Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStock markets in 2021: how have they performed?

Rotation has been a hallmark of 2021 with the early part of the year seeing growth shunned for value, before whipsawing back again as the year progressed. As the Omicron strain keeps Covid-19 very much in the headlines it looks like volatility will remain elevated in global stock markets as we approach 2022.

Pullbacks and shakeouts can be useful for investors, creating buying opportunities and helping the market to reset expectations. The past 12 months have seen three or four market shakeouts, the most recent on 26 November when the UK’s benchmark lost 3.6% in a day.

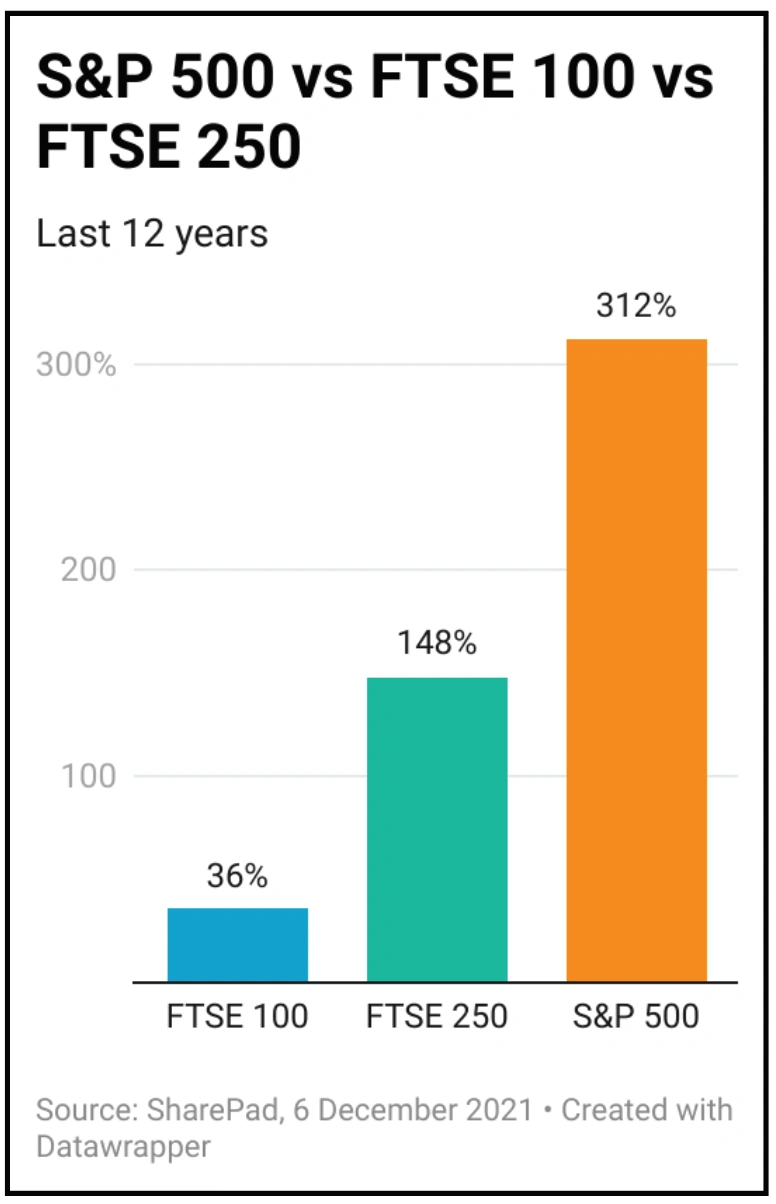

The conventional wisdom says that investing in the UK has been a bit of a disaster in recent years and if you look at the divergence between the FTSE 100 and the S&P 500 you can see why people might have come to that conclusion. This year’s 9.4% year to date performance of the FTSE 100 beats average long-range annualised returns of about 5% to 6% but that is less than half the near-23% of the S&P 500.

For context, the MSCI World index is up 14.7% in 2021 and Euro Stoxx 50 is 15.2% higher. Hong Kong’s Hang Seng, massively impacted by China’s technology regulations crackdown, has lost 15% this year.

FTSE 100 IS NOT THE UK

While the FTSE 100 is the UK stock market benchmark it is worth stating again that this is anything but a measure of the UK’s economic health. It shows the performance of the biggest companies, but these are concentrated in a handful of sectors and they earn most of their profits in the rest of the world, not here in the UK. According to data from Fidelity, just 24% of the FTSE 100’s sales are domestic, compared with 51% of the FTSE 250.

More than half of the value of the FTSE 100 is represented by commodities, financials and consumer staples. This was true in 2000, when an additional 30% of the index was in technology, media and telecoms stocks. TMT weightings have dwindled to next to nothing as companies have been taken over or gone out of business while the other stodgy sectors have grown more important. No wonder the FTSE 100 has gone virtually nowhere in two decades.

Yet the FTSE 250 tells a very different story. The mid-cap index’s 2021 performance has been broadly similar to its larger company cousin, up 10.6% year-to-date but has increased more than three-fold since 2000. Roughly matching the trebling in value of the S&P 500. Viewing UK stock market performance through this lens offers a far more compelling case for investing your money in UK companies, but only if you ignored many of those big, boring businesses in the FTSE 100.

HEATING UP BUT NOT OVERHEATED

On the face of it investors of a cautious nature might look at the S&P 500 and pause for thought. The index has risen 4.5-times in 12 years, quite the epitaph for the wreckage of the financial crisis.

‘If you look at the history of bull markets, the shape of the S&P chart will look familiar,’ says Fidelity. Stock markets climb a wall of worry, grinding higher as investors slowly put their fears to one side. Then at some point in the process, they throw caution to the wind, the glass becomes half full and the trajectory of the chart moves closer to the vertical.

‘Exactly the same thing happened towards the end of the 1982-2000 bull run.’

On that basis, the good times might continue for a while yet and you can make a good argument that valuations are not yet at the eye-watering levels of 2000, especially when measured against the much more expensive bond market today.

Investors need to look through the windscreen and not dwell too much on the rear-view mirror, and Goldman Sachs provides some encouraging data points.

While in valuation terms the FTSE 250 looks more expensive than the FTSE 100, with a price that’s 17.7-times expected earnings versus 12.4 for the blue-chip index. But look at the forecast earnings growth and that looks more than justified – Goldman Sachs estimates that FTSE 250 earnings will grow five-times faster than those in the FTSE 100 (53% vs 9%). And it’s worth pointing out that the FTSE 250 index’s valuation multiple is much lower than the 21.6 for the S&P 500.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

Investment Trusts

News

- BT could go down a different path for its sports arm

- China crackdown on US listings to benefit Hong Kong Stock Exchange

- Stock markets stage full recovery after Omicron fears

- Thungela plots bumper dividend despite coal price retreat

- Stocks relevant to efforts to licence vaping for medical use

- New listing rules aim to bring more innovative companies to London