Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAftershock: what could happen next after the mini-Budget earthquake

The UK market remains in turmoil as the aftershocks unleashed by the mini-Budget earthquake on 23 September continue to rumble.

Despite the Government’s U-turn on the 45% tax cut, investors are still wondering what will happen next with gilts, the pound and companies in their portfolio.

In this article we look at some of the areas which might be most affected and discuss the stocks and sectors which are most at risk.

CHAOS UNFOLDED

It is hard to overstate the events which have transpired since chancellor Kwasi Kwarteng delivered his mini-Budget. The pound hit a new record low against the dollar, yields on the five-year gilt were briefly trading at five times their level at the start of 2022, the Bank of England pumped £62 billion into the system to maintain financial stability and the mortgage market has seen products withdrawn left, right and centre.

While the long-term impact is hard to determine, in the short term it will be more expensive for consumers, business and the Government itself to borrow and the valuations of different asset classes will be affected. The Bank of England is likely to introduce a big rate hike at its next meeting on 3 November, if not before.

Why the Bank of England intervened

Since the start of the year UK 10-year gilt yields have increased from around 1% to 4%, reflecting the Bank of England’s aggressive hike in interest rates to dampen rampant inflation.

Periods of stress often reveal previously obscure pressure points. That happened on 28 September when the Bank of England was forced to start buying gilts. The immediate catalyst was a risk that pension funds which had invested in liability-driven investment swaps – financial products linked to the gilt market – might become insolvent.

The central bank’s temporary purchase of longer dated gilts to stabilise market conditions is a stop gap measure to allow the long end to function normally rather than a stimulus to the financial sector.

Rather confusingly the Bank of England still intends to go ahead with quantitative tightening (reducing its balance sheet) at the end of October, namely selling gilts.

STOCK MARKET DOMINO EFFECTS

The negative reaction of bond and currency markets to the mini-Budget has a big influence on UK stock markets.

For years companies and their shareholders didn’t need to worry too much about financial leverage for two simple reasons.

Persistently low interest rates meant companies could service much higher debts while the Bank of England’s quantitative easing policy meant refinancing was easier to achieve.

Companies will now find it harder to refinance their debts while inflation continues to challenge margins. The cost of servicing debts will rise and eat up more cash, reducing profits.

The firms most at risk will be those which have high financial leverage and low operating margins.

One additional factor to consider is operational gearing. Even a small drop in revenues can have a big impact on companies which have relatively high fixed costs. These are harder to cut during a downturn, which means profit margins are squeezed.

Companies with already wafer-thin margins are particularly at risk of falling into losses.

Shares has used Stockopedia software to screen for companies with high leverage, low margins and high operational gearing.

From the initial list adjustments have been made to reflect only interest-bearing debt by removing lease-based debts. Although high inflation may result in higher lease costs in future, the focus is on companies’ current ability to service debts.

The key metric used to measure financial leverage is net debt to EBITDA (earnings before interest, tax, depreciation, and amortisation). Companies with ratios close to three and above are considered more vulnerable to rising interest rates.

However, each company’s circumstances are relatively unique. The maturity profile of the debts, whether they are owed to banks or bond investors, and the strength of relationships are all factors to be weighed.

Talking a snapshot in time does not always reflect the full picture. For example, pub groups JD Wetherspoon (JDW) and Marston’s (MARS) have not yet fully recovered from the pandemic, so the latest EBITDA does not reflect ‘normal’ trading. In addition, both firms have well invested freehold estates which banks are generally more comfortable lending against.

To give an idea of the scale of adjustment some companies will need to make to account for higher costs of borrowing, look at car retailer Motorpoint (MOTR). In January it negotiated a new £29 million revolving credit facility which expires in May 2024. The average interest rate paid on its debts last year was 1.4%. The new credit facility looks well timed because UK interest rates have gone up more than four-fold since it struck that deal.

WHAT THE BIG MORTGAGE SQUEEZE MEANS FOR CONSUMER-FACING COMPANIES

One of the most immediate impacts on ordinary people of recent events has been chaos in the mortgage market where some products have been pulled entirely and rates have been moving steadily higher.

This is bad news for the housing market as it will make it more difficult for people to get on the ladder in the first place and more expensive for people to move home, with predictions for a significant crash in house prices. This has been reflected in the weak share price performance for housebuilders and property portal Rightmove (RMV).

Anyone coming off a fixed-rate mortgage deal is likely to face a big increase in their monthly payment, likely running into hundreds of pounds.

This will leave them with significantly less disposable income and will therefore have an impact on consumer-facing businesses. Most insulated are those, principally the supermarkets, which sell staples like food and household goods.

