Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

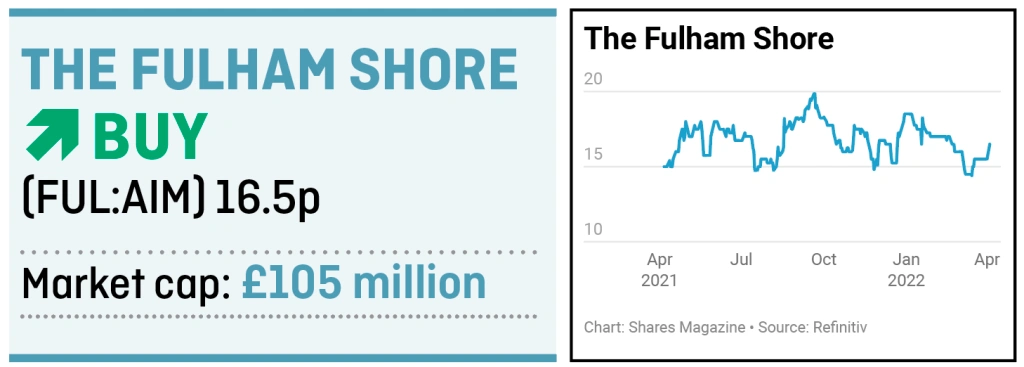

magazineCasual dining group The Fulham Shore offers great scope for growth

We have admired restaurant group The Fulham Shore (FUL:AIM) and its senior management team, which is one of the most experienced in the UK hospitality sector, for some time.

We almost recommended buying the shares in late 2019 but luckily given the impact of Covid forgetfulness – or inertia – meant we never actually pulled the trigger.

With the business having survived the pandemic and emerged in such good shape we think now is the time to snap up the shares.

A RARE SURVIVOR

Any hospitality firm which managed to weather such a perfect storm as the pandemic hasn’t just come out the other side a more resilient business but also one with better growth prospects due to the number of competitors which fell by the wayside.

The casual dining industry was already suffering from over-capacity in the run-up to Covid with many ‘samey’ restaurant chains like Ask, Bella Italia, Café Rouge and Prezzo struggling.

Even higher-end and household-name chain’s such as Carluccio’s and Jamie’s Italian ended up falling into administration.

Many of these firms expanded too quickly and paid up for ‘landmark’ sites which came back to bite them when trading tailed off.

It’s also notable how many failed restaurant chains were Italian-themed, while Franco Manca – Fulham Shore’s sourdough pizza brand – has gone from strength to strength.

Expansion has been measured, particularly during the pandemic, while rather than falling into the same trap that undoes many hospitality firms, namely trying to be all things to all people, Franco Manca does one thing and does it extremely well.

As its website says, whatever the question, the answer is pizza.

