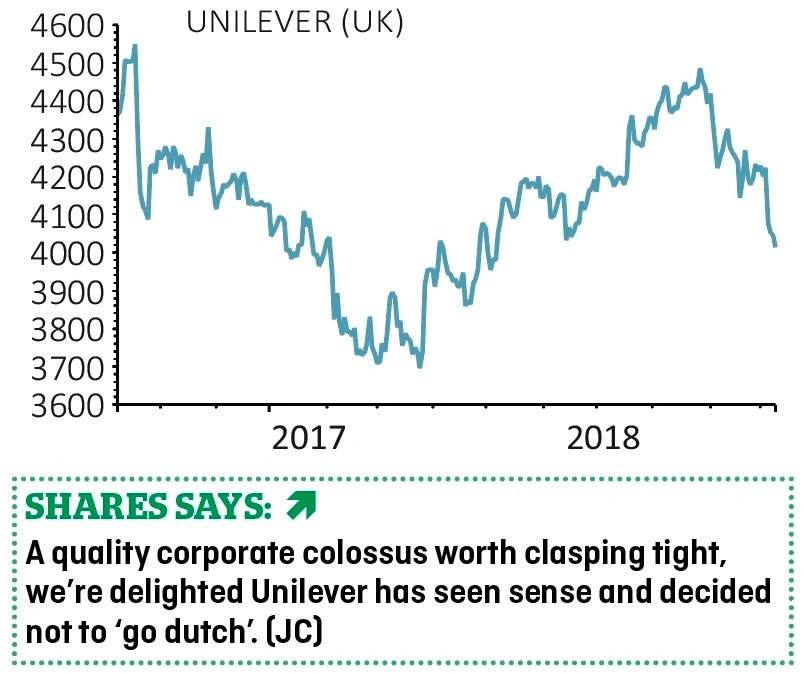

magazineUnilever ditches dud Dutch idea

UNILEVER (ULVR) £40.31

Loss to date: -5.2%

Original entry point: Buy at £42.53, 2 November 2017

Our late 2017 ‘buy’ call on packaged consumer goods giant Unilever (ULVR) may be slightly in the red, but we’re sticking with the high-quality business.

In a seismic development, the board at the Persil, PG Tips, Marmite and Magnum maker has capitulated to shareholder pressure and scrapped its plan to shift Unilever’s headquarters to the Netherlands.

This means Unilever is going to stay in FTSE 100, although the board’s reputation has arguably been damaged by the episode.

The blue chip company is a unique asset, a compounding star turn offering exposure to emerging markets.

Boasting an enviable portfolio of brands, deep entrenchment in the supply chains of its retailers is the source of Unilever’s wide economic moat and the company has reasonably predictable earnings.

Strong cash flows have enabled Unilever to consistently grow its dividend in real terms for decades and the shareholder reward is being supplemented by share buybacks.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Weakness in Standard Life shares is not a buying opportunity

- Watch out for storm hit at Beazley and Hiscox after Lancashire warning

- Why soaring US Treasury yields are driving down stocks around the world

- Who is looking to connect with French Connection?

- Packaging sell-off ‘way overdone’, insist analysts

- Retailer QUIZ has questions to answer after major profit warning