Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat if the consensus reflation trade is wrong?

For all the bullishness heading into 2021, so far markets this year are barely changed outside of Asia. This is despite a record $272 billion of net inflows into US stocks in the last three months, including the second largest ever inflow into small caps.

Some investors might be disappointed with this outcome and wonder why so many stocks aren’t moving when there is still a broad consensus that markets will go up this year thanks to universal vaccination and a splurge in consumer spending as a wave of pent-up demand is released.

Shares sees plenty of reasons to be optimistic, yet it always pays to be a rational investor and consider what might cause markets to be wrong. This article is food for thought.

CONSENSUS VIEW: MARKETS WILL RISE

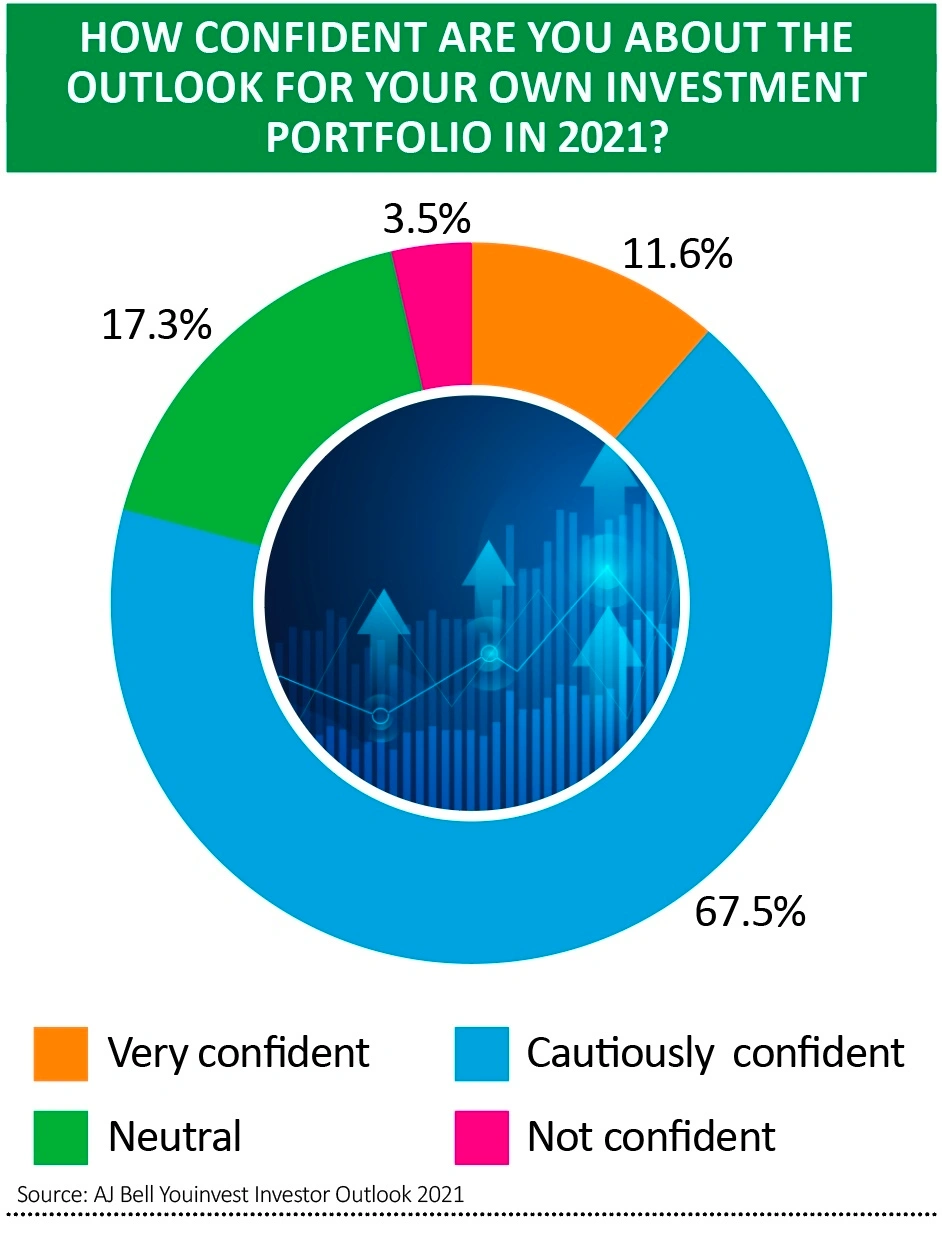

In an AJ Bell survey of 2,000 private investors in December, three quarters saw the FTSE 100 rising by at least 7% this year while a quarter believed the index could rise by more than 15% to above 7,500 points.

