Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineI’ve opened an ISA: now what do I do?

You have opened an ISA – congratulations, you have already taken one of the most important steps with investing, namely getting over the first hurdle.

This article will talk you through the next steps so you can start putting your money to work in the markets and hopefully grow your wealth.

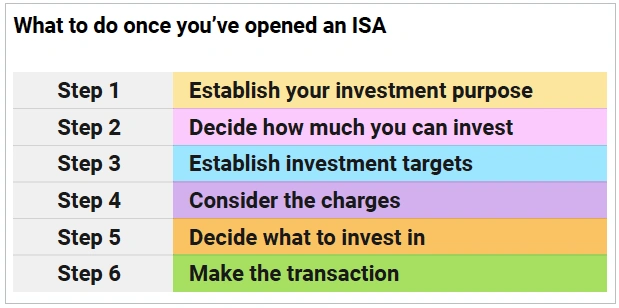

STEP ONE: ESTABLISH YOUR INVESTMENT PURPOSE

People invest for lots of reasons. If you are a parent you might want to invest for your child’s future whether that is for a college/university education, driving lessons or a deposit for their first home.

If you have just bought a new property, you might want to invest so you can carry out those home improvements you’ve always dreamed of – a new bathroom, kitchen, conservatory or garden room. You might even want to invest so that one day you can buy a holiday home.

Alternatively, you might want to start investing for the purposes of creating a ‘retirement nest egg’ if, for example, you are self-employed and do not have a workplace pension.

Whatever the reason for investing, it is important to understand it is a long-term activity. Five years is the minimum to allow you to ride out periods of volatility in the market.

Deciding on an investment goal should help you remain focused and by working backwards you can determine how much you need to invest in order to achieve it.

To calculate this, you need to appreciate there are two main ways to make money from investing.

One is through capital gains where the value of your investment increases to a level higher than the amount of money put into the market. You bank a profit when you sell the investment.

The other way to make money is through dividends from stocks and funds or coupons from bonds.

Your total return factors in the change in the value of your investments and the income generated from it.

Clare: investing £75 per month to save for a home deposit

Bournemouth-based Clare is a 25-year-old marketing consultant who has just opened a Lifetime ISA. She is able to invest £75 per month and hopes to increase this amount when she next gets a pay rise.

Clare is hoping by investing this amount she can save up for a deposit to buy her first home with her partner David.

The Government provides a 25% bonus on contributions to a Lifetime ISA up to £1,000 a year. Clare qualifies for £225 of free money in a year as a result of paying in £75 a month.

She decides to invest in Fidelity Index World Fund (BJS8SJ3). The fund aims to track the performance of the MSCI World index which encompasses more than 1,500 companies from stock markets in the developed world. Amongst its top holdings are tech giants Apple (APPL:NASDAQ) and Microsoft (MSFT:NASDAQ).

STEP TWO: DECIDE HOW MUCH YOU CAN INVEST

Before you start investing you need to decide how much you can invest. The lump sum or a regular amount can be as much or as little as you want – to suit your own personal or household budget.

For example, if you invested £75 a month over a five-year period and achieved 7.5% annual growth your investment could be worth just under £5,000 at the end. That assume 0.75% annual charges. That shows how little and often can add up to a decent amount over time.

STEP THREE: ESTABLISH INVESTMENT TARGETS

Let us say you have an investment target of £20,000. Starting from scratch over a five-year period with a 7.5% annual return and 0.75% charges, you would need to invest £281 per month to reach your target.

If this monthly amount is unrealistic, you may need to lengthen the investment period or rethink the size of your investment goal. Investing in riskier financial products to potentially achieve higher returns and meet your target could be counterproductive as the risk of losing money is higher.

Do not forget to consider the impact on inflation when working out your investment goal. For example, a loft conversion might cost £50,000 today, but it is likely to be more expensive in the future due to inflation.

While inflation is currently high, the Bank of England has a long-term 2% target. What this implies is that the cost of a loft conversion could go up by at least 2% each year. On that basis, you would need to target a minimum of £55,204 to cover the project cost in five years’ time, not £50,000.

STEP FOUR: CONSIDER ALL THE CHARGES

If you open a Stocks & Shares ISA, Lifetime ISA or Junior ISA with an investment platform there are various costs and charges which need to be factored into your planning.

For example, AJ Bell imposes an annual custody charge which is a fee for holding your investments. For shares, investment trusts, ETFs and bonds, this is 0.25% a year, capped at £3.50 per month. For funds, you pay 0.25% for the first £250,000 of assets, 0.1% for the next £250,000 worth of investments and nothing above £500,000.

For buying and selling investments there are costs associated with each trade. AJ Bell charges £1.50 for funds or £9.95 for all other types of investments including shares. The latter can fall to £4.95 per trade if you have done 10 or more share deals in the previous month. You can set up a regular investment service whereby you buy the share, investment trust, fund or ETF each month for £1.50 a trade.

You have to pay 0.5% stamp duty on UK-listed shares (excluding those on the AIM market) and there are also foreign exchange fees if you buy overseas-listed shares.

