Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineReasons why it pays to invest in small caps despite recent sell-off

Following on from the pandemic and war in Ukraine, UK stocks are being buffeted by headwinds from hot inflation, rising rates and the cost-of-living crisis. But it is UK small and mid-cap investors that have endured the toughest period over the past year, with the small cap, mid cap and AIM indices all suffering severe setbacks.

The good news, however, is this sell-off has created opportunities across a cohort of quality smaller companies with attractive growth prospects that now trade at valuations significantly lower than their recent history. And the set-up is more compelling when you remember that historically, UK smaller companies have outperformed larger stocks over time.

SMALL CAP DISCOUNT

Kirsty Desson, manager of the Abrdn Global Smaller Companies Fund (B777SP3), stresses that small cap performance has varied in different global markets.

She says small caps have only marginally underperformed large caps year-to-date. ‘If you look at the MSCI World index, that’s down around 23% now and the MSCI World Small Cap index is down 24%, so only marginally weaker.

‘What is certainly true is that valuations for small caps are still at quite a significant discount to large cap peers and that has been consistent for some time, really since Covid.’

This popular UK small cap index has delivered 1,016% total return since September 1990...

... but the performance hasn’t been great over the past 12 months

Despite prevailing risk-off sentiment, Desson argues investors should at least start thinking about an allocation to the small cap sector, one perceived as riskier than the large and mid-cap universe.

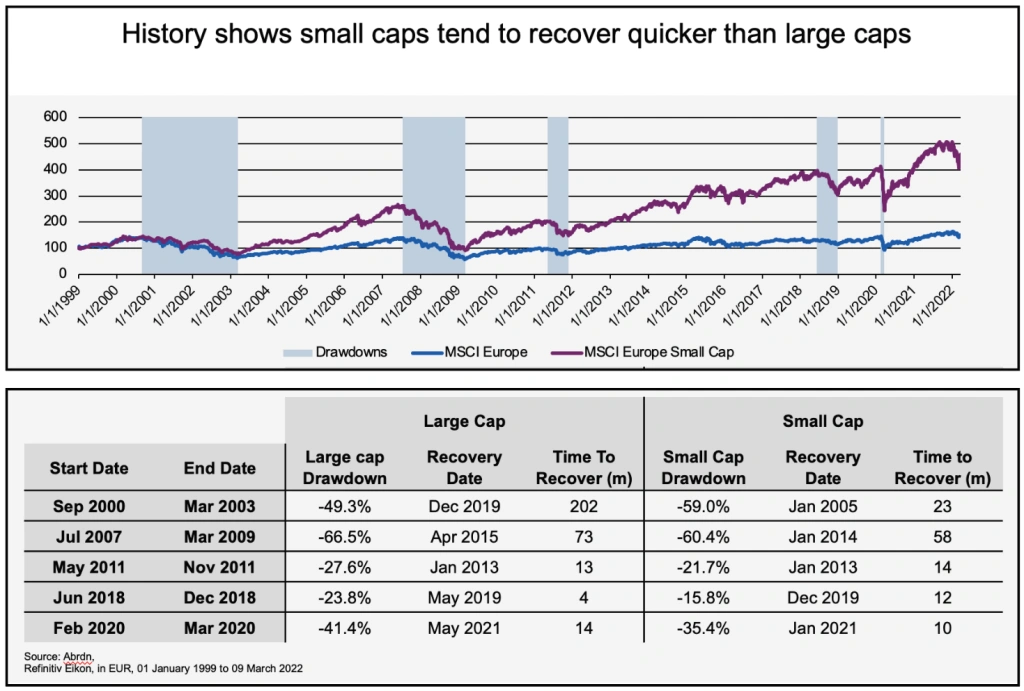

She points out that in the periods coming out of the downturns triggered by the bursting of the tech bubble and the 2008 financial crisis, from the trough, small caps dramatically outperformed large caps in both those periods. ‘While it is difficult to have a crystal ball, investors do want to be in small cap names coming through into a recovery.’

