Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy Bankers Investment Trust has the right characteristics to thrive

Anyone concerned about toppy-looking equity markets, rising inflation and the uncertainties arising from Brexit may wish to look at The Bankers Investment Trust (BNKR). It has a range of characteristics which could potentially help beat the aforementioned pressures and deliver a positive outcome for investors.

Investing globally with a goal of generating higher long-term returns than UK investors could achieve in the domestic market, Bankers specifically aims to exceed the long-term growth of the FTSE All-Share Index and to grow its dividend ahead of the Retail Prices Index (RPI), one measure of inflation in the UK. It has increased its dividend every year for the past 50 years.

What is bankers' strategy?

Lead manager Alex Crooke, in place since 2003, aims to invest in attractively valued, cash generative firms that themselves pay a growing dividend. Crooke decides upon the trust’s geographical allocation and is also responsible for UK stock picking.

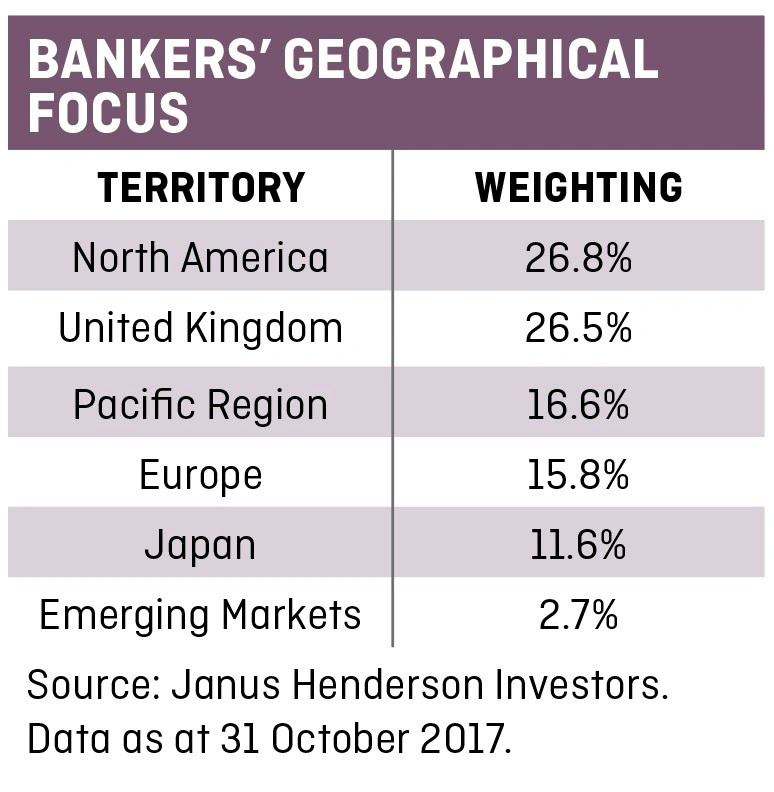

Bankers’ regional portfolios are managed by some of Crooke’s colleagues within asset manager Janus Henderson; they cover North America, Europe ex-UK, Asia Pacific, Japan and emerging markets.

All of Bankers’ fund managers follow a bottom-up stock picking approach and a value investment style. The investment trust is diversified with 197 holdings across geographical regions.

Bottom-up investing is an investment approach that focuses on the analysis of individual stocks and de-emphasises the significance of economic cycles and markets cycles.

‘We have the objective to grow the dividend ahead of RPI inflation,’ explains Crooke. ‘We don’t mind buying some growth stocks, but we have value bias to the stocks we try and own.’

How has it performed?

Managers of the aforementioned regional portfolios ‘all run their sleeves with the same value tilt’, continues Crooke, who adds that the team like companies with strong cash flow characteristics.

