Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

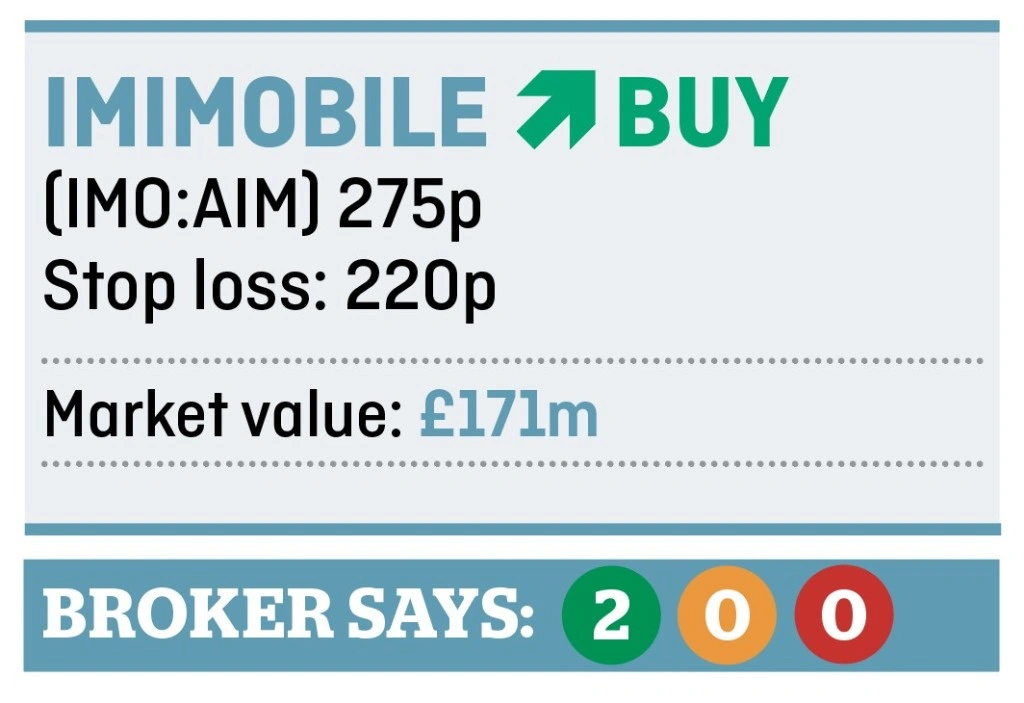

magazineSnap up digital economy winner IMImobile for potential big gains

Global commerce is increasingly shifting to online and smartphone applications and we anticipate IMImobile (IMO:AIM) will be a long-run digital economy winner.

The multi-channel customer engagement, marketing and commerce specialist is separated from its rivals thanks to a superior track record of consistency.

It has racked up growth in revenues, earnings before interest, tax, depreciation and amortisation (EBITDA) and pre-tax profit, all while throwing off impressive amounts of cash.

‘IMImobile is one of the most consistent performers in its peer group, mainly reflecting its geographic and sector spread, strong software products, and business-to-business focus,’ is how one analyst describes the company.

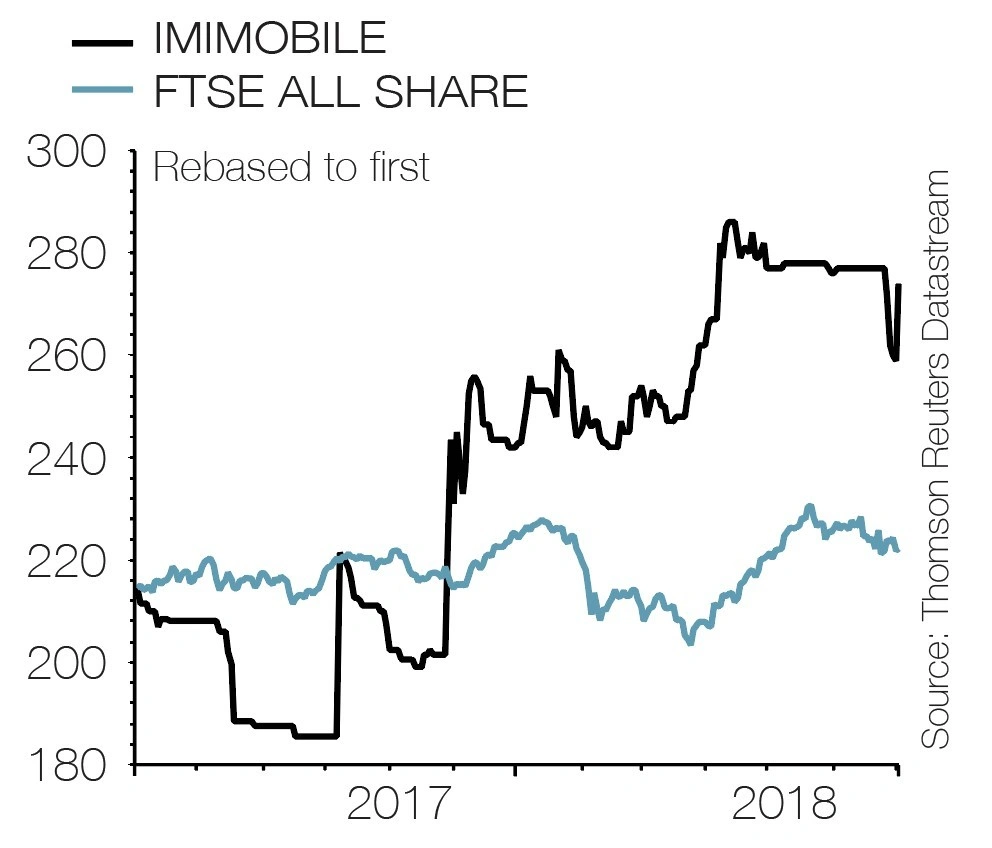

Full year results to 31 March 2018 were in line with already upgraded forecasts, showing revenue up 46% to £111.4m.

The fact it only managed 7% organic growth was largely down to challenging markets in the Middle East and Africa offsetting much better performances across the US, Europe and the Far East. Adjusted EBITDA of £13.4m was up 17% year-on-year and also beat consensus estimates.

IMImobile has been consolidating its position in the UK cloud communications space and growing its international operations through acquisitions.

Infracast, Sumotext and Healthcare Communications have been bought during the past year or so, adding considerable scale, bolstering financial services and healthcare expertise and allowing greater cross-selling across its client estate. Customers include Vodafone (VOD), BT’s (BT.A) EE business, British Gas-owner Centrica (CNA) and IBM.

Buying businesses does come with associated costs and IMImobile must constantly invest in its technology platform to keep it top notch.

It’s also worth noting the company’s habit of making hefty payments in stock, and while that has no effect on cash flow, it does help to explain the gap between adjusted and reported profit, which was £10.1m versus £2.7m last year respectively.

On 3 July it bought Canadian mobile engagement solutions provider Impact Mobile for £15.8m, a significant deal in terms of strengthening its footprint with North American mobile operators, retailers, government agencies and major household brands. That should equal more cross selling opportunities down the line.

The acquisition adds an extra £1.2m to forecast pre-tax profit both this year and next, according to Investec’s estimates, to £13.1m and £14m respectively. That implies a price-to-earnings multiple of nearly 19 falling to 17.6, hardly demanding by digital economy growth stock standards.

Investec calculates the stock will hit 400p over the next 12 months, implying 45% potential upside. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.