That doesn’t mean they won’t face any pain at all – trolleys are likely to be less full. Ocado Retail, the joint venture between Ocado (OCDO) and Marks & Spencer (MKS), reported average basket sizes fell 6% in the three months to 31 August, even before the current turmoil. This has implications for the profitability of online grocery operations where the costs of delivery are the same, regardless of how much people are ordering.

If they can afford it individuals may prioritise spending on getting away given the enforced hiatus on holidays during the pandemic. The weak pound and the high costs of jetting abroad may see more people pursue staycations, with the owner of low-cost hotel chain Whitbread (WTB) a potential beneficiary. The likes of travel operator TUI (TUI), British Airways operator International Consolidated Airlines (IAG) Jet2 (JET2:AIM) and EasyJet (EZJ) could see a recent recovery in demand knocked off course.

Eating out and takeaways may become less frequent due to affordability which is bad news for the likes of Restaurant Group (RTN), Deliveroo (ROO) and Just Eat Takeaway (JET). Socialising at pubs, bars and nightclubs could also suffer as people tighten their belts.

Both eateries and pubs face a significant impact from rising energy costs. All Bar One owner Mitchells & Butler (MAB) recently warned of an 88% increase in its heating and utility bills for 2023 compared with the pre-Covid level.

Retailer Next’s (NXT) profit warning on 29 September, with full price sales expected to be down 1.5% in the second half of its financial year to the end of January 2023, suggests no-one selling discretionary goods right now is safe.

You can read about the retail businesses which look most resilient and most vulnerable in this article. Strong balance sheets and a compelling offering to shoppers are an absolute must in such difficult conditions.

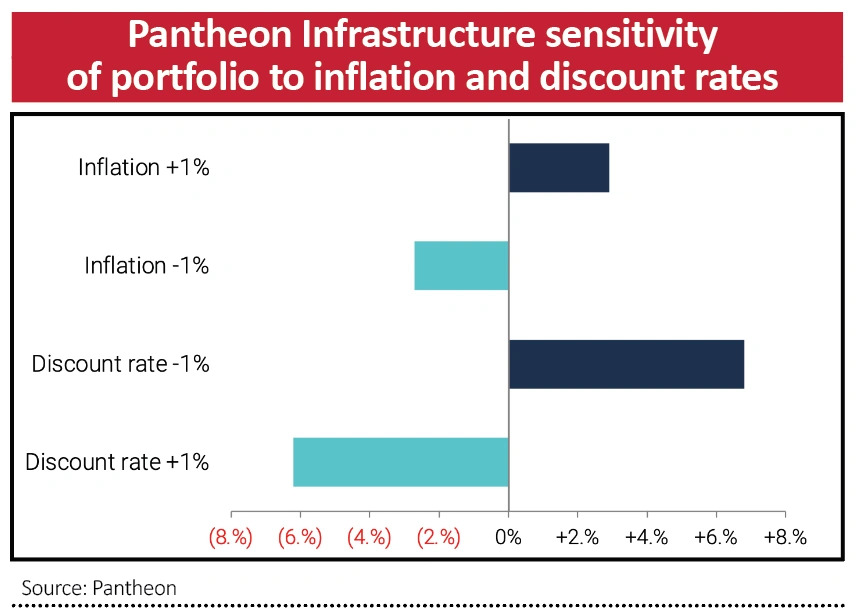

WHY REITS AND INFRASTRUCTURE TRUSTS FELL

Real estate investment trusts (REITs for short) and infrastructure trusts have been heavily sold off in the wake of the mini-Budget as the market has adjusted to higher discount rates for long duration assets.

Two key elements make up the discount rate. First you have the risk-free rate which is typically taken as the yield on government bonds. Then there is the risk premium – the part which reflects the risk associated with investing your money. The risk-free rate has soared and this has been reflected in falling net asset values.

In discussions with infrastructure funds ahead of the mini-Budget, most observed to Shares that discount rates had remained relatively stable despite rising rate expectations, and they argued this stability reflected the strong appeal of the asset class.

The mini-Budget appears to have changed the calculus. The sensitivity analysis from Pantheon Infrastructure (PINT) shows the impact of inflation and discount rates on its portfolio, and this should be a good proxy for the wider infrastructure space.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

Great Ideas

- Ruffer delivers positive return in difficult times but sees more pain for investors

- Ideal time to invest in life sciences cheaply through this trust

- Essentra's transformation to a pure-play industrial supplier is now complete

- How Crestchic is powering up for a growth push and why now is a great time to buy

Investment Trusts

News

- Will Porsche shares surge like Ferrari or skid like Aston Martin?

- Resilient Greggs holds firm on outlook in good start for Roisin Currie

- FTSE 100 firms set for record cash return in 2022 but pressures are mounting

- Find out which stocks surged and slumped during a turbulent third quarter

- Why dollar strength and foreign exchange volatility is bad for stock markets