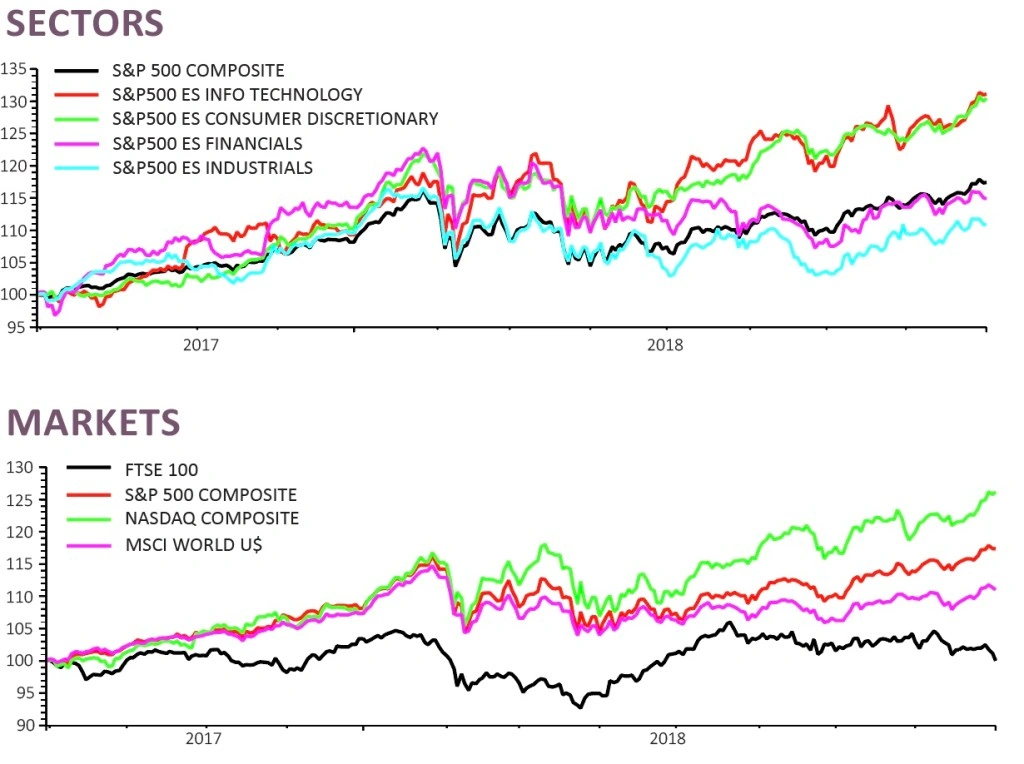

Reassuringly, Bankers has a strong long-term record of outperforming its FTSE All-Share benchmark in both share price and net asset value (NAV) terms, achieving its objective of compensating investors for the extra risk of investing outside the UK by achieving superior returns to the domestic market.

As at 31 October 2017, Bankers’ 10 year share price total return of 158.4% compares very favourably versus the 71% total return generated by the benchmark.

Investors must appreciate that past performance is not a guide to future performance. The value of an investment in Bankers and any income generated from the trust can rise as well as fall in value as a result of market and currency fluctuations.

What have the fund managers been up to?

The outlook for global equity investors is not without risk. Many stock markets around the world are testing new highs, notably in the US, while investors also need to be aware of geopolitical risks such as North Korea and the Brexit negotiations.

Against this backcloth, Bankers’ flexible approach to allocating between markets, and focus on cash-generative companies trading at attractive valuations, may find favour with investors.

‘In February, we took some money out of America and allocated funds towards Europe and China,’ recalls Crooke.

North America portfolio manager Ian Warmerdam pruned positions in highly valued US growth stocks, enabling Bankers to redeploy funds into Europe and Asia where valuations and yields were at a discount to North America.

