Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInvest in micro cap funds for growth

In light of the implications of the unfolding tragedy in Ukraine, the global growth outlook has dimmed, which means now more than ever, portfolios should be as diversified by asset class as possible to in order to maximise returns relative to risk.

Higher risk assets they may be, yet ‘micro caps’, the London stock market’s smallest quoted companies should form at least a portion of a well-diversified portfolio.

WHY INVEST IN MICRO CAPS?

Being early-stage businesses, the fortunes of many micro caps remain focused on the domestic economy and their ability to grow in a stagnant economic climate could prove useful in the current turbulent backdrop.

Micro cap companies offer potential for much more rapid-paced growth than mid or large caps, which means their share prices have a better chance of increasing at a faster rate over the long term. It is much easier for a £50 million market cap to get to a £200 million valuation than it is for a £50 billion company to quadruple in size.

Though there is no standard definition of what constitutes a micro cap, most market watchers consider the asset class to encompass companies valued at below £150 million and certainly sub-£250 million.

Through funds and investment trusts, investors can access the vast potential of opportunity in this under-researched part of the market, where managers are able to exploit liquidity premium and often find it easier to consistently generate market-busting returns.

As Gervais Williams and Martin Turner, managers of Miton UK MicroCap Trust (MINI), remarked in its January factsheet: ‘The nature of quoted micro-caps is that they are often overlooked by professional investors, so there is opportunity for active stock pickers to add to the potential upside.’

They also stressed that many UK micro caps ‘are relatively young businesses, that are serving industry sectors that are immature. During the pandemic-induced recession in 2020 for example, many businesses in the portfolio continued to prosper despite the global setback.’

One of the main drawbacks for investors in micro caps however is they can suffer from their shares being traded infrequently and in modest volumes. As a result, liquidity can be a major problem, with significant bid/offer spreads (the difference between the price at which you can buy and sell a share) triggering more pronounced share price moves.

10 YEAR STAR TURNS

Shares has crunched the data from FE Fundinfo to find the top 10-year total return performers among the merry band of dedicated UK micro cap funds and shine a spotlight on vehicles which may have shorter track records, yet might appeal to risk-tolerant investors.

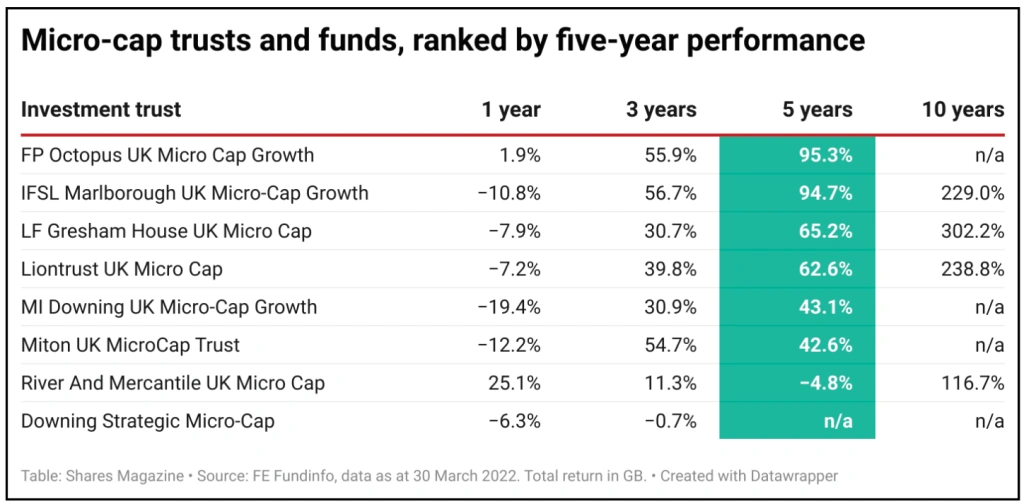

In the funds space, LF Gresham House UK Micro Cap (BV9FYS8) has returned 302.2% on a decade-long view and 65.2% over the past five years, consistently outperforming the IA UK Smaller Companies sector, though it has generated a negative return of 7.9% over a one-year horizon amid the market rotation away from risk assets due to fears over rising interest rates.

Managed by the well-regarded Ken Wotton, the fund looks for six key areas when assessing potential investments: entrepreneurial managers, strategy, market opportunity, market position, valuation and financials.

The latter includes earnings potential, quality of earnings and balance sheet strength. Its portfolio currently includes the likes of Alpha Financial Markets Consulting (AFM:AIM), cyber security firm Kape Technologies (KAPE:AIM), wealth manager Mattioli Woods (MTW:AIM) and maritime artificial intelligence leader and AIM newcomer Windward (WNWD:AIM), whose customers include BP (BP.), Shell (SHEL), HSBC (HSBA) and some leading government agencies.

Other 10-year performance star turns include IFSL Marlborough UK Micro-Cap Growth (B8F8YX5), which has returned 229% over 10 years and almost 57% over five, albeit the fund is down 10.8% over one year.