Funds have an in-built charge which is typically 0.1% to 0.2% for products that track an index or 0.75% to 1% for those where a fund manager makes all the portfolio decisions.

Jeff and Sharon: putting money into a tracker fund to grow their wealth

Jeff is a 41-year-old accountant, and his wife Sharon is a 38-year-old freelance designer. They have each opened an ISA with the intention of putting money into the markets and not taking anything out for as long as possible.

Jeff has a workplace pension with his employer but Sharon, who is self-employed, does not have a private pension. As it stands, she will be relying on the state pension when she turns 68 years old. Sharon wants to have an additional source of money later in life, so forms an investment plan.

Sharon decides to open a Lifetime ISA to benefit from the 25% Government bonus available with this type of investment account. She can afford to invest £300 a month which equates to £3,600 a year. That amount is topped up by an extra £900 from the Government bonus, meaning she has £4,500 a year going into the ISA. The bonus will be paid every year that she contributes money until she turns 50, and she can withdraw funds from the Lifetime ISA from the age of 60 without penalties.

Jeff wants the flexibility of being able to take out money whenever he wants, should an emergency crop up. For that reason, he opens a Stocks & Shares ISA where there are no restrictions on withdrawals. Jeff also decides to invest £300 a month but does not qualify for the Government bonus as that is not available with this type of ISA. He would not have been able to use a Lifetime ISA anyway, as the maximum age to open an account is 39 years old.

The couple want to focus on growing the value of their capital rather than generating an income today. They decide to invest in iShares MSCI ACWI ETF (SSAC), an exchange-traded fund. They use a regular investment service to qualify for a reduced dealing charge of £1.50 per trade.

This product provides exposure to companies of all sizes across 23 developed markets and 24 emerging markets countries for a low ongoing annual charge of 0.2%. It mirrors the performance of the MSCI All Countries World index.

STEP FIVE: DECIDE WHAT TO INVEST IN

Make sure you do your research before putting money into any investment. A good starting point is Shares – as a digital magazine we cover a range of investments as well as educational material to aid your understanding of the markets and investing.

Other useful sources of information include the personal finance and business sections of newspapers and your investment platform. For those serious about improving their investment skills, we have articles about useful investment books or you could look at financial data platforms including SharePad and Stockopedia which offer useful screening tools.

Not everyone wants to become an expert in investing and instead they would rather find the simplest way to put money into the markets. If that is you, starting with funds and investment trusts could be the most sensible option.

You benefit from diversification as you gain exposure to lots of different holdings rather than having your returns dependent on one or two individual shares. If something goes wrong with one or two investments in a fund, the rest of its portfolio should help cushion the blow and hopefully limit any losses.

A sensible starting point might be to invest in a handful of funds covering different markets and asset classes. Or, if you are only investing a modest sum, then you could look at a low-cost diversified global equity or multi-asset fund. For example, F&C Investment Trust (FCIT), Brunner Investment Trust (BUT) and Witan Investment Trust (WTAN) style themselves as one-stop shops for investors.

If you know the fund you want to invest in then, input the name into your platform and bring up the relevant page which will include information about its performance, fees and portfolio.

It is also worth checking which version of the fund you are buying – specifically whether it is the ‘inc’ (income) or ‘acc’ (accumulation) version? If you invest in the accumulation version of the fund then any income generated from the underlying investments will be reinvested back into the fund, while the income version will see dividends paid out to you as cash.

STEP SIX: MAKE THE TRANSACTION

For a one-off investment you will start by clicking on the deal or trade button. This places an order which is an instruction to buy or sell your chosen investment.

It is worth having enough cash in your account to fund any charges. If you do not then small bits of existing investments could be sold to pay these fees when they are due to be paid.

Before you invest in a fund, you will need to confirm you have read the necessary information about a fund including the Key Information Document or KID. This is a short document that provides important background about a fund which can help you decide if it is a suitable investment for you.

It often takes at a day for the order to buy a fund to be processed and completed. This means if you select to buy a certain number of units in a fund you will not know the total cost straight away, but you can also opt to buy units in a fund up to a certain monetary value.

For a transaction in shares, investment trusts and ETFs you will be provided with a time-limited quote to buy (or sell) at a certain price, reflecting the fact that their prices move around all the time. In a similar way to funds you can either select how much money or how many shares you want to trade. You will then be shown the total cost of the transaction.

Once you have clicked that buy button or set up your regular investment then congratulations, you have done it and you are a fully-fledged investor.

DISCLAIMER: AJ Bell referenced in the article owns Shares magazine. The author of the article (Sabuhi Gard) and the editors of the article (Daniel Coatsworth and Tom Sieber) own shares in AJ Bell. DC also invests in Fidelity Index World.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

News

- Why investors are excited about upcoming big tech results

- Hipgnosis Songs Fund at all-time low ahead of big vote on 26 October

- Coca-Cola shares have been weak heading into third-quarter earnings

- Pfizer hit by lower Covid vaccine demand but Novo Nordisk soars on weight-loss boost

- Computacenter shares still on a roll after upbeat financial results two months ago

- What do the latest US banking results tell us about the economy and markets?