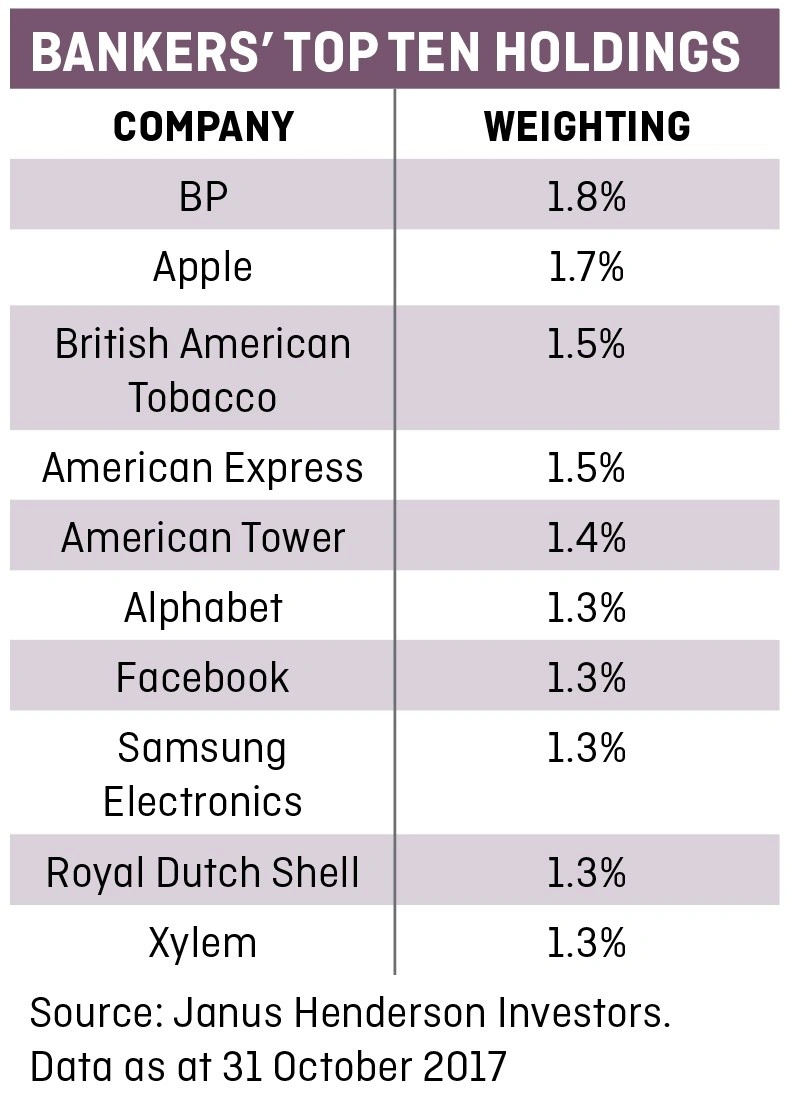

Nevertheless, among the exciting US growth names still nestling in the portfolio are iPhone maker Apple, Google’s parent company Alphabet and Facebook. Crooke is also bullish about the growth to come from credit card names American Express, Visa and Mastercard.

Which other stocks does it like?

Readers will perhaps be less familiar with another US company in Bankers’ top 10, though it offers a play on sustainability. Xylem is a global water technology company that takes its name from the tissue that transports water in plants.

‘It is the global leader in big filtration plants and desalination and should do well as water and environmental standards start to tighten up,’ says Crooke.

Another US growth stock held in the fund is Delphi Automotive, a producer of vehicle components for car makers which has just split into two companies; one producing powertrains, the other developing self-driving systems and similar new technology.

Delphi recently acquired self-driving start-up NuTonomy for $450m, a deal speeding up its plans to supply carmakers with autonomous vehicle systems. ‘We think the auto sector is quite cheap and there are opportunities to own the parts manufacturers,’ says Crooke, also invested in Japanese components and sensor systems giant TDK Corporation.

Reducing debt exposure

Gearing on the trust has been reduced to 3%, reflecting Crooke’s wish to bank some profits following strong equity market showings.

Gearing is the ability to borrow money to invest that money on behalf of shareholders and is a tool uniquely available to investment trust managers, rather than managers of open-end funds. Gearing represents the proportion of debt to equity. The net gearing ratio is calculated by dividing the total debt, including long and short-term liabilities and bank overdrafts, by the total shareholder equity.

Investment trusts often use debt to increase the pool of money from which they can make investments if they feel market conditions are favourable. Reeling in the debt position, as represented by the gearing ratio, can be a sign that a fund manager is more nervous about the near-term outlook for markets.

‘We think equities look good value and for patient holders there are good opportunities out there,’ Crooke explains, ‘but we’ve been keeping our powder dry. We did put some money into Japan and that has stormed forward.

‘There’s a slightly better tone to dividends,’ adds Crooke, flagging data from Janus Henderson that shows a surge in global dividends in the third quarter (Q3) of 2017, jumping 14.5% on a headline basis to $328.1bn, comfortably a Q3 record.

What's happening with some of Bankers' underlying holdings?

As the global economy continues its post-crisis normalisation, confidence is improving, many company’s profits are growing and income investors are benefiting as growth feeds through into higher dividends.

In the oil sector, where Bankers owns both BP (BP.) and Royal Dutch Shell (RDSB), Crooke insists ‘we are seeing the cash cover there improving – these dividends are better underpinned.’

Royal Dutch Shell in November 2017 announced plans to cancel its scrip dividend, introduced in early 2015 in the wake of falling oil prices, and return to delivering the payout entirely in cold, hard cash.

Scrip dividends are ones paid in the form of new shares. Companies occasionally go down this route to preserve cash. The downside is an increase in the number of shares in issue.

Though cautious on the UK consumer, Crooke owns JD Wetherspoon (JDW) ‘because it is the value proposition in the pub companies sector’.

He’s also been buying soft drinks group Britvic (BVIC) whose full year results (29 Nov 2017) revealed better than expected profits buoyed by cost savings as well as a surge in free cash flow.

‘We quite like a bit of restructuring as there’s the ability to benefit from earnings recovery,’ says Crooke, who has also been buying currently unloved UK pet specialist Pets at Home (PETS) as the company tries to improve its business and margins through restructuring. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Regulators take aim at trading platforms

- Purplebricks pasted on cost concern

- Heavyweights join OneMedia board

- Another video games developer joins stock market

- Tough festive trading to put retailers to the test

- UK water companies facing earnings, dividends pressure

- What does Disney-Fox deal mean for Sky shareholders?

Editor's View

Feature

Great Ideas Update

Investment Trusts

Main Feature

- Share pick for 2018: Future

- 10 superb stocks for 2018

- Share pick for 2018: DotDigital

- Share pick for 2018: Alliance Pharma

- Share pick for 2018: Johnson Matthey

- Share pick for 2018: Biffa

- Share pick for 2018: Dixons Carphone

- Share pick for 2018: Charter Court Financial Services

- Share pick for 2018: Sage

- Share pick for 2018: Dignity

- Share pick for 2018: AB Dynamics