Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThe lost decade for Cash ISA savers

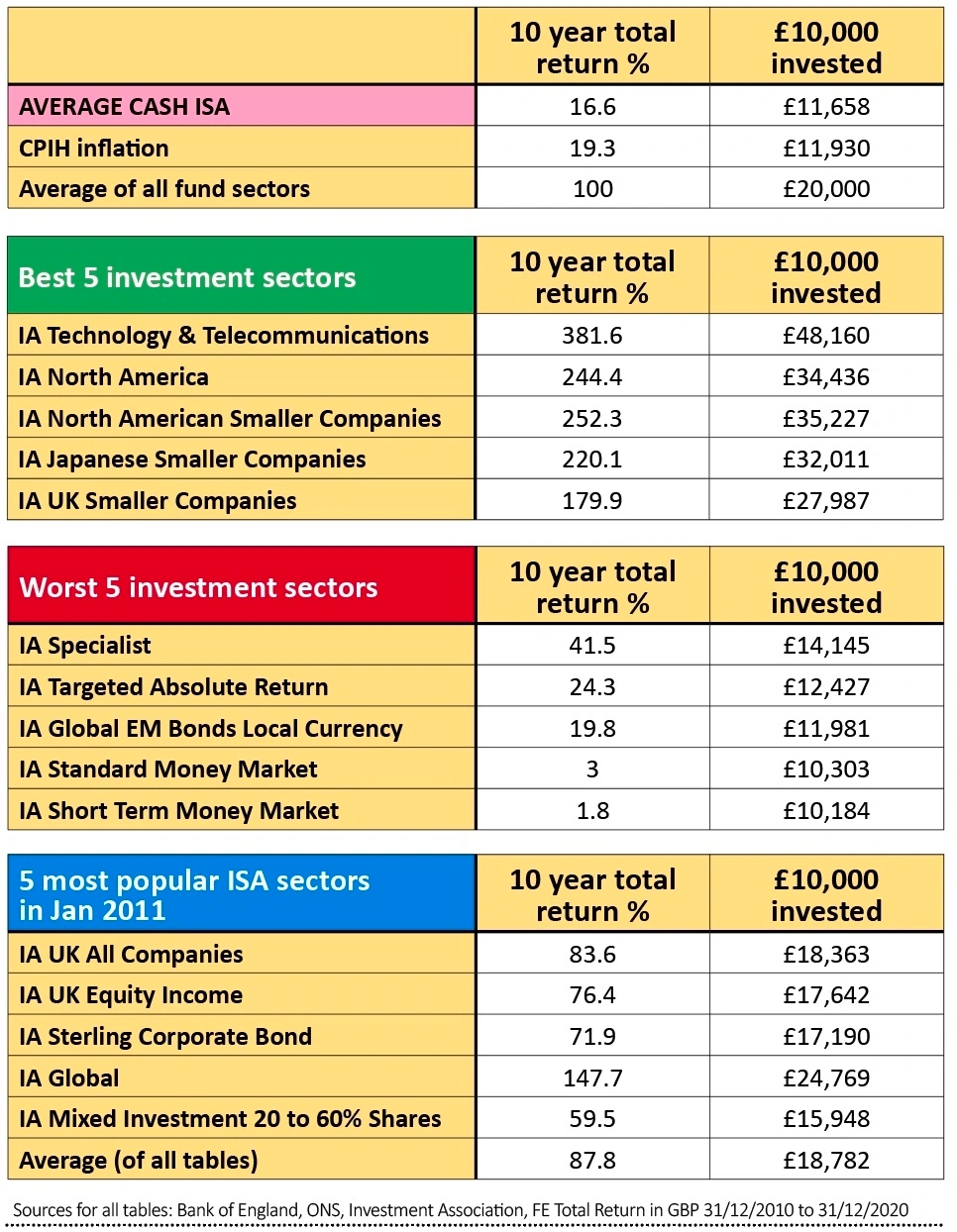

It has been a lost decade for Cash ISA savers, with the interest from the average account failing to beat inflation over the last 10 years. That means the money stashed away has actually lost its buying power.

