Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

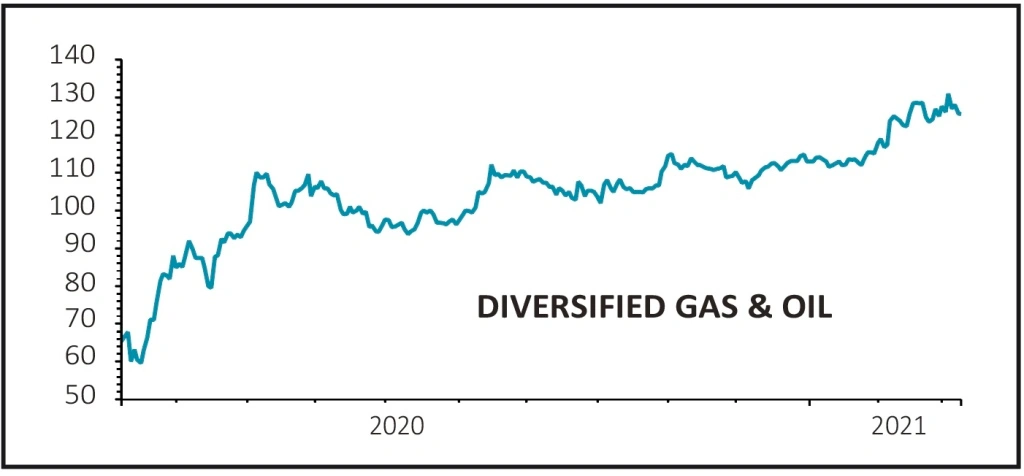

magazineThe share price and dividends are rising at Diversified Gas & Oil

Diversified Gas & Oil (DGOC) 127.4p

Gain to date: 24.9%

Original entry point: Buy at 102p, 21 May 2020

Unusually for a medium-sized oil company Diversified Gas & Oil’s (DGOC) investment case is as much about income as it is about capital gains but the recent improved sentiment towards the sector is helping it chalk up an advance in the share price to go with its growing dividend.

Results on 8 March saw the company report record annual production, up 18% to 100 million barrels of oil equivalent per day. This helped to underpin a 14% year-on-year increase in the dividend with two consecutive increases in the quarterly payment during 2020.

The company, which concentrates on acquiring low-cost natural gas production in the Appalachian region of the US, has protected itself from any downside in the gas price by hedging 90% of its output at an average price of $2.66 per million British thermal units.

In November 2020 the company formed a partnership with specialist asset manager Oaktree Capital to acquire further assets, with Oaktree committing up to $1 billion over a three-year period to be matched by Diversified.

Investec says the tie-up provides ‘the firepower for the company to go after deals in an “acquisition rich” environment in the US’, adding that it expects news on a deal in the coming months.

SHARES SAYS: Its strategy is simple and effective. Keep buying.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.