Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSilver spenders: Vaccinated and ready to reclaim their lives

It might not seem like it in the depths of a gloomy lockdown winter, but brighter days are ahead of us. By mid-February the UK hopes to have vaccinated most over-70s, with a large chunk of over-50s potentially covered by the end of March.

This cohort should then be much better protected against Covid-19 and that could result in a new spending spree.

Getting the vaccine should allow for the gradual reopening of society and give people more confidence to go out and reclaim their lives, using cash built up in lockdown to hit the shops, eat out, engage in leisure activities and travel.

Older people will be leading the charge because they will have been first to be vaccinated and so it makes sense to focus on where they might spend money.

FIVE STOCKS TO BUY

The rise of the silver spenders, or the so-called ‘grey pound’, could be a big boon to all sorts of different businesses. In this article, we highlight five stocks to buy which could benefit from increased spending by this demographic.

As well as leisure and retail, we also look at how parts of the financial services sector could benefit. We believe the over-50s will look back at the experience of Covid-19 and think harder about financial planning, which suggests greater demand for financial advice.

At the moment we can’t leave our local area, go to a restaurant, cinema, non-essential shop or other venue even if we wanted to, so some readers might wonder why we are saying to buy certain stocks now. We are taking a forward-looking view.

Judging exactly when restrictions will be lifted is difficult but a gradual easing by the summer doesn’t seem an outlandish scenario.

An important point to consider beyond any exit from lockdown is that by being vaccinated you are likely to feel happier about going out without the same risk of catching Covid, even if we still need to wear face masks for a while.

Many people are already planning their activities before even getting vaccinated, so we are confident there is pent-up demand which will soon translate into actual spending.

INCREASING SPENDING BY OLDER PEOPLE

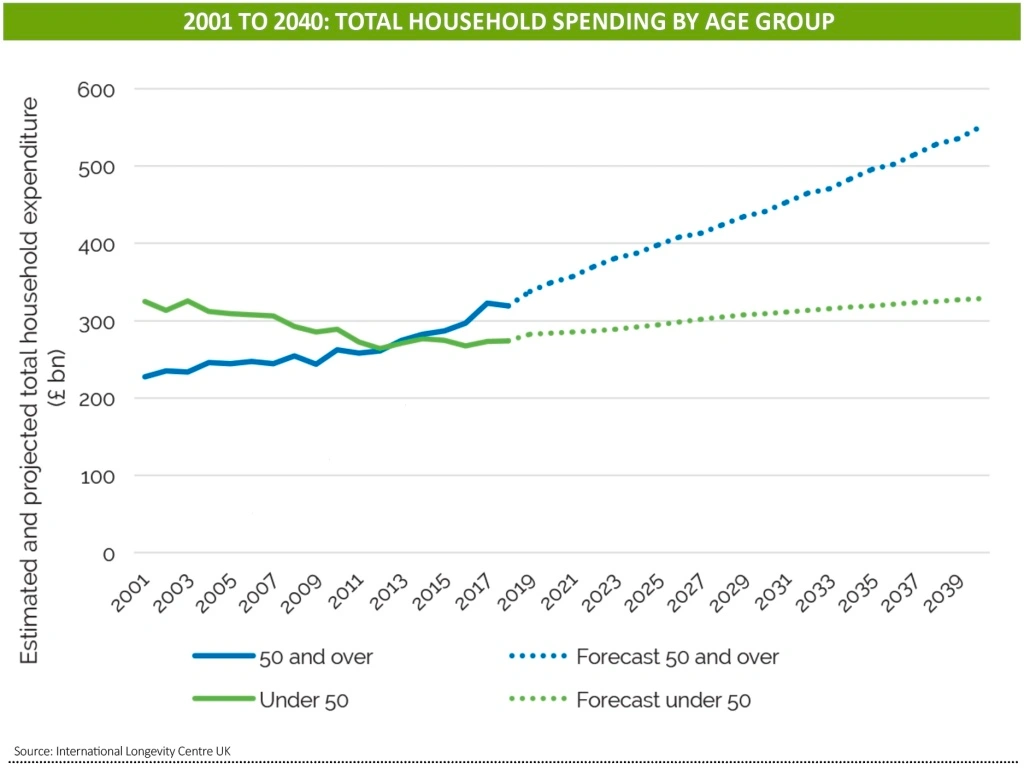

Increased spending by older consumers was already a growing theme before the pandemic. In a December 2019 report the International Longevity Centre UK forecast that by 2040, older households were expected to spend £550 billion a year (63% of total spending).