BARGAINS GALORE?

Jonathan Brown manages Invesco Perpetual UK Smaller Companies (IPU), an investment trust trading at a 18.7% discount to net asset value which demonstrates how out of favour corporate small fry are at present.

Brown thinks the small cap sector is very cheap at the moment, whether you compare it to valuations it has traded on historically or other global indices.

Paul Marriage, manager of TM Tellworth UK Smaller Companies Fund (BDTM8B4), says the small cap discount to large cap is deeper now than in 2008. He adds: ‘Stocks were sold off heavily in 2008. But what’s happened this year is things have been sold off heavily, but small caps have been sold off more, though absolute valuations aren’t quite down to 2008 levels.’

Marriage bemoans the fact that the small cap sell-off has been ‘pretty indiscriminate’.

‘AIM has underperformed the large and mid-cap indices and is in a pretty horrible place, and most small cap funds including us have got plenty of AIM, but we’re negotiating that okay.’

He says certain companies are being valued as if they won’t exist in five years’ time. Yet he sees opportunities to find some that should be around in 2027 and may also be a lot more valuable by then.

Like Desson, Marriage makes the case for allocating to small caps for a recovery. ‘Typically, when people get more risk-on, the first things to go up would be more liquid, easier to buy mid-caps. And then small caps have what I describe as an “Andrex rally”. You know, “stronger for longer”, because they start at a lower place.’

Ken Wotton, manager of UK small caps trust Strategic Equity Capital (SEC) and co-manager of the LF Gresham House UK Smaller Companies Fund (BH416G5), argues the longer-term opportunity within British small caps is ‘extremely compelling’ at present. He says: ‘There remain scores of high-quality, resilient businesses on offer, and the agile demeanour and niche positioning of smaller caps may allow these companies to navigate more smoothly through broader economic headwinds.’

Wotton says the fall in valuations and current sterling weakness relative to the US dollar has made UK small caps attractive to foreign investors and investors could see companies acquired at highly attractive multiples over the coming months.

LATEST INVESTMENTS

The biggest holdings of £1.2 billion Abrdn Global Smaller Companies Fund include payroll firm Paylocity (PCTY:NASDAQ), swimming pool supplier Pool Corp (POOL:NASDAQ) and video game industry services company Keywords Studios (KWS:AIM).

The fund focuses on three key factors; quality, growth and momentum, as Dessen says stocks with these characteristics have the greatest likelihood of outperforming.

‘In small caps, we find that stocks that are unprofitable, blue sky or don’t have a sustainable growth outlook, those are the companies that have the greatest amount of risk.

‘In terms of delivering the most optimal risk-adjusted returns, we like companies with good quality metrics, so solid balance sheets, decent cash flows, strong margins, defendable competitive advantage and solid ESG.’

New names added to the fund’s portfolio this year include Carlisle (CSL:NYSE), one of the largest roofing repair companies in the US with around 30% market share which ‘does a lot of insurance and commercial work and still has a huge backlog, meaning the earnings outlook is very well supported for the next year’.

Desson’s other new buys in 2022 include Japan-listed Sho-Bond (1414:TYO), an expert in the maintenance of roads, bridges, tunnels with a steady income stream where the money stems from the government. ‘That stock has been doing very well for us,’ says says.

The fund also invests in Australia-based building company Johns Lyng (JLG:ASX), a contractor that rebuilds and restores properties after damage after insurable events such as weather and fire damage.

UNDERSTANDING THE PROCESS

Tellworth UK Smaller Companies Fund typically invests in companies in the £100 million-to-£500 million market cap range. The £247 million fund uses an investment process called ‘P3M’, which seeks to encompass the characteristics desired in a company and stands for ‘product, market, margin and management’.

Its holdings range from engineering, environmental and strategic consultancy Ricardo (RCDO) and content creation-focused hardware and software firm Videndum (VID) to P3M exemplar AB Dynamics (ABDP:AIM), a ‘world leader in testing driving systems that keeps on delivering’ in terms of organic growth and earnings upgrades, according to Marriage.

