Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDiversified Gas & Oil doubles production with blockbuster deal

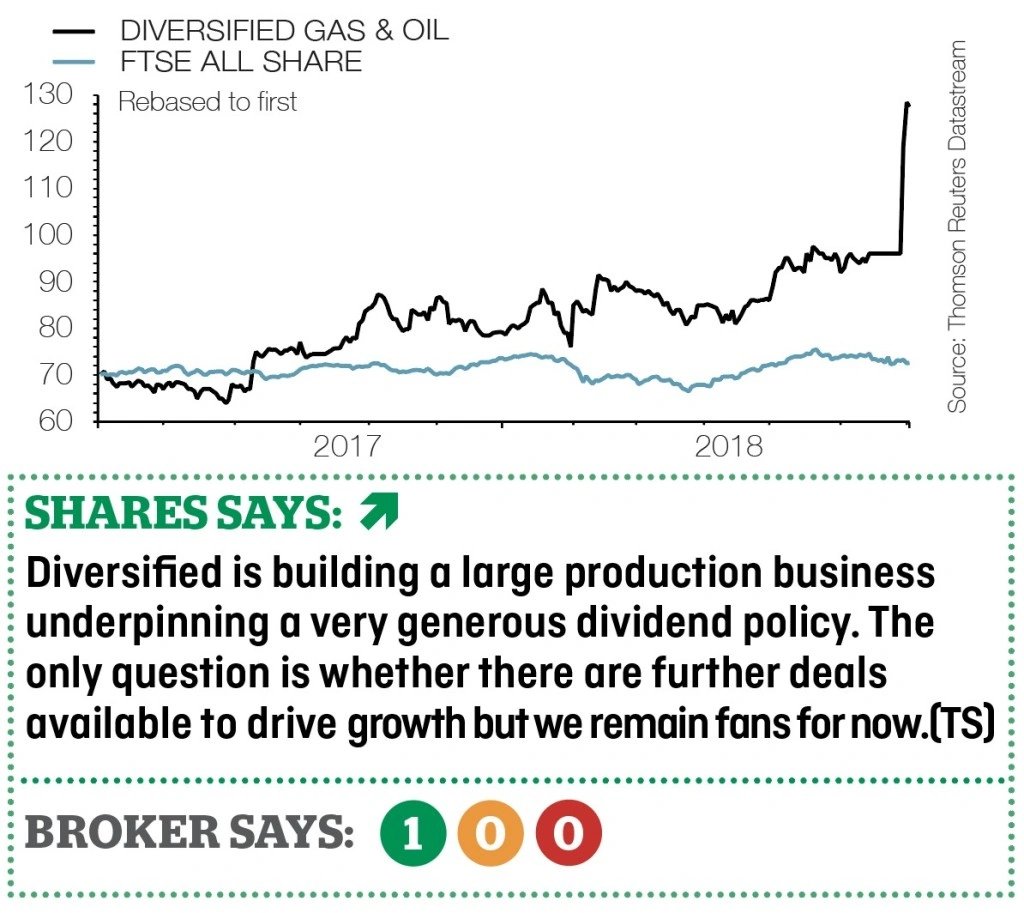

Diversified Gas & Oil (DGOC:AIM) 130p

Gain to date: 44%

Original entry point:

Buy at 90p, 22 February 2018

Our positive call on AIM oil producer Diversified Gas & Oil (DGOC:AIM) continues to be rewarded with the company completing its largest acquisition to date (29 Jun).

The $575m acquisition of assets from shale producer EQT is located in the company’s traditional base in the Appalachia basin and is expected to double output to 60,000 barrels of oil equivalent per day.

Sums by analysts at banking group Mirabaud suggest the deal will more than treble annual earnings and more than double the dividend payout with the market value of the group hitting $823m at the current share price.

The deal is being funded by placing $250m worth of new shares at 97p but shareholders are at least being heavily compensated for the resulting dilution. Back of an envelope calculations suggest the company could offer a dividend yield of nearly 7%.

This transaction is consistent with the company’s strategy of acquiring conventional (mainly) natural gas assets from big operators who are more interested in chasing the higher volumes associated with shale deposits.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.