Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineBuy remote IT connector Teamviewer for big growth potential

We recently looked at Europe and talked about some of the exciting growth companies on the Continent, and how they are often lost in the noise created by their US cousins. German technology company TeamViewer (TMV:XETRA) is exactly the type of fast-growing and profitable tech company that will have flown below the radar of most ordinary investors in recent months.

The German company has built a real-time remote connectivity platform that lets IT experts take control of devices (PCs, laptops, smartphones etc) to solve problems or to enable people to connect and collaborate from home, different office locations or anywhere, while the organisation maintains IT control.

During the lockdown this year, countless people around the world will have found themselves working from home and encountering IT problems. If you’ve ever had to call your work IT support team for help and had them take over your device virtually to find a fix, you may well have used TeamViewer, even if you didn’t know it.

15-YEAR HISTORY

TeamViewer was founded in 2005 and today sells its products and services in 180 countries.

Private equity firm Permira brought the company to the Frankfurt Stock Exchange in September 2019 with a €5.25 billion price tag, selling 42% of its stake to investors at €26.25 per share. Permira has continued to release shares into the market over the past year, leaving it with a 39% stake.

Several big tracker funds own TeamViewer stock while UK active funds with decent sized stakes include Rathbone Global Opportunities (B7FQLN1), Man GLG Continental European Growth (B011948), and BGF World Technology (B8KMZ39).

COVID WAKE-UP CALL

TeamViewer made a slow start on the stock market, but the Covid-19 pandemic has made investors suddenly appreciate the company’s digital growth potential. Since the virus low point in March the stock has gone bananas, more than doubling to a record €53.62 in early July. The stock remains more than 80% up since March at €44.93.

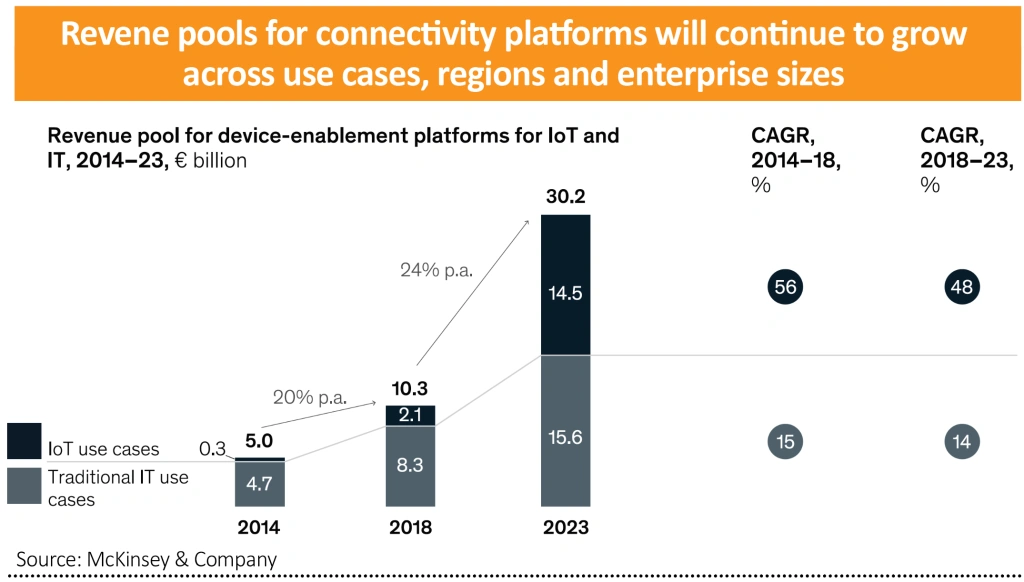

This is a very competitive space, with the likes of Microsoft, Citrix, LogMeIn and others, but the growth potential for connected devices in the coming Internet of Things (IoT) world is enormous and getting bigger. A McKinsey report estimates that the size of the remote connectivity platform market will triple by 2023 from €10 billion in 2018.

Analysts at Berenberg believe TeamViewer’s total addressable market will expand to €40 billion by 2023. This will be driven by the company widening its customer base, deepening its sales and marketing pool, and adding new tools around areas like augmented reality, such as its recent acquisition of Ubimax.

In short, the analysts think TeamViewer leads the way as the high-quality, large bandwidth, all-in-one platform to connect, manage and interact.

A study by independent global quality assurance company Qualitest found TeamViewer compatible with significantly more device types than peers, and the internet bandwidth scale to send large raw data files at significantly faster speeds.

This is an easily scalable business model that should throw off lots of free cash flow and expand profit margins as it grows.

Earnings before interest, tax, depreciation and amortisation (EBITDA) margins last year were 48.6% according to Refinitiv data, and consensus forecasts predict expansion to 56.4% by 2022, while Berenberg is even more optimistic.

This year, second quarter billings jumped 45% to €105.9 million while EBITDA shot up 60% to €57.3 million, with 534,000 subscribers.

This should provide the free cash flow to pay down borrowings fast and open the door for selective acquisitions to bolster annual growth predictions of 20% to 25%.

Berenberg anticipates net debt of €473 million at the end of 2020 will more than halve in 2021 to about €210 million. By the end of 2022 TeamViewer is expected to have nearly €140 million of net cash. Berenberg believes the stock is worth €61.

INVEST TO COMPETE

What could go wrong? For one, competition is thought to be particularly fierce, which could see churn rise.

There are also challenges from the big public cloud operators who package applications for clients. TeamViewer will need to keep investing to stay ahead of the pack.

And as cloud-based software provider itself, investors cannot rule out the threat that the platform becomes exposed to abuse by cybercriminals, changes to data privacy regulation and other IT infrastructure faults.

Any of these factors could potentially slow TeamViewer’s growth and potentially squeeze profit margins down the line. That could leave its highly rated stock exposed. The stock is trading on a 12-month forward price-to-earnings multiple twice the size of its software peer group at 52.5, according to Refinitiv data. But the PE drops quickly given an accelerating earnings profile.

SHARES SAYS: TeamViewer has many positive attributes and could prove to be a good solid long-term investment. The only caveat is investors must recognise the competition risks and appreciate they must pay a premium to own the stock.

It look like a quality business, with return on capital employed forecast to go from 20% in 2019 to 32.7% in 2021 and 41.9% in 2022, according to the consensus analyst forecast. Buy the shares.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Saga white knight welcomed by investors

- SDL’s tie-up with RWS offers a compelling story

- Shock resignation of Japan PM hits Nikkei

- US markets flash warning signs with echoes of past corrections

- US Federal Reserve tweaks monetary policy goals

- Beauty website owner prepares for biggest London listing of 2020