Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSoaring book sales help publisher Bloomsbury beat sales and profit expectations

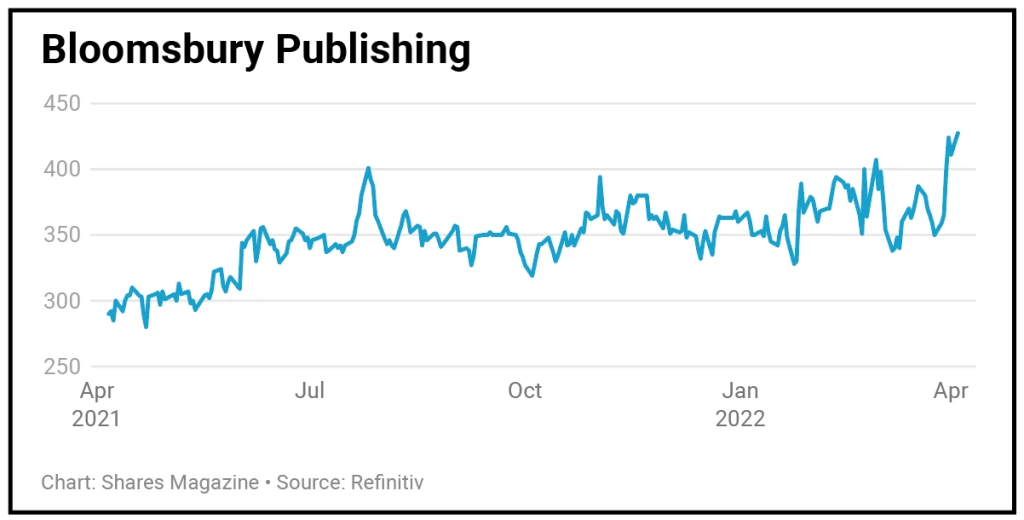

Bloomsbury Publishing (BMY) 403.2p

Gain to date: 42.5%

Original entry point: Buy at 283p, 4 February 2021

Our faith in Bloomsbury Publishing (BMY) continues to be rewarded with another encouraging trading update (30 Mar).

The company guided for revenue to be ‘comfortably ahead’ and profit ‘materially ahead’ of consensus expectations for the 12 months to 28 February.

A revival in reading seen during the pandemic looks to be continuing and Bloomsbury has demonstrated its ability to successfully mitigate ongoing supply and cost challenges.

Peel Hunt analyst Malcolm Morgan said: ‘Bloomsbury goes from strength to strength. It is a first-rate publisher, evidenced by the commercial and critical success it generates.

‘It is well financed – with significant cash assets on the balance sheet and investment in working capital, with the value of the library of publishing rights unrecognised on the balance sheet.

‘It is diverse in its subjects (children, adult, special interest, academic and professional), in the channels via which its product can be consumed (physical, e-books, online resources, rights), by the territory served (direct operations in the UK, US, India, Australia, and globally through export) and the nature of its routes to market (high street, online and direct).

SHARES SAYS: We continue to rate the shares as a ‘buy’.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Invest with confidence - four funds which make a perfect portfolio

- European shares tend to do well when the US raises interest rates... not this time?

- Why Trainline still faces a big test despite ticket commission win

- Our 2022 stock portfolio rises against a volatile market backdrop

- ESG investing faces a watershed after Russia’s invasion of Ukraine

Great Ideas

- Euromoney set to benefit from strong growth as data-driven businesses excite

- Zoo Digital sets up shop in Scandi-thriller homeland after Bollywood move

- Invest in Rathbones as a wealth management bid frenzy highlights value appeal

- Soaring book sales help publisher Bloomsbury beat sales and profit expectations

- Casual dining group The Fulham Shore offers great scope for growth

- Belvoir continues to enjoy strong tailwinds in the UK property market