Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineTurnaround scope means you should have ‘Intel inside’ your portfolio

Microchips giant Intel had a rough 2020. While most major technology stocks soared last year, this one-time bellwether has struggled as rivals like Nvidia and Advanced Micro Devices (AMD) ate its lunch.

Even after a double-digit recovery rally in 2021 the stock has bounced less than 30% off 2020 lows, dismal when compared to the S&P 500’s 70% rally. Nasdaq, where Intel is listed, has almost doubled in price.

The days when every computer gadget seemed to be powered by ‘Intel inside’ seems a long time ago, yet there is hope that the Santa Clara-based business is ripe for a reversal of fortune.

We believe new Intel leadership is capable of sorting out its manufacturing struggles, retaking control of its future, and rebuilding its reputation within the industry and with investors. If so, we would expect the stock to power beyond all-time highs of over $70, while still paying handsome dividends.

TRIPPED ITSELF UP

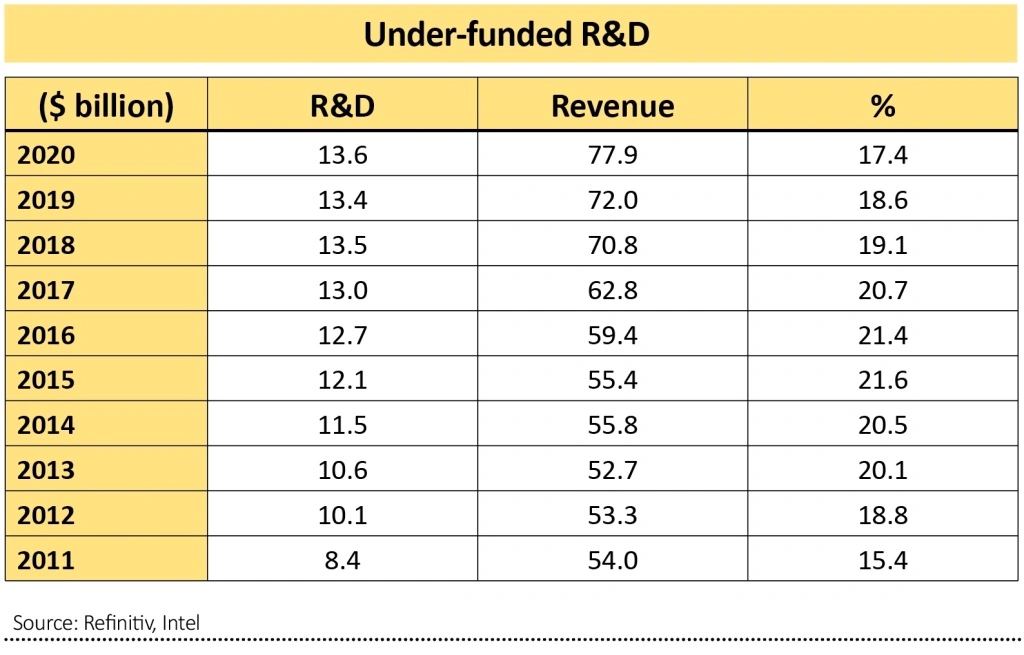

Intel’s problems have been largely of its own making. Under chief executive Bob Swan the company has focused on reducing capital expenditure and boosting share buybacks to drive shareholder returns, financial engineering that has left its semiconductor engineering R&D (research and development) under-resourced. R&D as a percentage of revenue fell to its lowest in 10 years in 2020 at 17.3%, versus the 10-year average of 19.6%.

That myopia has seen Intel lose its grip on the microchip bleeding edge and fall behind rivals. Struggles to ramp up production of newer 10nm (nanometre) chips have had knock-on effects. In July, Intel stunned investors by admitting its next generation 7nm chip development was running at least 12 months behind target and won’t be ready until 2022 or even 2023.

TSMC is already manufacturing 7nm chips for AMD and other chipmakers, and it will likely be producing 3nm chips by 2022, according to analysts. Apple has also announced that it plans to design its own semiconductors (based on ARM architecture) for its Mac range and outsource manufacturing, ending years of partnership with Intel.

Investors are now pushing for Intel to outsource manufacturing like many of its design rivals do. This would slash the expensive business of factory (known as fabs) retooling and free the company to concentrate on design, with its faster growth and higher margin profits.