Ranked first quartile over three, five and 10 years, the Guy Feld and Eustace Santa Barbara-bossed unit trust has 35.9% of its assets in sub-£250 million companies, with customer relationship management software concern Cerillion (CER:AIM) among their number, although some 37.3% of assets are in companies that have grown from micro caps into small caps valued at between £250 million to £1 billion, among them recent Marlowe (MRL:AIM).

FP Octopus UK Micro Cap Growth (BYQ7HP6) may be down materially on a one-year view its performance over the longer term is strong.

Whereas the core is populated by profitable, cash generative businesses with an experienced management team, the satellite positions, limited to 25% of the portfolio by value, are higher risk growth opportunities including initial public offerings and exceptional growth opportunities including firms yet to turn a profit.

Launched in 2007, the £253 million Octopus fund has handsomely outperformed the IA UK Smaller Companies sector since inception. Managers Richard Power, Chris McVey and Dominic Weller pursue a long-term approach of investing in small fry that have the opportunity to develop into substantially bigger corporate fish, hopefully with global scale.

As at 31 January 2022, FP Octopus UK Micro Cap Growth’s diverse holdings spanned everything from AIM constituent RWS Holdings (RWS:AIM), the provider of language localisation and intellectual property (IP) support services, to Harry Potter publisher Bloomsbury (BMY) and construction materials distributor Brickability (BRCK:AIM).

RE-RATING POTENTIAL

All three dedicated micro cap investment trusts have differing approaches to the asset class and trade on varying discounts to NAV (net asset value) that imply the possibility of gains as the shares move bck towards the value of the underlying assets . The aforementioned Miton UK MicroCap, for example, trades at a 5.9% NAV discount.

Shares sees the wide 14.2% NAV discount on investment trust River & Mercantile UK Micro Cap (RMMC) as compelling, although prospective investors should note there’s a performance fee of 15% of outperformance levied on top of the 0.75% annual management charge.

Managed by the diligent George Ensor, the trust invests in sub-£100 million cap companies and as a closed-ended vehicle, can take a high-conviction, concentrated approach – only 41 stocks populated the portfolio at last count – which is not usually possible with open-ended structures.

Ensor is happy to run his winners as they move up the market cap ranks but it is also worth noting that River & Mercantile UK Micro Cap has continued to return to capital to shareholders at NAV in order to keep its net asset value at around the £100 million mark and continue to run a concentrated portfolio of tiddlers.

Chemistry graduate Ensor invests according to River & Mercantile’s tried-and-tested ‘PVT philosophy’, where stocks are evaluated by a combination of their potential to create value, their valuation and the timing of buying into a position.

Portfolio holdings range from Instem (INS:AIM), a provider of IT solutions to the life sciences market and sports nutrition business Science in Sport (SIS:AIM) to legal eagle Keystone Law (KEYS:AIM) and relative AIM newcomer CMO (CMO:AIM), the online-only building materials retailer.

Ensor recently supported the initial public offering of Strip Tinning (STG:AIM), a supplier of specialist connectors to the automotive sector with a leading market share in glazing connectors supply.

The company raked in £8 million of new money at 185p to build on its initial success in electric vehicle connectors where light, complex connectors are required to combine individual battery cells.

Downing Strategic Micro-Cap’s (DSM) 22.3% discount to NAV reflects some difficult early years since its 2017 launch, although recent performance has been encouraging.

In fact, Shore Capital believes ‘the market rotation favouring value stocks, given the prospect of further rate hikes, should provide a supportive environment for DSM’s portfolio’ as the market searches for value and the broker points out ‘most of the structural changes required in the portfolio companies have been implemented, and we believe it is now a matter of reaping the rewards’.

Managed by Judith MacKenzie, the fund employs a value approach and seeks to be influential through taking strategic stakes.

Investors should note the portfolio is highly concentrated at between 12 and 18 positions, among them the likes of Volex (VLX:AIM), Hargreaves Services (HSP:AIM) and Real Good Food (RGD:AIM).

Three new positions that value investor MacKenzie has added to the portfolio of late include Centaur Media (CAU), the publisher of The Lawyer and Marketing Week, as well as executive search specialist Norman Broadbent (NBB:AIM) and National World (NWOR), an ‘illiquid and under-the-radar company trading at the bottom end of the main market’ according to MacKenzie.

‘National World was a reverse into the regional publishing assets of the old Johnston Press. The management team are top calibre, with experience seldom found in £70 million market caps.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

- Invest with confidence - four funds which make a perfect portfolio

- European shares tend to do well when the US raises interest rates... not this time?

- Why Trainline still faces a big test despite ticket commission win

- Our 2022 stock portfolio rises against a volatile market backdrop

- ESG investing faces a watershed after Russia’s invasion of Ukraine

Great Ideas

- Euromoney set to benefit from strong growth as data-driven businesses excite

- Zoo Digital sets up shop in Scandi-thriller homeland after Bollywood move

- Invest in Rathbones as a wealth management bid frenzy highlights value appeal

- Soaring book sales help publisher Bloomsbury beat sales and profit expectations

- Casual dining group The Fulham Shore offers great scope for growth

- Belvoir continues to enjoy strong tailwinds in the UK property market