Teleradiology company Medica (MGP), one of the UK’s leading outsourced scanning businesses which is saving the NHS money, has caught the fund manager’s attention. The shares are currently trading on less than 13 times next year’s expected earnings. Marriage believes historically the market would have paid a much higher multiple for the type of defensive growth on offer.

The fund manager recently invested in Team17 (TM17:AIM), the video games developer and publisher which Marriage describes as looking like ‘a good company at the wrong price’ at the point he bought its shares. ‘We had watched the share price halve after a poorly managed placing earlier in the year.’

A new position for Invesco Perpetual UK Smaller Companies is identity data intelligence platform provider GB Group (GBG:AIM), which Brown has added to the portfolio over the last few months. That looks fortuitous timing as it recently received a takeover approach and there is chatter that more than one party is interested in buying the company.

‘GB Group had previously sold off very heavily, which prompted us to get involved and its recent takeover approach doesn’t surprise us,’ says Brown.

‘A lot of these businesses are trading at low valuations and if you look at what’s happened to sterling, things look especially cheap if you are a US buyer, for example. Hopefully there will be competing offers for GB. It is a business that we would hope to hold for many years, so it would have to be a good offer to prise it from our hands.’

COMING BACK INTO FASHION

Keywords Studios has been a popular stock for small cap funds to own over the years, but it hasn’t always enjoyed a rising share price.

‘It’s a stock we’ve held since IPO quite a few years ago now and we took a lot of profits 18 months ago. Keywords has since derated a long way, but the business is still trading very well,’ says Brown.

The fund manager says Keywords is benefiting from growth within the computer games sector but also from increased outsourcing. ‘We think the business has the potential to grow for many years to come.’

UNDERSTANDING THE OPPORTUNITY

Anna Macdonald, one of the managers of the TB Amati UK Listed Smaller Companies Fund (B2NG4R3), is a fan of Learning Technologies (LTG:AIM), which has become, through organic development and acquisitions, a market leader in digital learning and talent management.

It comprises a Software and Platforms division that sells multi-year software-as-a-service licences to enterprises. The other division, Contents and Services, delivers fixed price projects to clients, and grew substantially on the addition of GP Strategies in 2021, where the team has doubled margins, while growing sales.

‘While corporate training spend is normally correlated to GDP growth, we believe Learning Technologies has resilient sector exposure,’ says Macdonald. ‘For example, the CEO says that GP Strategies has served General Motors for 40 years, and the automotive industry is caught “in the eye of a change storm”, as the way we make and consume cars requires completely different market training and change management.’

Macdonald adds that a free cash flow yield of more than 8% is compelling for an AIM-listed business-to-business operator generating 75% of revenues in US dollars.

As for Ken Wotton, he has recently boosted Gresham House UK Smaller Companies’ holding in high margin motor insurer Sabre Insurance (SBRE) in the belief ‘there could be material capital growth ahead’ for a company which dominates the premium and hard-to-insure vehicle categories and which pays a substantial dividend. ‘Its competitive advantage lies in proprietary data processes and intellectual property, leaving Sabre Insurance less vulnerable to wage inflation,’ he adds.

DISCLAIMER: Editor Daniel Coatsworth owns units in Abrdn Global Smaller Companies Fund and TM Tellworth UK Smaller Companies Fund

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

- Ruffer delivers positive return in difficult times but sees more pain for investors

- Ideal time to invest in life sciences cheaply through this trust

- Essentra's transformation to a pure-play industrial supplier is now complete

- How Crestchic is powering up for a growth push and why now is a great time to buy

Investment Trusts

News

- Will Porsche shares surge like Ferrari or skid like Aston Martin?

- Resilient Greggs holds firm on outlook in good start for Roisin Currie

- FTSE 100 firms set for record cash return in 2022 but pressures are mounting

- Find out which stocks surged and slumped during a turbulent third quarter

- Why dollar strength and foreign exchange volatility is bad for stock markets