Managing this task will fall to incoming CEO, and former Intel chief technology man, Patrick Gelsinger. He will take over on 15 February but he is already making his mark, luring back engineering talent from Intel’s past.

Gelsinger seems reluctant to stop manufacturing entirely, so it looks like a balance will be struck in time, but the greater focus on R&D and design is a huge step forward. That should ensure that Intel reclaims its position at the top end of the supply chain for PCs, laptops and, increasingly important, data centre server computers and internet of things connectivity applications, while pushing ahead in graphics processors and automotive development.

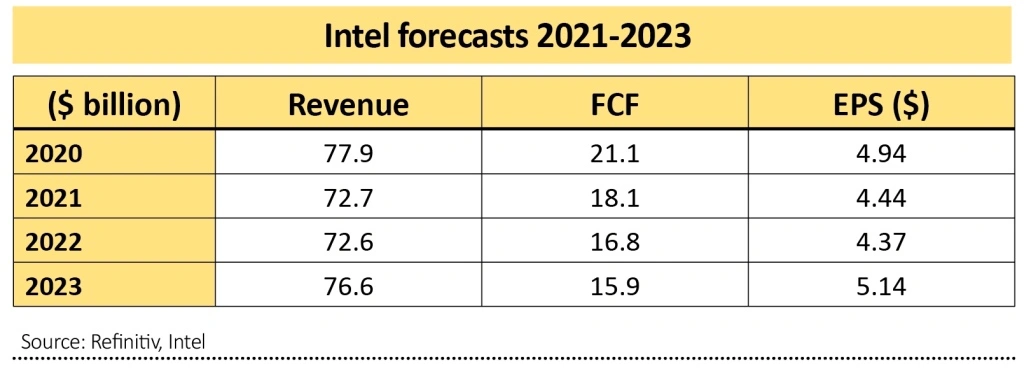

Intel has just reported a 15% fourth quarter revenue beat on estimates at $20 billion and earnings per share (EPS) of $1.52, versus $1.10 expectations. Despite better-than-expected Q4 and encouraging guidance for Q1 2021, sluggish data centre demand across cloud providers, enterprise and government end-markets is likely to weigh on the top-line performance in the near term, believe analysts.

That’s demonstrated in 2021 and 2022 EPS and revenue forecasts that can be described as pedestrian at best, before the expected pick up in 2023.

CHANGING THE TUNE

We believe that the previously downbeat mood music is gradually changing, a process that Gelsinger’s appointment this month will accelerate. ‘With a new CEO coming on board, it does seem the company is stabilising,’ says Daiwa Capital Markets. ‘Intel does have many competitive advantages, like 15,000 internal and a million external software developers and a full line of products.’

Other wide moats include its brand power, wealth of expertise, years of industry trust and very strong cash flows. Last year Intel threw off a staggering $21.1 billion of free cash flow, its biggest haul in at least five years and easily covering the rough $5.5 billion of 2020 dividends. Net debt of $28.2 billion compares to more than $81 billion of shareholders’ equity giving a sleep-easy debt-to-equity ratio of 35%.

Metrics such as return on equity and return on capital employed, which help measure the quality of a company’s profitability and bang for buck from investment, averaged 26.5% and 20.2% over the past five years respectively. Intel is also one of the US’s top 20 responsible companies, according to ESG (environmental, social and governance).

The stock has a delivered total return (share price plus dividends) of 14.6% and 11.9% annualised over five and 10 year periods respectively, according to Morningstar data, albeit below the average of the Nasdaq.

At $56.06, the stock trades on a 2021 price to earnings (PE) multiple of just 12.8 and promises a $1.37 dividend, implying a decent 2.4% yield for a company with scope to re-energise growth.

That modest valuation and respectable yield should limit Intel’s downside even if things don’t play out quite as planned.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Money Matters

News

- Amazon drops a bombshell during bumper US earnings season

- Pfizer sales boost puts vaccine economics under the spotlight

- Dr. Martens and Moonpig ‘pop’ on market debuts

- BP’s big challenge in funding its transition to renewable energy

- GameStop loses momentum but is the Reddit movement here to stay?

- What you need to know about changes to Bankers and Baillie Gifford European shares

- Marston’s fights takeover interest from US private equity firm