Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy there’s more to Frasers than Mike Ashley, cheap tracksuits and trainers

Among the most resilient operators in a retail sector battling with inflationary pressures and the squeeze on household budgets is Frasers (FRAS), the FTSE 100 conglomerate controlled by retail tycoon Mike Ashley, which he founded in 1982 as a sports shop in Maidenhead.

There are many misperceptions about Frasers, which remains best-known as the company behind value-for-money trainers and tracksuits seller Sports Direct. What’s still underappreciated is how the business has moved way beyond its sporting goods roots to also become a premium and luxury retail powerhouse with attractive prospects.

Ashley, the swashbuckling entrepreneur often referred to as ‘the saviour of the UK high street’, has an appetite for a bargain and has helped to shape Britain’s retail landscape over the years by acquiring distressed businesses. Commentators have devoted pages to understanding his masterplan for the rapidly expanding Frasers’ empire.

Bulls argue the strategy is simple – acquire brands or businesses that help to expand the group’s skillset and customer reach. Bears argue the £3.5 billion business still needs to demonstrate the real value in its increasingly broad portfolio of companies, labels and brands which risks becoming unwieldy.

MISPERCEPTION #1: FRASERS IS BASICALLY SPORTS DIRECT, ISN’T IT?

Since its 2007 stock market flotation as Sports Direct International, Frasers has completed countless acquisitions under the stewardship of retail kingpin Ashley. Shore Capital points out these have typically been deals to acquire businesses out of administration, essentially buying them for pennies in the pound.

Already a dominant force in sporting goods through Sports Direct, Frasers is working towards becoming increasingly relevant in faster growing areas of the consumer space where there is a trend towards premium and luxury offers.

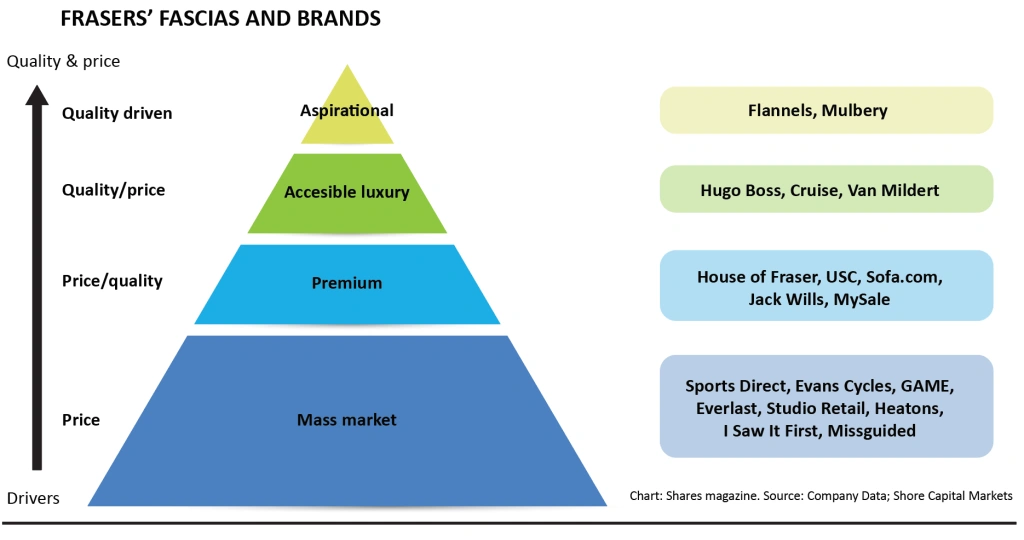

Present-day Frasers is a collection of the world’s most iconic brands and offers three core pillars – sports, lifestyle and luxury – through different banners including Sports Direct, luxury designer fashion chain Flannels and department store House of Fraser.

Its product range spans sports and leisure clothing, footwear and equipment – sporting brands include Slazenger, Lonsdale, Everlast, Karrimor and Kangol – as well as lifestyle and apparel products sold through department stores, shops and online. The Frasers empire also spans retailers and brands including Game Digital, Sofa.com, Evans Cycles and Jack Wills.

The sportswear-to-luxury brands group has also taken strategic stakes in companies ranging from high-end handbags group Mulberry (MUL:AIM) and German fashion brand Hugo Boss (BOSS:ETR) to ASOS (ASC) and N Brown (BWNG:AIM), interests which create new opportunities by allowing Frasers to develop relationships and partnerships with other retailers, suppliers and brands.

More recent acquisitions include fast fashion firms I Saw It First and Missguided, which should help it raise its digital game, the Australian online retailer MySale and the Savile Row tailor Gieves & Hawkes. Frasers has even scooped up some premium fashion brands from arch-rival JD Sports Fashion (JD.).