UK investors weren’t alone in looking ahead to sunny uplands. A survey of global asset allocators by Absolute Strategy Research showed record levels of optimism that global equity prices would increase this year, global earnings would be higher, stocks would beat bonds, value would beat growth, cyclicals would beat defensives, and emerging markets would beat developed ones.

In the AJ Bell poll, two thirds of retail investors cited the rollout of Covid vaccines and a return to ‘normal’ by Easter as a reason for their confidence in markets.

However, as it stands, delays in getting hold of the vaccine and treating enough people, together with the emergence of a more virulent strain of the virus, mean we could still be in lockdown in two to three months’ time.

Globally, vaccinations are running way behind projections according to data from Bank of America and Bloomberg.

The only region which seems to have moved past the point of coronavirus restricting its economic growth is Asia, but it can’t pull the rest of the world along single-handedly.

CONSENSUS VIEW: CONSUMERS WILL SPEND LIKE CRAZY

The notion that all consumers will indulge in a spending frenzy once lockdown ends also seems to be misplaced, at least in the UK. A survey by digital financial app Claro revealed that 20% of UK adults or 10.5 million people have insufficient savings to cover their household bills even for one month if they were to lose their job or their furlough payments.

More worryingly, the proportion of 18 to 24-year-olds without a month’s financial ‘cushion’ was over 30%, with more than 40% of young people saying their income already falls short of their outgoings.

Sadly, prospects for retail and hospitality – which employ large numbers of young people – are not looking bright. At the end of March, the sector faces the end of the lease forfeiture moratorium, meaning businesses could face rent arrears of up to £3 billion.

CONSENSUS VIEW: RATES WILL STAY LOW BECAUSE INFLATION ISN’T A PROBLEM

Probably the most consensus call of all is that central banks can keep interest rates low and keep credit flowing without stoking inflation.

However, a recent Harvard Business School study suggests the pandemic has altered consumer spending habits to such an extent that real inflation is double the rate registered by the official indices.

On the one hand, the basket of goods in most consumer price indices no longer reflects what people are buying, while on the other many elements of ‘essential’ spending such as housing, healthcare, education and childcare are grossly under-represented.

It’s also worth flagging that inflation works in two ways: you can either pay more for the same quantity of something, or you can pay the same for a smaller quantity, a more pernicious phenomenon known as ‘shrinkflation’ which doesn’t show up in the official indices. Chocolate bars are classic example of the latter, which is one reason why investors like Warren Buffett love confectionery makers.

UK inflation has been stoked both by the pandemic and Brexit, which has raised the price of imported goods while creating a scarcity of supply. In addition, companies are starting to see rises in input costs such as freight and raw materials. The fear in corporate circles is that at some point firms are likely to face calls for higher wages or risk industrial stoppages.

In the US meanwhile, the Federal Reserve’s shift to targeting ‘average’ inflation of 2% means it will let prices overshoot before it dares to lift interest rates.

A growing number of observers believe 2020 will be the inflection point for US rates, and as Bank of America points out, rates, regulation and redistribution (for example retail investors via the Reddit Wallstreetbets forum versus Wall Street hedge funds) are historically the catalysts which bring bull markets to an end.

In a worst-case scenario, we could end up with no growth but higher inflation and higher interest rates, which would be disastrous for investors in mainstream financial assets.

Disclaimer: AJ Bell is the owner and publisher of Shares magazine. The author Ian Conway and Shares’ editor Daniel Coatsworth own shares in AJ Bell.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Money Matters

News

- Amazon drops a bombshell during bumper US earnings season

- Pfizer sales boost puts vaccine economics under the spotlight

- Dr. Martens and Moonpig ‘pop’ on market debuts

- BP’s big challenge in funding its transition to renewable energy

- GameStop loses momentum but is the Reddit movement here to stay?

- What you need to know about changes to Bankers and Baillie Gifford European shares

- Marston’s fights takeover interest from US private equity firm