Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSummertime blues or sign of things to come?

A VIX index reading of 17.6 compared to a post-1990 average of 19.3, so the so-called ‘fear index,’ which measures expectations for future market volatility, is hardly blaring out a warning signal.

However, the indicator stood at just 9.2, almost a record low, on 3 January 2018, as optimism about the Trump tax cuts, accommodative central bank policy and hopes for a globally synchronised economic recovery took many stock markets to new peaks.

Since then, fear has crept steadily back into markets and the going has got tougher.

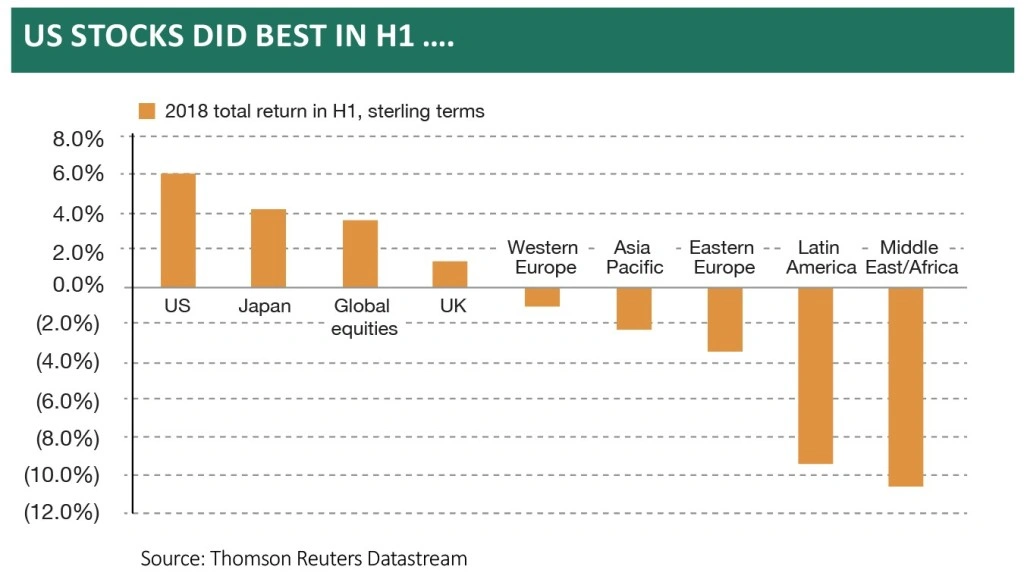

Analysis of total returns from key asset classes, continents and sectors, in sterling terms over the first six months of 2018, offers some potentially surprising trends.

Three stand out:

1. Equities and commodities may still believe in the inflationary, globally synchronised recovery but bond markets appear less convinced, especially if price action in the very long end of the market is any guide. At least one of them has to be wrong, in the end.

2. Emerging markets are taking a pounding, in terms of their currencies, bonds and equities and high yield bonds are making heavier weather of it.

This could smell of gathering risk aversion, especially after the hammering given out to cryptocurrencies and low-volatility strategies earlier in the year, to suggest money may be slowly starting to retreat from riskier, ‘peripheral’ markets to ‘core’ ones that are seen as safer propositions.