THE DICK’S SPORTING GOODS OF EUROPE

Shore Capital says with supportive industry tailwinds and evidence of a demand for luxury from customers less exposed to the cost-of-living squeeze, it forecasts a continuation of the strong recovery from the Covid disruption experienced in recent years.

While many investors still mistake Frasers as a seller of cheap socks, footballs, basketballs and running shoes, today’s Frasers is a best-in-class retail conglomerate working with many of the world’s top brands.

These include Nike (NKE:NYSE), Adidas (ADS:ETR), Skechers, Asics and Puma (PUM:ETR) in sports and premium brands such as Hugo Boss, Moncler (MONC:BIT) and Mulberry. In fact, the company is focused on ‘elevating’ its proposition by smartening up its stores and tightening its supplier relationships to receive a better product allocation from the world’s winning brands.

Shore Capital makes the point that like the well-managed Dick’s Sporting Goods (DKS:NYSE) in the US, Frasers is becoming Nike’s ‘partner of choice’ in the European sporting goods market and is benefiting as the big footwear brands rationalise their wholesale accounts.

Admittedly, sporting goods is a mature part of the consumer industry and has been the slowest growing part of Frasers in recent years. The real growth opportunity for Frasers lies in expanding deeper into the premium and luxury areas. ‘These are much faster-growing markets, where consumers are less exposed to the cost-of-living squeeze,’ stresses Shore Capital.

MISPERCEPTION #2: DOESN’T MIKE ASHLEY STILL RUN THE SHOW?

Yes and no. Four decades after starting his retail empire, Ashley stepped down as Frasers’ CEO in May 2022, though he remains on the board as an executive director and still holds 72% of the shares, so his influence is undeniable.

Ashley remains a key advisor and major shareholder, and current CEO Michael Murray is his son-in-law – not great from a corporate governance perspective perhaps, but Murray’s early successes have proved Frasers can thrive without Ashley at the wheel.

Murray’s previous role as ‘head of elevation’ is helping him to take the group more upmarket through a strategy delivered organically and through selective acquisitions.

‘Elevation’ is widening Frasers’ economic moat and broadening its exposure to higher-end brands, making its offer increasingly appealing to its customer.

Many have questioned Frasers’ mergers and acquisitions transactions and Murray has promised a refocused strategy and deals that enhance margins. He is also likely to pursue a less combative approach with the investment community than his father-in-law.

ARE FRASERS’ SHARES WORTH BUYING?

Shore Capital recently initiated coverage with a ‘buy’ rating and £12 fair value estimate, implying 60% upside from current levels. The broker enthused: ‘Frasers’ diversification and the elevation strategies, coupled with tailwinds in luxury, should drive resiliency into calendar year 2023.

‘Deep value investments in the retail space over the past few years position Frasers well to weather the storm and we expect margins to grow in tandem.

‘In addition, following the strategic geographical expansion in Europe, we estimate Frasers could deploy up to £2 billion, putting it in a strong position to extend its lead and “own” the sporting segment of the EU sportswear sector.’

While Frasers doesn’t pay a dividend, it does have a reputation as an excellent capital allocator that uses its free cash flow for acquisitions as well as share buybacks which have significantly increased per share business value.

Results for the six months to 23 October 2022 revealed the positive strategic and trading momentum behind Frasers, with revenues rising 12.7% to over £2.6 billion, reflecting acquisitions and strong sales growth from premium fascia including Flannels.

Frasers also reiterated its full year 2023 guidance for adjusted pre-tax profits of between £450 million to £500 million, with the company encouraged by the effective elevation strategy under Murray’s leadership.

The shares trade on single digit multiples of forward earnings, a discount to peers Shore Capital views as ‘unjustified’ given the company’s strengthening market position and the fact that it offers exposure to the buoyant luxury sector and a high level of diversification within the consumer space.

Liberum Capital says there are very few companies generating adequate cash flow that can accommodate the scale of investment in Frasers’ core business, expand organically and through M&A, and return capital to shareholders.

‘Considering this optionality, such strong momentum and the levers for future growth, we see the shares as cheap,’ it concludes.

‘A sum-of-the-parts for UK sports, the value building within Flannels, strategic stakes (Hugo Boss, Mulberry) and other key brands (including Everlast) is very compelling when set against the current market cap.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

Investment Trusts

News

- Marks & Spencer builds on sparkling Christmas with news of 20 new stores to come

- Darktrace back to IPO price after slicing growth expectations

- UK stocks enjoy big gains as travel and retail lead the way

- Housebuilder warnings about a slowdown in activity does not bode well for suppliers

- Musicmagpie shares soar more than 300% from October lows