It said: ‘This is £231 billion more than in 2018 and £221 billion more than projected spending by younger households in 2040. This means that by 2040, 63p of every pound spent in our economy would be spent by older households.’

The report also noted that the top three growing sectors for older consumers were recreation and culture, transport and household goods, and services.

Among the most obvious beneficiaries of the silver spenders is Saga (SAGA). The insurance and travel provider targets the over-50s and the growth of this demographic is seen as a long-term catalyst for the group.

Even before the pandemic disrupted its cruise business, Saga proved to be a massive disappointed to the market. This was evident in the big losses it chalked up in its January 2019 and January 2020 financial years. Adjusting for an October 2020 share split, the stock is down 90% on its IPO price. Its fortunes are now improving.

A new CEO, Euan Sutherland, took over at the start of last year and a £150 million fundraise supported by former chief executive and founder’s son Roger de Haan, who moved into the chairman’s seat, has helped to steady the ship.

After its latest trading statement on 26 January Numis analyst Nick Johnson said: ‘We think this is a reassuring update, with insurance on track to meet forecasts, an ample cash position, and encouraging signs of pent-up demand in the cruise business.’

Based on Numis’ January 2023 post-pandemic forecast, the shares trade on a price to earnings ratio of 4.3 times. This looks like an attractive buying opportunity.

RETAIL WINNERS

A vaccinated over-50s cohort should have greater confidence in venturing outdoors in the months ahead, a welcome development with positive implications for select retailers. Cooped-up for months on end, consumers of a certain vintage will want to hit the high streets, shopping centres, retail parks and restaurants, and reacquaint themselves with socialising while also investing some of the cash they’ve saved up during lockdowns.

This behavioural shift offers a potential earnings catalyst for homeware and furniture retailers such as cushions, quilts and kitchenware seller Dunelm (DNLM) and sofa sellers DFS Furniture (DFS) and ScS (SCS). The latter pair’s products are tactile in nature, so a reopening of non-essential stores should see pent-up demand released as over-50s wander into their shops and touch their products before they buy.

Vaccinations could also sustain the boom in spending on major DIY or home and garden improvement projects, generating a possible earnings tailwind for the likes of B&Q-owner Kingfisher (KGF), specialist retailer Topps Tiles (TPT) and PVCu replacement windows and doors maker Safestyle UK (SFE:AIM). The older demographic’s rising levels of confidence in getting outdoors could boost other purveyors of big ticket purchases such as cars, offering a potential boost to earnings for major auto retailers Pendragon (PDG), Vertu Motors (VTU:AIM), Cambria Automobiles (CAMB:AIM) and Marshall Motor (MMH:AIM).

As social life and events begin to return, retailers catering for the more mature customer may well see an uptick in sales, among them high street stalwart Marks & Spencer (MKS) and plus-size digital fashion retailer N Brown (BWNG:AIM), the Manchester-based business which sells to the underserved 50-plus demographic via its JD Williams and Ambrose Wilson brands.

Manufacturers that might see improved trading prospects from the grey pound include the likes of luxury interior design and furnishings specialist Sanderson Design (SDG:AIM) and Portmeirion (PMP:AIM), the company behind homewares brands such as Royal Worcester, Spode and Wax Lyrical, not to mention Churchill China (CHH:AIM), the pub and restaurant ceramics maker counting on a recovery in the casual dining market.