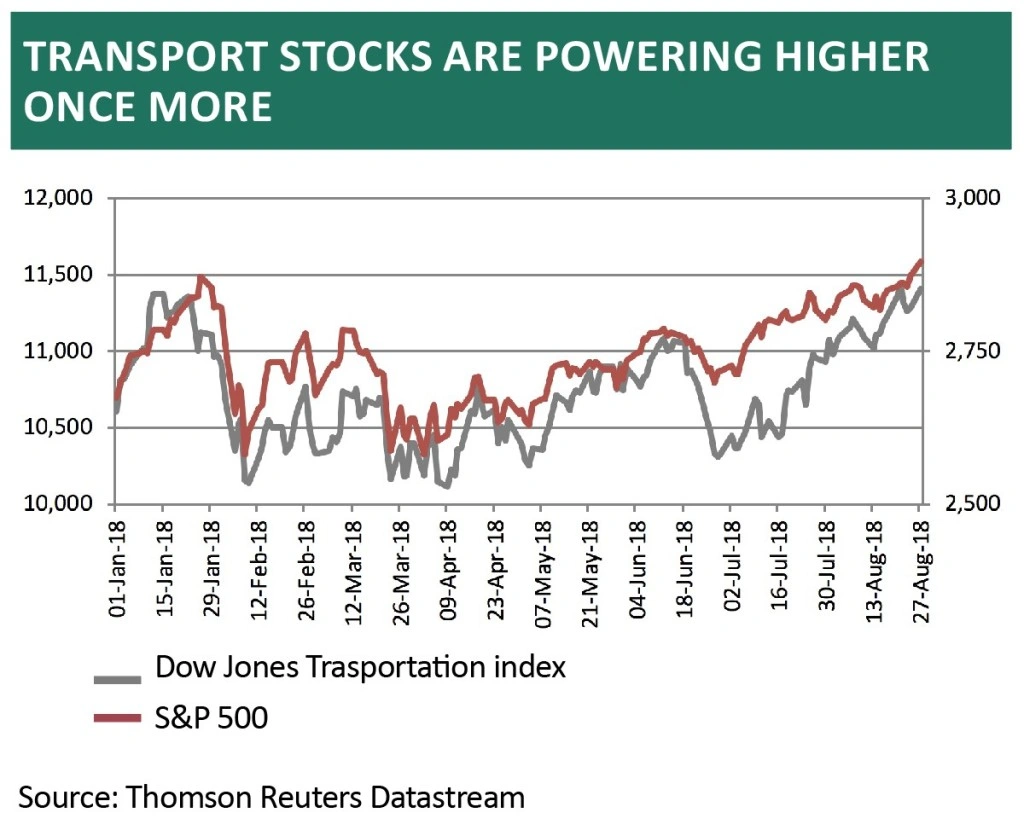

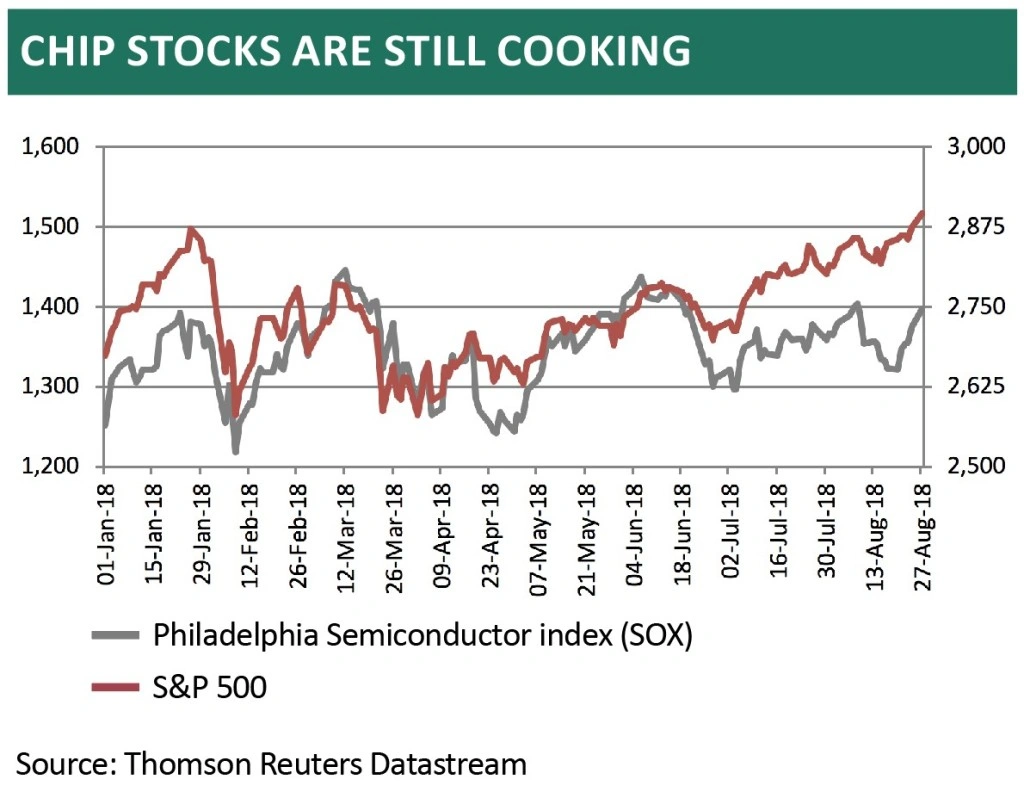

3. This shift could help to explain the ongoing strong performance of technology stocks on a global basis, as these firms as seen as largely immune from many of the geopolitical and economic questions which dominate today, owing to their dominant market positions.

Investors must still consider the issue of valuation and the dangers of paying any price for safety. After all, the more expensive an asset class becomes, by dint of its popularity, the more dangerous it becomes; as the experiences of the tech collapse of 2000-2003 and the fall from grace of the Nifty Fifty in 1973-74 imply.

None of this is to say investors should begin to panic. These shifts in sentiment may be no more than a case of the summertime blues which will wash away as soon as we get to St. Leger Day in September. Central bank policy also remains a key variable.

