Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSecond quarter update on our 2018 share portfolio

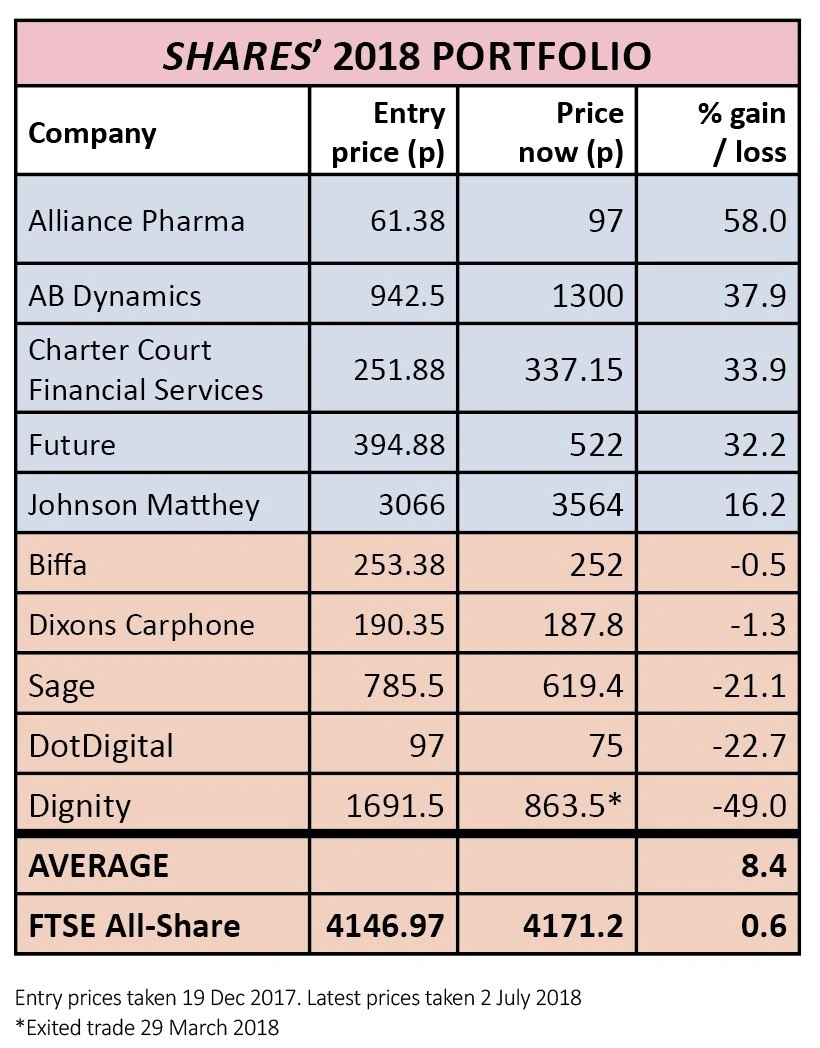

Our top picks for 2018 have on the whole enjoyed a superb second quarter, reversing the first quarter’s losses to now stand significantly ahead of the market.

The average gain from the portfolio is now 8.4% versus a mere 0.6% from the FTSE All-Share over the same period. This is a dramatic turn of events considering we were down by 8.4% on average at the end of Q1.

As a reminder, towards the end of December each year we pick various stocks in the belief they perform well over the following 12 months.

STOCKS IN FOCUS

The best performer in our 2018 portfolio is currently Alliance Pharma (APH:AIM), up by 58% to 97p. Its latest trading update revealed good growth from international brands Kelo-cote and MacuShield with overall trading in line with expectations.

Last month, morning sickness drug Diclectin was given the green light by regulatory authorities. Alliance Pharma expects approval to sell the product in the UK shortly. Numis analyst Sally Taylor believes the drug – which has been licensed by Alliance Pharma from Canadian group Duchesnay – has sales potential of over £20m over five years, potentially hitting £40m in peak sales in the longer term.

And on 19 June Alliance Pharma announced plans to acquire exclusive marketing rights to anti-dandruff shampoo brand Nizoral for £60m. It says the deal will materially enhance earnings in its first full year of ownership.

AB DYNAMICS looking good

Shares in AB Dynamics (ABDP:AIM) have burst back to life and are now 37.9% ahead of our entry point. The company recently won its first order for an advanced vehicle driving simulator, validating more than two years of development work with Williams Advanced Engineering.

Half year results published in April included 39% increase in revenue to £15.3m with chairman Tony Best saying the business had seen ‘an excellent start’ to the financial year.

CHARTER COURT IS ON A ROLL

Challenger bank Charter Court Financial Services (CCFS) is enjoying strong upwards share price momentum and our trade has now increased by 33.9% in value since we said to buy last December.

A first quarter trading update in May showed 28.2% year-on-year increase in its loan book to £5.5bn, plus customer deposits increasing by 16.2% to £4.3bn. Total Bank of England Term Funding Scheme drawings at the end of the quarter stood at £1.1bn.

‘Despite competitive pressure in the group’s core specialist mortgage market, we believe that the group’s highly efficient operating model, backed by its quick decision-making engine and well capitalised balance sheet, means that it is well placed to continue growing profitably and taking share,’ said Shore Capital analyst Gary Greenwood in May.

FUTURE HAS LEGS

Just as we hoped it would, publisher Future (FUTR) is keeping up the momentum it showed in 2017.

Results for the six months to 31 March revealed revenue up 25% to £51.1m. This was supported by M&A as the company feeds newly acquired titles into its transferable platform.

The publisher of Total Film and Tech Radar confirmed alongside the first half numbers that it was considering resuming dividends at its full year results in November.

SOME OF THE REST

Johnson Matthey (JMAT) continues to defy predictions of going ex-growth with its clean air business. Tighter emissions regulation should allow the business to grow at low double digits for at least the next four years, say analysts.

It is also making progress with its enhanced lithium nickel oxide material which could potentially disrupt the electric vehicle battery market. It’s been a good portfolio performer for us with 16.2% gain

to date.

Dixons Carphone (DC.) is also holding up relatively well despite several bits of negative news in recent months. A profit warning in May was followed by news of a cyber attack which saw a data breach involving payment card and personal data records.

THE LAGGARDS

Sage (SGE) started 2018 full of promise that it was finally about to accelerate growth yet the confidence shareholders invested in the accounting and enterprise software tools provider has so far proved mis-placed.

Organic growth remains stubbornly hitched to the 6% or so levels it has been doing for years and several analysts see little hope of that changing in the near future.

Sales execution and intense competition seems to be behind this sluggishness. The former is within management’s control, the latter may prove to be a more belligerent challenge.

Multi-channel digital marketing business DotDigital (DOTD:AIM) has been bogged down by short-term growth concerns, largely relating to new data regulations called GDPR which came into force in May.

Interestingly, new features released this year include things like the right to be forgotten, which should make its platform more, not less, relevant to modern marketeers.

The share price has remained out of favour since February’s half year results, but a trading update due in the next few weeks may well be the catalyst to put investor concerns to bed.

BIFFA BOUNCES BACK

Our patience with Biffa (BIFF) is starting to be rewarded with the waste expert recovering nearly all of its lost ground. Our trade was down 20.7% at the end of March as a result of a Chinese clampdown on importing certain recyclable materials which hurt Biffa’s earnings. Now it is only down by 0.5%.

Fortunately the business quickly found a way to adapt its business and reported decent full year results in June. Stockbroker Numis last month noted some improvement in the recyclate pricing market and implied a continuation of this trend over the coming months may trigger some earnings upgrades.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.