Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

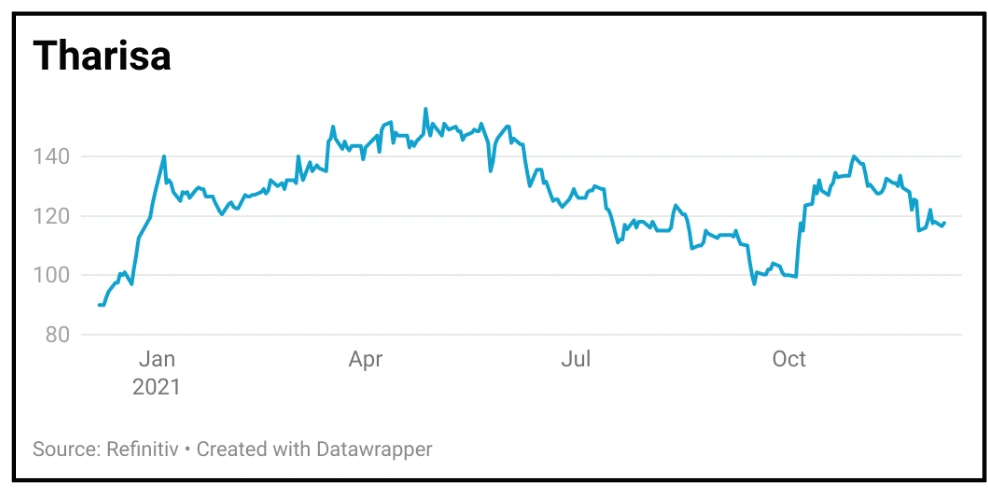

magazineTharisa can shake off recent weakness in 2022

Tharisa (THS) 117.6p

Loss to date: 10.9%

Original entry price: Buy at 132p, 28 October 2021

Platinum group metals and chrome miner Tharisa (THS) may have drifted lower amid recent price weakness for its products and Covid-related concerns in South Africa but we think the shares will regain momentum as evidence piles up of its improved cash flow in 2022.

On 2 December the company reported a record pre-tax profit of $185.3 million for the 12 months to 30 September, up 144.5% year-on-year on a 46.9% increase in revenue as margins improved. Free cash flow totalled more than $100 million and the dividend was up 157% to a record level.

The company also ended the year with a strong balance sheet, with net cash of $46.6 million. As the Vulcan processing plant is brought on stream operating costs are expected to come down and the company’s carbon footprint is also expected to reduce.

CEO Phoevos Pouroulis tells Shares the company is geared up to manage Covid risks despite the emergence of the Omicron variant in South Africa. This reflects the fact the open pit Tharisa mine is ‘socially distanced by the nature of the operations’, with clinics and track and tracing also set up on site.

SHARES SAYS: Stick with Tharisa.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

Investment Trusts

News

- BT could go down a different path for its sports arm

- China crackdown on US listings to benefit Hong Kong Stock Exchange

- Stock markets stage full recovery after Omicron fears

- Thungela plots bumper dividend despite coal price retreat

- Stocks relevant to efforts to licence vaping for medical use

- New listing rules aim to bring more innovative companies to London