A saver who prudently used their full Cash ISA allowance every year since 2011 would have sunk £127,320 into these accounts. That money would now be worth £124,857 after inflation is taken into account, based on the interest paid on the average Cash ISA account published by the Bank of England. That’s a loss in real terms of almost £2,500.

Things have been very different for Stocks & Shares ISA investors. The same £127,320 invested over the last decade into the average global equity fund would be worth £196,079 after inflation, a gain of almost £70,000 in real terms.

There has been a high degree of variation in performance across markets, with technology funds and US funds sitting atop the fund league table. But the average fund sector has delivered a 100% return over the last 10 years, equivalent to doubling your initial investment (in nominal terms, so not adjusting for inflation).

Likewise the five most popular sectors with stocks and shares ISA investors in 2011 have significantly outperformed the average Cash ISA, posting an average 10 year return of 87.8%, compared to 16.6% from cash.

EXTREME DIVERGENCE

The extreme divergence between the fortunes of cash savers and stock market investors over the last 10 years comes down in part to the actions of central banks. Loose monetary policy has depressed the interest paid on cash, while at the same time boosting the prices of the shares and bonds which form the bedrock of most ISA portfolios.

Of course, it’s all very well looking back at past performance, but no-one has a time machine to go back to 2011 and make some better decisions, otherwise there would be quite a big queue to get in it.

The question is rather, will returns in the next 10 years look like the last? No-one can answer that with any accuracy. But perhaps we don’t have to, if we acknowledge that the last decade has not been just a weird statistical anomaly, because over 10 years it’s entirely normal to expect stock market returns to beat cash.

EXTRA REWARD FOR EXTRA RISK

That’s the extra reward stock market investors get for taking risk with their capital, and enduring its fluctuations. Since 2011 the scale of the difference between cash and stock market returns has been extreme, but the fact that equities have beaten cash is not unusual.

Today, remarkably, the base rate is even lower than it was 10 years ago, and the Bank of England is considering whether to cut it further, possibly taking it into negative territory for the first time. Despite that, money continues to accumulate in cash accounts thanks to lockdown decimating spending options. The issue of high levels of cash predates the pandemic though, as the financial regulator highlighted in December.

Their consumer research, which took place before the Covid crisis, found that around six million UK adults had investable assets of £10,000 or more, which were all held in cash. A further three million or so had more than three quarters of their assets in cash.

RATES CAN STAY LOW FOR LONGER THAN WE THINK

Here’s what the Financial Conduct Authority themselves said in December 2020: ‘Many consumers are still holding money in cash that could be invested to provide potentially higher returns, but they have not sought or received the help with their finances that would help them to make better investment decisions.’

The interest rate currently paid on cash doesn’t present a high bar to step over by any means. While there is some speculation that monetary and fiscal stimulus will lead to inflation and rates

will have to rise, if the last 10 years have taught us anything, it’s that interest rates can stay lower than we imagine, for, longer than we expect.

But for savers and investors, speculating over the course of future rates isn’t what should be driving decisions in the here and now. The question of whether to save in cash or invest in the stock market is actually relatively straightforward, it simply comes down to thinking about your finances in terms of short, medium, and long term pots.

For money that you might need in five years or less, cash is likely to be the main focus. For money that you might need in five to 10 years, you could consider putting at least some of it in the stock market.

For money that you won’t need for 10 years or more, you might consider investing a higher proportion, or even all of it, in the stock market. Savers may of course choose to take a more conservative approach by holding higher levels of cash, but they should then be comfortable that in the long run, this extra caution will likely come at a price.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Feature

First-time Investor

Great Ideas

Money Matters

News

- Amazon drops a bombshell during bumper US earnings season

- Pfizer sales boost puts vaccine economics under the spotlight

- Dr. Martens and Moonpig ‘pop’ on market debuts

- BP’s big challenge in funding its transition to renewable energy

- GameStop loses momentum but is the Reddit movement here to stay?

- What you need to know about changes to Bankers and Baillie Gifford European shares

- Marston’s fights takeover interest from US private equity firm