Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineEuropean shares tend to do well when the US raises interest rates... not this time?

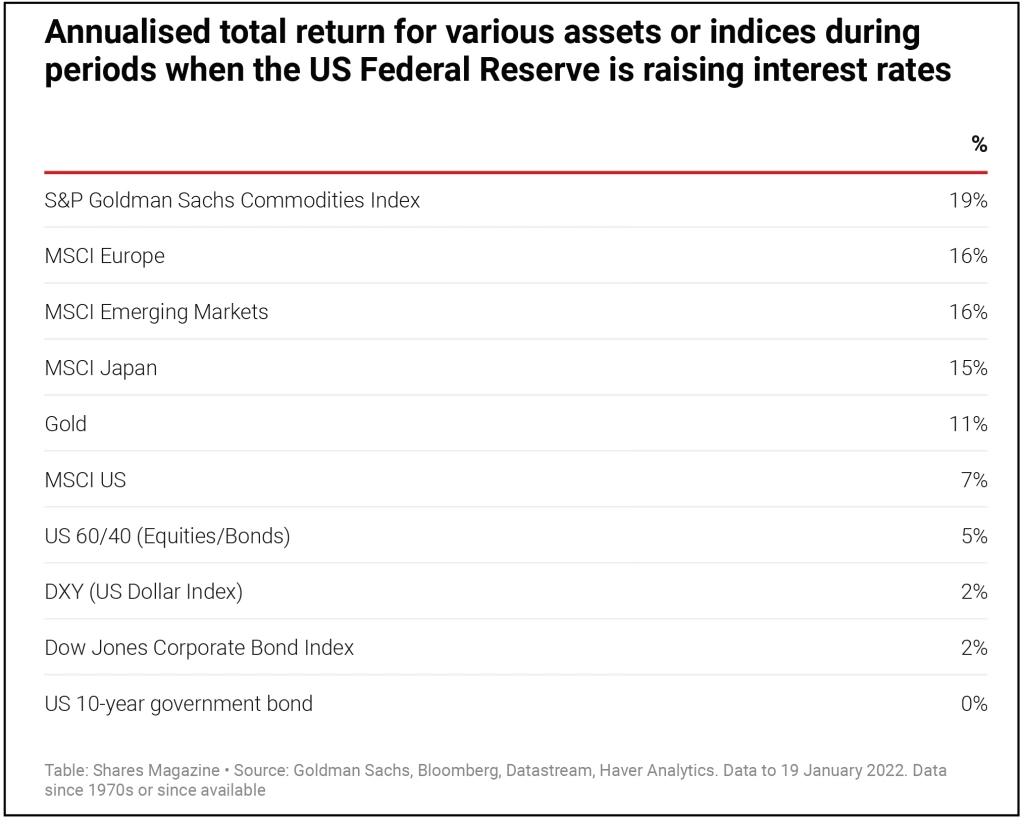

History suggests European stocks can do well when the US goes through a cycle of raising interest rates, such as we are seeing now. Analysis by Goldman Sachs finds the MSCI Europe share index achieved a 16% annualised return during such periods.

On this basis you might think Europe is a great place to invest. Unfortunately, the Ukraine war changes everything.

Europe is expected to see a sharp rise in inflation, partially linked to having to find alternative sources of energy supply and further supply chain disruption, and that could reduce earnings expectations for companies in the region.

STAY INVESTED OR LOOK ELSEWHERE?

Shares sees merit in staying invested in Europe as valuations are cheap and there are plenty of high-quality businesses with good longer term growth potential. The catch is that near-term performance could see a lot of ups and downs.

There are already signs that investors are no longer panicking about the war and that peace talks could lead to a resolution. If that does happen, we believe European stocks could rally hard as so much bad news has already been priced in.

Year to date Germany’s DAX index is down approximately 10% but that doesn’t tell the full story. At its worst point on 8 March, the index was down 19% since the start of January. Since then, it has rebounded by 13%. Investor confidence has been improving in recent weeks across Europe and other geographic regions.

REASONS TO BE CAUTIOUS

Not everyone shares our positive view, with some experts suggesting it might be time to take some money out of Europe and reinvest in other parts of the world including the US.

Strong consumption has been a key driver of the recovery in Europe, but consumers are now facing numerous headwinds as incomes are squeezed by higher inflation.

This has contributed to a recent decline in consumer confidence, which suggests a significantly weaker outlook for the European consumer.

The US should be among the most resilient economies globally, given its energy independence and its lower share of commodity consumption in gross domestic product.

There are still hopes 2022 can be a year of above-trend growth across the Atlantic as strong household and corporate balance sheets keep the economy on a firm footing.

LOOKING AT THE US AND JAPAN

In commentary published on 28 March asset manager BlackRock shifted its favourable stance on European shares in favour of US and Japanese stocks.

This change in geographic asset allocation is predicated on Russia’s invasion of Ukraine and the resulting spike in commodities prices.

Wei Li, chief investment strategist at Blackrock Investment Institute, says: ‘This is dampening economic growth and exacerbating supply driven inflation with Europe most exposed among developed markets.

‘We expect the energy shock to hit European equities hard. We like the market’s cyclical bend in the inflationary backdrop and expect the European Central Bank to only slowly neutralise policy’.

Morgan Stanley’s chief Europe economist Jens Eisenschmidt shares similar concerns regarding the increasingly constrained outlook for European consumers.

He says: ‘Compared with just a few months ago, the outlook for consumers in 2022 has darkened substantially. Consumers are now facing two distinct shocks this year, higher inflation, in particular higher food and energy prices, which is squeezing incomes. We expect inflation to average 5.3% in 2022, with energy inflation up by around 30% this year as of February 2022.

‘Food and utility bills account for approximately 15% of the total consumption basket in the euro area. A sharp increase in prices is likely to represent a tax on consumer’s disposable incomes and is likely to be reflected in lower consumption.’

Morgan Stanley estimates the rise in energy and food prices seen so far will result in a 0.5% hit to Eurozone growth in 2022.

DOWNGRADED GROWTH EXPECTATIONS

This more cautious view regarding the outlook is echoed by S&P Global Economics which now expects Eurozone growth to be 3.3% this year, compared to 4.4% in a previous forecast, and inflation to reach 5% this year and stay above 2% in 2023.

It comments: ‘Growth could face downward pressure, and inflation could be amplified by a higher and longer oil price shock, outright cuts to the gas supply, stronger confidence effects that would lead households to save more’

The European Commission’s March consumer confidence survey showed the second largest fall in the data’s history, with the largest fall recorded at the start of the pandemic. That is important to note because historically there has been a close link between consumer confidence and equity performance, both in Europe and the US.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Invest with confidence - four funds which make a perfect portfolio

- European shares tend to do well when the US raises interest rates... not this time?

- Why Trainline still faces a big test despite ticket commission win

- Our 2022 stock portfolio rises against a volatile market backdrop

- ESG investing faces a watershed after Russia’s invasion of Ukraine

Great Ideas

- Euromoney set to benefit from strong growth as data-driven businesses excite

- Zoo Digital sets up shop in Scandi-thriller homeland after Bollywood move

- Invest in Rathbones as a wealth management bid frenzy highlights value appeal

- Soaring book sales help publisher Bloomsbury beat sales and profit expectations

- Casual dining group The Fulham Shore offers great scope for growth

- Belvoir continues to enjoy strong tailwinds in the UK property market