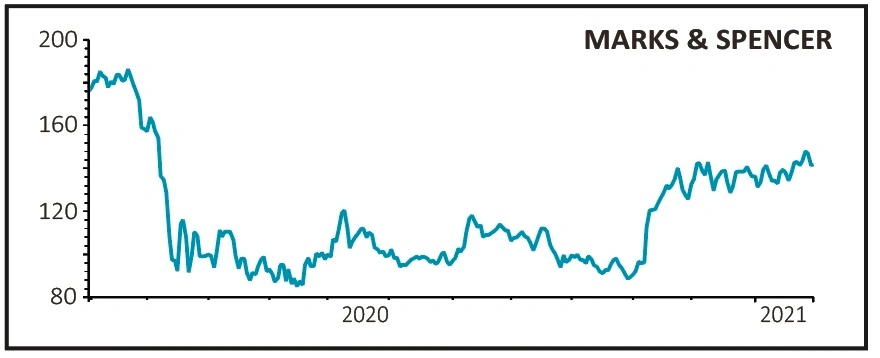

Buy Marks & Spencer at 144.65p

Covid-induced lockdowns and restrictions have taken a massive toll on British retail institution Marks & Spencer, as demonstrated by its Christmas trading statement. UK turnover for the three months to 26 December fell 7.6% on a like-for-like basis to £2.53 billion, as a 2.6% rise in food sales was more than offset by a 24.1% decline in clothing and home sales.

Virus restrictions are likely to remain in place until at least the spring, leaving Shore Capital to forecast a collapse in pre-tax profit from £403 million to a mere £24 million for the year to March 2021.

However, the market is forward looking and as the older cohort is vaccinated, restrictions are lifted and non-essential stores reopen, over-50s may begin to congregate at M&S once again, reviving a clothing and home business lapping soft comparatives and boosting Marks & Spencer’s food business.

AT THEIR LEISURE

If the government’s vaccination plans are delivered by mid-February, the elderly and most vulnerable in society will be able to emerge from their long hibernation behind closed doors.

This may unleash an increase in activities ranging from day trips to the countryside or beach, Bingo nights with friends and more treats such as a nice meal in a country pub or a long weekend at a spa.

At the very least people will want to engage more within their local community and should feel safe visiting friends in local cafes and bars.

This could drive earnings for community all-day café/bar/restaurant company Loungers (LGRS:AIM) whose 168 sites are located in small towns across the country, trading under the Lounge and Cosy Club brands.

As traditional pubs have closed Loungers has increasingly become the social hub for many towns where locals can meet and discuss affairs that affect the community.

The company delivered significant outperformance of the market once sites reopened last July, delivering 25.1% like-for-like sales growth over the 13 weeks to 4 October.

This was no doubt also helped by the fact that the company has no sites in large city locations.

Despite the challenges caused by the pandemic Loungers has continued its growth strategy, albeit on a reduced scale and has a long-term goal of growing to 400 sites.

A chance to escape the local town might also be an attractive endeavour to those people who have been confined to their home for months.

Activities such as taking a leisurely drive to a country pub or staying overnight in a hotel/pub could become more popular. Pubs and hotels group Marston’s (MARS) has 400 destination pubs and inns spread across the UK from Newcastle to West Sussex.

Our favoured option for investors looking to get exposure to the theme is Young’s (YNGA:AIM) with its collection of inns and country escapes offering weekend retreats.

The freedom to leave the house with confidence boosted by inoculation extends into the evenings too and a big rebound in bingo could be on the cards.

While there aren’t any pure bingo companies listed, Rank Group (RNK) owns the Mecca bingo brand. When its venues could open last summer, it saw a 25% uplift in the number of customers visiting its bingo halls.

Ladbrokes and Coral owner Entain (ENT), formerly GVC, owns the Gala bingo brand.

TIME TO TRAVEL

People aged 50 and over are shifting their spending towards non-essential purchases according to a report by the International Longevity Centre.

The report says transport spending among over 50s is expected to see growth of £62 billion from 2019 to 2040 and is one of just a small number of sectors expected to see any growth at all among over 50s.

Signs of this can already be seen since the vaccine rollout started as confidence from this demographic to book holidays grows significantly.

Cruise operators Saga, TUI (TUI) and Carnival (CCL) have all reported a surge in bookings from over 50s as the demographic offers a ray of hope to beleaguered holiday and travel firms.

Saga for example has said that despite the pandemic, customer retention levels have been high and an average of 69% of cruise passengers rebooked rather than requested a refund.

More recently it said this has jumped to 86%, showing the ‘pent-up demand for cruises among our guests who will benefit from the first round of vaccine rollout’. TUI, the UK’s largest tour operator, said in mid-January 50% of bookings on its website were made by over-50s, while Carnival said bookings for the first half of 2022 are above 2019 levels.

But in less positive news for the big cruise and holidays firms, it could be domestic travel that benefits the most with recent headlines talking about a staycation boom once again this summer.

