Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

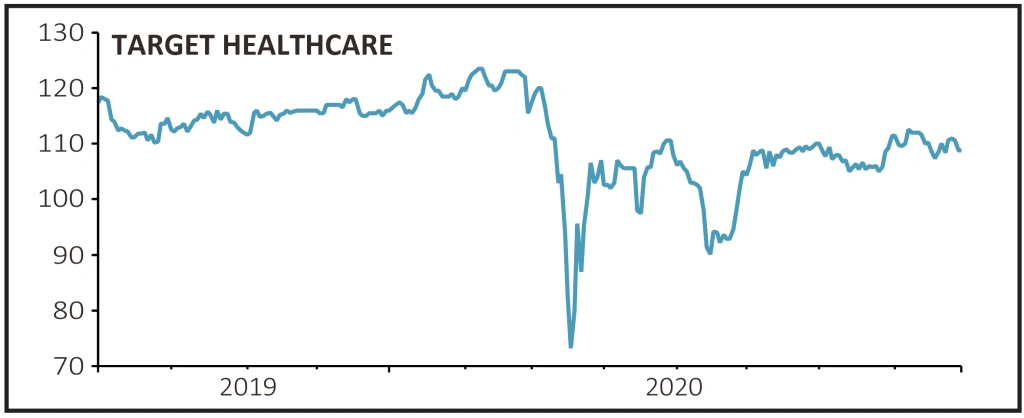

magazineTarget Healthcare has welcome news for income investors

Target Healthcare REIT (THRL) 112.8p

Gain to date: 5.6%

Original entry point: Buy at 106.8p, 16 July 2020

Care home investor Target Healthcare (THRL) is off to a decent start as one of our Great Ideas.

The shares have risen modestly, supported by a positive recent update (5 Aug) which revealed a slight increase in its net asset value per share from 108p at the end of March to 108.1p as at the end of June and robust rent collection.

Given we flagged the company’s income appeal in our initial article it was also pleasing to see the quarterly dividend nudged up by 1.5% to 1.67p per share.

On an annualised basis that would equate to a payout of 6.68p and a yield of 5.9% at the current share price.

Stockbroker Numis commented: ‘Target Healthcare’s continued robust performance reflects the defensive characteristics of the portfolio despite the care home sector featuring heavily in the news during the midst of the Covid-19 pandemic. The board has been able to maintain the dividend at the targeted level on the back of strong rent collection figures (96% for Q3 as at 6 July).’

SHARES SAYS: We continue to see Target Healthcare as a

relatively lower risk way of accessing a generous stream of income.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Saga white knight welcomed by investors

- SDL’s tie-up with RWS offers a compelling story

- Shock resignation of Japan PM hits Nikkei

- US markets flash warning signs with echoes of past corrections

- US Federal Reserve tweaks monetary policy goals

- Beauty website owner prepares for biggest London listing of 2020