Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy 3M on the cheap before the market mood changes

Truly excellent companies are seldom available on the relative cheap but US industrial giant 3M is a rare exception. The share price has been on the backfoot since August and that has left the business trading on multi-year lows on a price to earnings basis.

It is dealing with some company-specific issues, but we believe these are largely transitory. On the assumption that 3M justifies our faith and demonstrates recovery, we believe there is substantial

scope for the stock to re-rate higher over the coming 12 months or so.

3M, whose history goes back to 1902, manufactures and markets more than 60,000 products that range from adhesives to abrasives, automotive aftermarket products, medical protective gear and tapes. Some of its well-known products and brands include Nexcare, N95 respirator masks, Post-it, Scotch, Scotch-Brite, Scotchgard, Thinsulate and many more day-to-day essentials.

The shares are listed in the US and 3M is part of the Dow Jones Industrial Average and S&P 500 indices.

MAIN ATTRACTIONS

The company’s sheer scale and diversity remain two of its chief attractions, developing and manufacturing all over the world.

Innovation is another draw for investors. 3M’s corporate strapline is ‘science applied to life’ and research and development activities are right at the heart of the business, allowing 3M to design many proprietary products.

‘It developed the N95 masks 20 years ago for industrial purposes but was able to scale that up during the pandemic,’ says James Dowey, co-manager of the Liontrust Global Dividend Fund (B9225P6) which features 3M in its portfolio.

3M’s business model that throws off a lot of free cash, more than $6.6 billion in 2020 despite the pandemic shutting down manufacturing for several weeks. Analysts estimate a similar $6.5 billion free cash flow for 2021, and that’s after slashing net debt by around $500 million to a forecast $1.45 billion.

Such a powerful cash generating machine has seen 3M increase its annual dividend for 64 years in a row, even upping the payout during the teeth of the pandemic. It yields 3.3%.

WHY HAVE THE SHARES BEEN WEAK?

There are two main reasons for the recent share price sell-off. The first is ongoing litigation. 3M is facing thousands of claims that earplugs sold to the military designed to prevent hearing loss didn’t work. Rulings so far have been mixed with 3M prevailing in some trials, not so in others, leading to multi-million-dollar awards. Ringfenced funds for potential future payouts should limited the long-run damage.

The other issue is cost inflation and 3M should be able to pass these onto customers. This is a global issue impacting businesses of all shapes and sizes as raw materials and staff wages rise. A large part of 3M’s cost base is chemicals while it is also exposed to the Chinese automotive industry facing a shortage of microchips.

Yet with vast scale comes tremendous pricing power, says Storm Uru, the other co-manager of Liontrust Global Dividend Fund. He says there is often a one or two quarter time lag in terms of passing on extra costs, which has dragged on market sentiment in terms of 3M’s shares. This should be worked through in early 2022.

LATEST EARNINGS

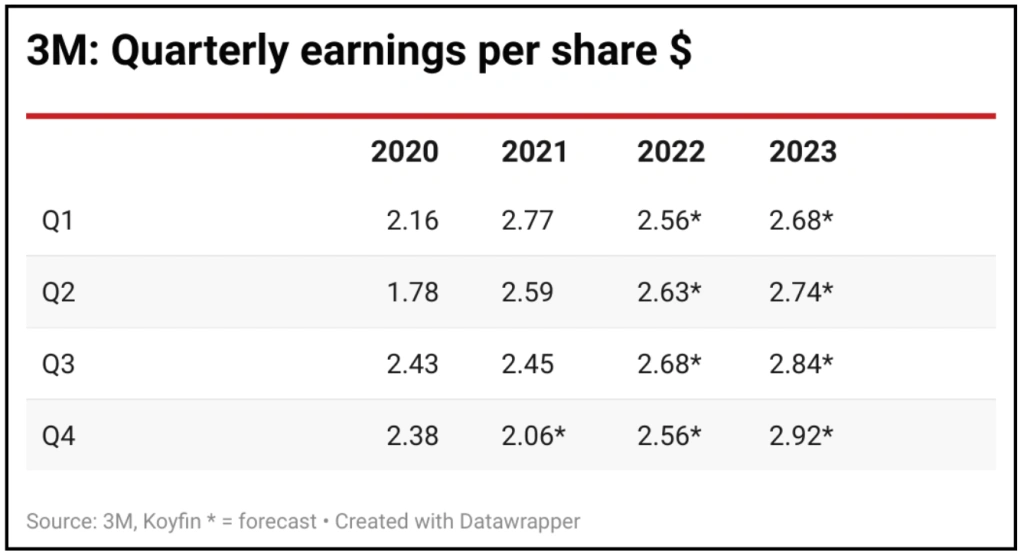

3M released third quarter earnings on 26 October 2021 showing revenue up 7.1% at $8.94 billion, and earnings per share of $2.45, both beating forecasts pitched at $8.65 billion and $2.21 respectively. Yet the share price still lost 2% on the day, an indicator of just how negative the market has felt towards the stock lately.

During the quarter, the group returned $1.4 billion to shareholders via dividends and share repurchases. Chief executive Mike Roman made a point of flagging broad-based organic growth, and strong margins and cash flow.

This leaves 3M on the cusp of what we believe will be a shift in the market mood towards the stock.

Bear in mind this is a company running on operating margins of 22%, with 45%-plus return on equity and return on investment in the mid-teens. The 2022 price to earnings multiple is 17, a PE that hasn’t been consistently this low in about seven years.

If we imagine that the PE returns to a level like 22 – this is perfectly realistic given it was in the 25-26 ballpark three years ago – it would imply a share price of more than $245 by the end of next year, simply based on existing 2023 earnings forecasts of $11.18 per share.

UK investors will have to complete a W-8 BEN form for tax reasons to buy the shares, but this is a fairly simple process.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

Investment Trusts

News

- BT could go down a different path for its sports arm

- China crackdown on US listings to benefit Hong Kong Stock Exchange

- Stock markets stage full recovery after Omicron fears

- Thungela plots bumper dividend despite coal price retreat

- Stocks relevant to efforts to licence vaping for medical use

- New listing rules aim to bring more innovative companies to London