Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRare chance to buy popular tech trusts for a big discount

Investors have the rare opportunity to buy some technology-focused investment trusts significantly below the value of their underlying assets. Names on sale include Allianz Technology Trust (ATT), Polar Capital Technology Trust (PCT) and Scottish Mortgage Investment Trust (SMT).

The downside is that investors would be buying at a time when market sentiment has turned against this sector.

Making an investment now would require taking a long-term view over the prospects for tech-led businesses and being comfortable with potentially losing money in the near-term, should market sentiment stay negative towards these stocks.

WHY IS TECH OUT OF FAVOUR?

A surge in bond yields indicates investors are concerned about how economic recovery will drive inflation and lead to higher interest rates.

Investors are prepared to pay top dollar for high-growth tech stocks when rates are low but that changes in an environment where interest rates are rising.

WIDER DISCOUNTS

Historically Allianz Technology, Polar Capital Technology Trust and Scottish Mortgage have either traded at the same level of their underlying assets or at a small discount, such as 2% to 3%.

At the time of writing, Scottish Mortgage and the Polar Capital trust both traded approximately 12% below net asset value, while Allianz Technology Trust traded nearly 10% below NAV.

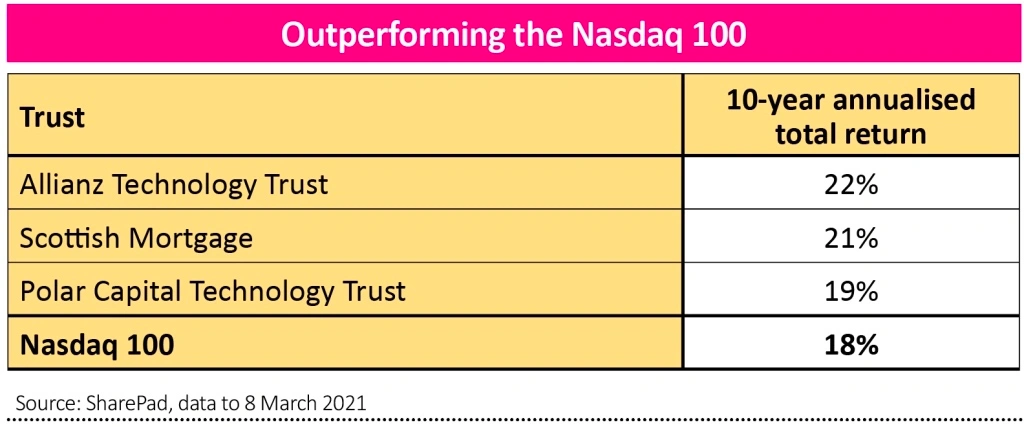

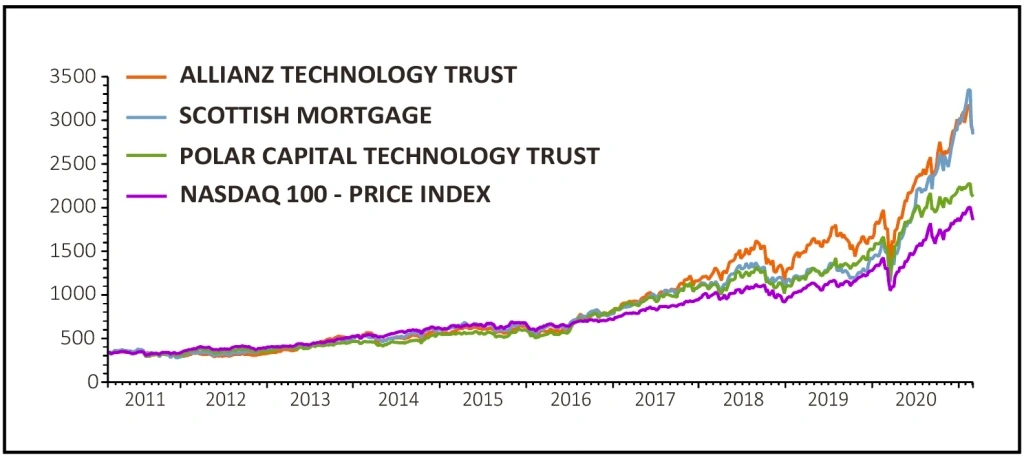

TRACK RECORD

It is fair to use the US tech-heavy Nasdaq 100 as a benchmark for these trusts and all three have outperformed an index which itself has delivered a total return of more than 400% over the last decade.

On one level their performance justifies the extra costs associated with an actively managed portfolio; after all you could achieve exposure to the Nasdaq with a lower cost exchange-traded fund.

To beat such a buoyant performance from the Nasdaq is a notable feat. Some credit for this achievement can be given to the investment trust structure which makes investment in early stage unquoted businesses easier and supports a long-term approach.

STRUCTURAL BENEFIT

Trusts, unlike mutual funds, aren’t as reliant on how easy underlying investments are to trade and aren’t forced to make short-term decisions on stocks as they don’t need to sell down holdings to meet redemptions when investors ask for their money back.

Beyond sharing the same structure and broadly the same focus on the tech industry there are important differences in the approach pursued by Allianz Technology, Polar Capital Technology and Scottish Mortgage.

For one, Scottish Mortgage, the largest of the three, would probably object to being lumped into the technology category, even if several of its top holdings – electric vehicle firms Tesla and NIO, Amazon, microchip specialist ASML as well as Chinese internet firms Alibaba and Tencent, would be considered tech businesses in most people’s eyes.

The aim, under long-standing managers James Anderson and Tom Slater, is to identify and invest in the best growth companies in the world and hold on to them for the long-term, so five years or more.

The recent decision of Anderson and Slater to trim exposure to Tesla, previously their largest holding, shows they are not averse to taking some profit when the opportunity arises.

Unquoted companies account for 16.1% of total assets and previous investments in private businesses which have gone on to join a stock market include music streaming firm Spotify, Alibaba and ride hailing app Lyft.

EXPLICIT TECHNOLOGY FOCUS

The Allianz and Polar trusts have a more explicit focus on technology but there are subtle distinctions in their strategies.

Run by veteran manager Walter Price and his team from San Francisco and with 85% of the fund allocated to North America, Allianz Technology takes a bottom-up stock picking approach which tends to mean it deviates from its benchmark more than some other tech funds with an active share (a measurement of just how much the portfolio deviates from the benchmark) of 70%-plus. The higher the percentage, the greater the difference to the benchmark.

There is an emphasis on meeting directly with businesses and staying in touch with the latest big themes to identify firms which could become the industry leaders of the future.

It has big positions in familiar names like Google-owner Alphabet, Amazon, Microsoft, Apple and Samsung. Alongside these there is a place for smaller outfits like online payroll firm Paycom Software and cyber security play Zscaler.

This approach might lead to a bit more volatility but historically has helped Allianz deliver outsized returns. Both the Polar Capital and Allianz trusts are all about capital gains as, unlike Scottish Mortgage, they do not pay a dividend. Nonetheless, Scottish Mortgage’s payout is nominal at best with a 0.3% yield.

COST COMPARISON

Steered by Nick Evans and Ben Rogoff, Polar’s tech trust also adopts a thematic approach with a focus on stock picking and likewise carries a mix of larger and smaller names. However, it hugs the benchmark a little bit more closely with an active share of 60.9%. Its performance, while still impressive, has lagged that of the Allianz product.

Polar Capital Technology is slightly more expensive with an ongoing charge of 0.93%, against 0.92% for Allianz Technology. The substantially bigger Scottish Mortgage benefits from greater scale and has an ongoing charge of 0.36%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.