But it can be argued that the mood music is changing and while the market cannot always be right – it would be pretty hard for anyone to make capital gains if it were – its views should always be respected.

Performance breakdown

A swift analysis of four performance data tables helps to draw out the three themes above. In each case, the graphics show total returns in sterling terms and as such the pound’s second-quarter swoon helps to boost the figures offered by overseas markets. This is in itself a further issue to ponder with the future in mind.

The first chart shows how inflation and recovery were the dominant themes of the first half, especially early on. Commodities and stocks beat bonds.

Yet the bond markets’ returns had an unusual slant to them. Longer-term Government bonds did best (although yen strength against the pound could tilt the figures), high yield struggled, corporate bonds did poorly and emerging market fixed-income markets were flayed.

The strong showing by longer-term paper suggests fixed-income markets feel central banks may not raise rates as much as some think – or even if they do, a swift capitulation and return to rate-cutting and quantitative easing will follow, meaning that headline borrowing costs do indeed prove to be ‘lower for longer’.

If emerging market bonds hardly covered themselves in glory, their equity counterparts did even worse, moving swiftly from penthouse to outhouse, as they went from being 2017’s star performers (and the consensus pick for 2018) to notable laggards.

Currencies will have had a role to play here, even relative to an enfeebled pound, as Brazil, Turkey, South Africa and China all saw the counters weaken – and that is before the rout in Argentina is taken into account. Weakness in the Russian rouble and the Czech koruna (despite a run of four rate rises from the central bank) also caught the eye.

A booming US economy was not enough to lift all boats, particularly given fears over the rise of global protectionism, a particular concern for emerging markets.

America’s economic and market-might can also be seen in the global equity sector data and technology’s dominance of the sector listings

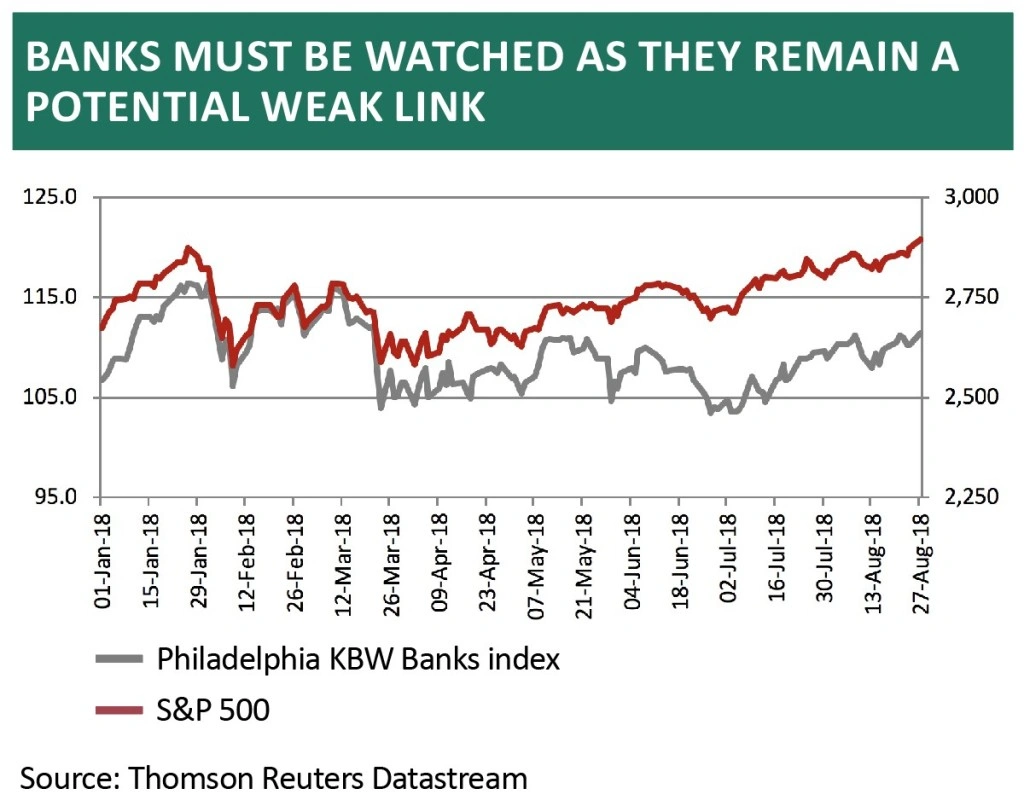

Energy stocks fed off a firm oil price. But neither industrials nor miners (under ‘materials’ on the table) nor financials made any headway, which looked odd in the context of broader bullish sentiment.

The failure of the financials in particular is a concern and their slump in the second quarter needs to be followed as it was their boom, bust and then recovery which have largely set the tone for global markets since 2003.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.