BUILDING THE BRANDS

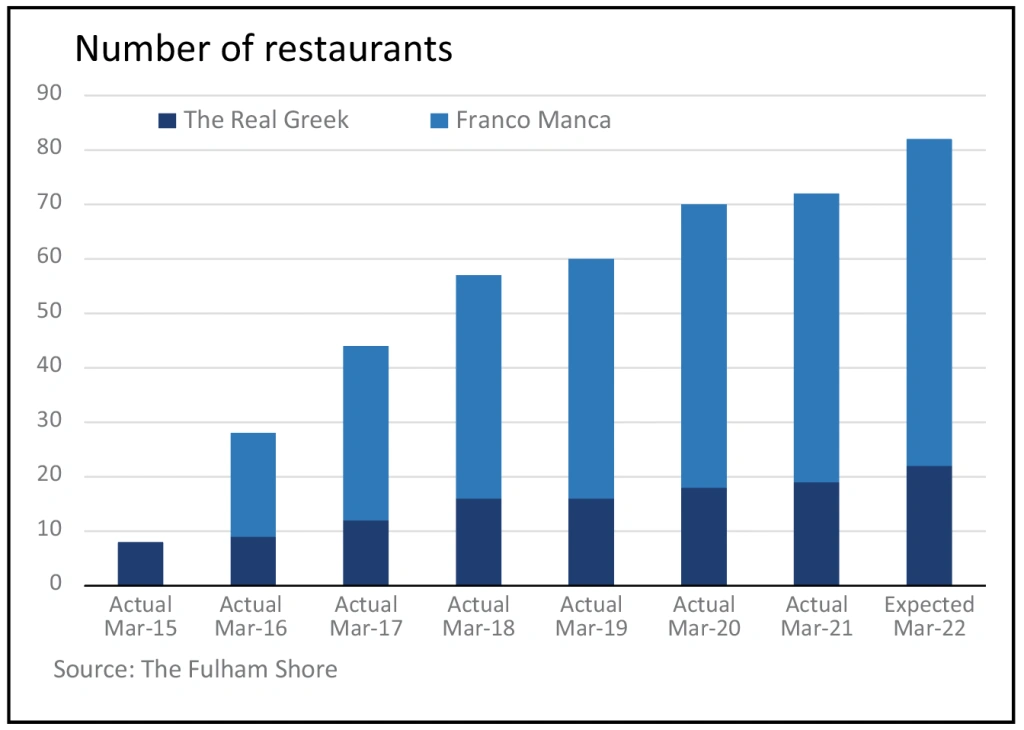

The group’s second brand is The Real Greek, which actually pre-dates Franco Manca by nearly 10 years but has half the outlets.

Franco Manca was acquired when it had just 11 restaurants compared with 59 today, while the Real Greek had just 6 outlets when it was acquired compared with 23 today.

Both brands have scalable business models based on good quality products, high restaurant volumes and an attractive price point, typically between £10 and £16 per head.

Both businesses buy their products directly from growers and suppliers in Italy and Greece which means they can control the quality of their ingredients and they can fix prices far in advance.

Buying direct also cuts out the wholesalers here and abroad who typically take their cut before selling on to restaurants, which means the firm can pass on lower prices to customers.

Group chairman David Page lives and breathes the restaurant trade, having started in the business managing a Pizza Express outlet in Kingston upon Thames more than four decades ago.

The name of the game is volume, not margins, says Page. ‘Chasing margins is very dangerous. What you really need is to get lots of turnover, which you do by offering a very good product for a very low price. Once you’ve got lots of people through the door, the margins take care of themselves.’

Between them Page and managing director Nabil Mankarious own more than 30% of the business, so their interests are very much aligned with shareholders.

INVESTING TO GROW

While its margins may not be as high as some firms, the restaurants themselves actually generate more profit than many of their peers.

Thanks to their profitability, and the availability of desirable sites at rents which are actually lower than before the pandemic, the group is using its high levels of cash flow to open 18 more outlets this year taking the total to 100.

As far as Page is concerned, the best way to create value is by investing in the brands.

‘The best thing for shareholders is to build up the value of each of the brands and then someone might come knocking for one or both of them.

‘That’s how you make the shareholders money, by growing the share price’, he adds.

Once the business is mature the firm might start paying dividends, but Page has said before he thinks between them the two brands could reach 250 outlets.

RISK FACTORS

We know challenges lie ahead for the hospitality sector, not least the cost of living crisis and its impact on peoples’ disposable income.

However, Fulham Shore’s value-for-money proposition should help insulate its brands from the worst of a contraction in discretionary spending and eating out.

Similarly, staff availability and costs are likely to be headwinds if infection levels rise or new variants emerge, but with the experience of the pandemic we think the group will be able to ride them out.

Assuming the country doesn’t go back into full lockdown, the group’s growth prospects look very good.

Sales and operating profit for the year to March 2022 are set to be ahead of market estimates of £73 million and £16.5 million, respectively.

By comparison, Restaurant Group (RTN) posted revenue

of £636 million and operating profit of £81 million last year.

Much of those sales and earnings come from the phenomenally popular Wagamama, which has over 150 restaurants as well as dark kitchens and another 50 overseas franchises.

For us, that demonstrates the scope for growth for Fulham Shore’s equally well-priced, scalable brands.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Invest with confidence - four funds which make a perfect portfolio

- European shares tend to do well when the US raises interest rates... not this time?

- Why Trainline still faces a big test despite ticket commission win

- Our 2022 stock portfolio rises against a volatile market backdrop

- ESG investing faces a watershed after Russia’s invasion of Ukraine

Great Ideas

- Euromoney set to benefit from strong growth as data-driven businesses excite

- Zoo Digital sets up shop in Scandi-thriller homeland after Bollywood move

- Invest in Rathbones as a wealth management bid frenzy highlights value appeal

- Soaring book sales help publisher Bloomsbury beat sales and profit expectations

- Casual dining group The Fulham Shore offers great scope for growth

- Belvoir continues to enjoy strong tailwinds in the UK property market