Extended lockdowns and international travel bans have seemingly hit consumer confidence to an extent in terms of holidays abroad, with a number of domestic operators reporting a sharp rise in enquiries and bookings.

There have been conflicting reports whether Spain for example, by far the most popular destination for UK holidaymakers according to ABTA, will open to tourists before the end of summer, while politicians continue to warn against booking foreign holidays.

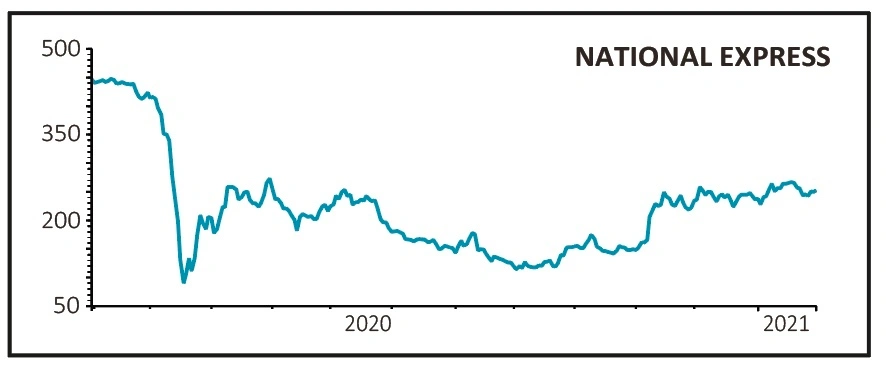

Buy National Express at 247.4p

Coach operator National Express (NEX) recently reported a 185% increase in spring and summer holiday bookings compared to the same period last year. Around 98% of its holiday customers are over 65s.

Analysts at Berenberg are keen on the stock and say it’s a ‘matter of when, not if earnings recover’, adding it has shown resilience in the pandemic and has many growth opportunities ahead in North America and Morocco, with any boost as a result of the vaccine rollout considered a bonus.

SAVINGS AND RETIREMENT PLANNING

When we discuss demographics and the power of the ‘grey pound’, we shouldn’t overlook the importance of the savings and retirement market.

According to the Office for National Statistics (ONS), the market value of UK pension funds reached £2.2 trillion at the end of 2019, boosted by the take-up of auto-enrolment.

By comparison, the total amount of deposits held by UK households, excluding notes and coins, was just £1.5 trillion at the end of last year according to the Bank of England.

The current generation of retirees typically has a well-funded final salary pension scheme and a range of retirement products such as individual savings accounts (ISAs) and self-invested pensions (SIPPs), which means they don’t need a high level of advice beyond estate planning.

However, the generations below them are much less likely to be able to retire at 65 as they don’t have the same generous pensions or level of savings as their predecessors, and typically they are happy to pay for professional financial planning advice.

Firms such AFH Financial (AFHP:AIM) have been extremely successful in selling advice as well as gathering assets, even seeing inflows during the pandemic despite – or perhaps because of – heightened uncertainty over the economy.

Earlier this month chief executive Alan Hudson said he expected more consolidation in the sector, with AFH one of a small number of larger businesses eventually dominating the landscape.

Within a week of his comments, the firm received a takeover offer at a 16% premium to its market value from a US private equity investor aiming to scale the business up rapidly through mergers and acquisitions.

Buy Just Group at 73p

Just Group (JUST) is one of the leading players in the retirement savings and advice market, having amassed retirement income sales of £2.15 billion in the year to December.

Driving this growth was a 22% increase in defined benefit premiums, courtesy of a very buoyant market. Also, thanks to strong pricing discipline, the firm’s operational gearing has increased meaning profits will have grown faster than turnover.

Analysts at Numis recently raised their full year 2020 and 2021 revenue and earnings forecasts and put a price target of 160p per share on the company, more than double the current level, which reinforces our positive view.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Money Matters

News

- Amazon drops a bombshell during bumper US earnings season

- Pfizer sales boost puts vaccine economics under the spotlight

- Dr. Martens and Moonpig ‘pop’ on market debuts

- BP’s big challenge in funding its transition to renewable energy

- GameStop loses momentum but is the Reddit movement here to stay?

- What you need to know about changes to Bankers and Baillie Gifford European shares

- Marston’s fights takeover interest from US private equity firm