Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineRecovery and income potential make Polar Financials stand out

There is a growing consensus that as the global economy recovers from the pandemic and long-term interest rates – such as the US 10-year Treasury yield and the UK 10-year gilt yield – start to move upward, investors need to increase their exposure to banking stocks.

The thinking goes that as banks are large, geared, cyclical plays they should benefit as the economy improves. They can lend more money to businesses and consumers at attractive rates while provisioning less against potential credit losses as the risk of default decreases.

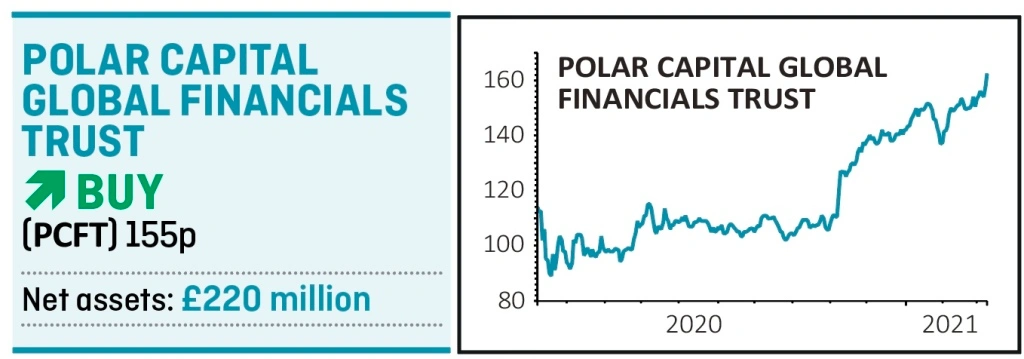

Our preferred way to get exposure to the financial sector as a whole, not just banks, is through Polar Capital Global Financials Trust (PCFT).

WELL CAPITALISED

The big difference between the current pandemic and the global financial crisis of 2007 to 2009 is the health of the global banking system.

After the financial crisis, regulators worldwide forced banks to provision early for potential bad loans and to carry enough surplus capital to be able to withstand another severe drop both in stock markets and economic demand.

As a result, the banking system today is far better placed to help speed the recovery than it was over a decade ago. If short-term interest rates rise along with long-term rates – which isn’t a given at the moment but seems likely if inflation overshoots the central banks’ targets – then banks would be a big winner as they would be able to expand their net interest margins for the first time in many years.

Net interest margin is a crucial figure to monitor with banks, being the difference between income received from loans and money paid out as interest to depositors.

As a rule of thumb, a 1% rise in US short-term interest rates would add 7% to bank earnings in the first year and 10% to 12% the following year. Earnings for European and Asian banks are even more sensitive to short-term rates so the uplift to profits would be significantly higher.

RISING INCOME STREAM

Shonil Chande, an equity analyst at investment trust research group QuotedData, highlights the fact the £220 million Polar fund aims to generate a growing dividend income alongside capital appreciation. As it stands, the dividend yield of 3%, paid semi-annually, is reasonably attractive compared with zero deposit rates.

However, because the banks were so well-capitalised going into the pandemic and the impact of defaults on loans has been so much milder than expected, the discussion has turned to distributions in the form of dividends and share buybacks.

For US banks, dividends and buybacks can’t exceed the previous four quarters’ net income. As the banks took large provisions in the first two quarters of last year, once those quarters drop out of the rolling 12-month calculation in July then tens of billions of dollars’ worth of unused loan reserves could be returned to shareholders.

For UK banks, the rules on dividends and buybacks are stricter but they can still look forward to a steadily growing stream of income over the next couple of years.

WELL DIVERSIFIED

Lead manager Nick Brind cautions against looking at the Polar investment trust through the lens of UK banks. ‘Understandably, there’s a lot of interest in the UK banking sector because it’s cheap and unloved, but there are huge opportunities globally,’ he says.

As well as banks, the investment trust has stakes in life insurers, non-life companies, asset managers, stock exchanges, specialty lenders, payment providers and fintech companies.

It is also geographically diversified, with exposure to Asia Pacific excluding Japan having risen from 18% to 26% over the past year making it the second largest region after the US, which accounts for 45% of the portfolio. By comparison, the UK makes up just 7% of the portfolio.

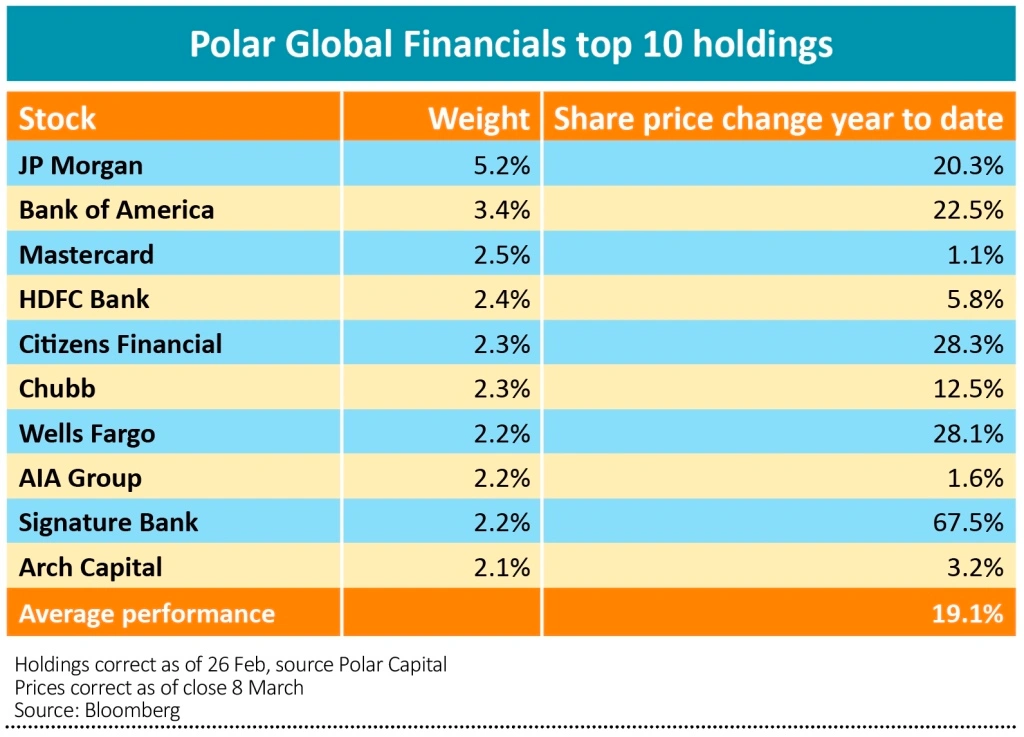

As of mid-February, the fund’s top 10 holdings were JPMorgan, Bank of America, Mastercard, HDFC Bank, Citizens Financial, Chubb, Wells Fargo, AIA Group, Signature Bank and Arch Capital.

Among the fund’s UK holdings are Direct Line (DLG), Helios Underwriting (HUW:AIM), Lancashire Holdings (LRE) and OneSavings Bank (OSB).

A TURNING TIDE

Many financial stocks hit multi-year lows during the first half of last year, but the sector outperformed strongly in the fourth quarter after the announcement of the Pfizer vaccine, helping the fund’s shares to a gain of 0.85% last year.

So far this year, the shares are up 9.1%, just slightly ahead of the net asset value which is up 9% to 153p.

We think financials in general and the fund have the potential to carry on rallying as confidence builds that the recovery is real and the tide of interest rates has turned.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.