Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineHow Crestchic is powering up for a growth push and why now is a great time to buy

The market is picking up on the reality that Crestchic (LOAD:AIM) is a transformed business with real momentum behind it. With the valuation remaining attractive we think investors should buy the stock.

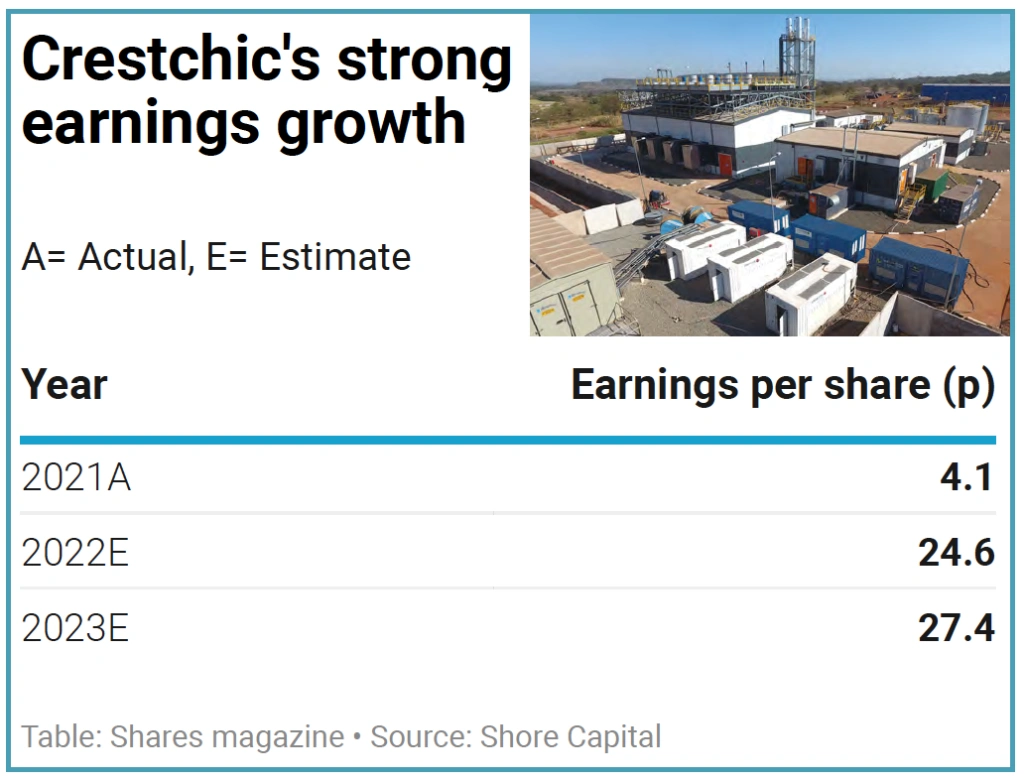

Despite a 40% rally in the shares over the past three months, with the company delivering its fourth earnings upgrade of 2022 alongside its first-half results, the shares still trade on just 9.9 times Shore Capital’s latest earnings per share forecast for 2023.

Crestchic has been on a journey. Formerly known as Northbridge Industrial Services, the company sold off its Australian oil drilling tools business Tasman in March 2022. This left the focus entirely on its load banks business.

Load banks are equipment used to test power systems and Crestchic manufactures, sells and rents them out to clients across the UK, Americas, Europe and Middle East – it is a market leader.

They can be permanently installed at a facility to be connected as required or portable versions can be used for testing standby generators and batteries. Its customer base includes data centres, oil, gas and mining operations as well as renewable power and marine facilities where a loss of power could result in significant financial and reputational damage.

Data centres, linked to the exponential growth in the cloud computing sector, are an increasingly important end market for Crestchic, with Shore Capital estimating they accounted for 30% of revenue in 2021. According to market research and consulting firm Precedence Research data centre construction is expected to enjoy a compound annual growth rate of 6% between 2021 and 2030.

Having signed a lease on a new rental depot in Texas and appointed a business development manager in the US, the company is poised to

take advantage of demand in a large US data centre market.

The disruption to the energy sector created by the war in Ukraine has increased demand for renewables, a sector where load banks are often crucial to testing back-up and storage facilities required to mitigate the intermittent nature of these power sources.

Servicing demand should be easier thanks to an 60% increase in capacity at its factory in Burton-on-Trent. An improved balance sheet and strong cash generation should also enable the company to invest in its rental fleet and drive organic growth.

Net debt stands at £1.5 million. The company returned to paying dividends earlier this year, with scope to surprise on the upside on this front given Crestchic’s strong financial position.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

- Ruffer delivers positive return in difficult times but sees more pain for investors

- Ideal time to invest in life sciences cheaply through this trust

- Essentra's transformation to a pure-play industrial supplier is now complete

- How Crestchic is powering up for a growth push and why now is a great time to buy

Investment Trusts

News

- Will Porsche shares surge like Ferrari or skid like Aston Martin?

- Resilient Greggs holds firm on outlook in good start for Roisin Currie

- FTSE 100 firms set for record cash return in 2022 but pressures are mounting

- Find out which stocks surged and slumped during a turbulent third quarter

- Why dollar strength and foreign exchange volatility is bad for stock markets