Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDebt and savings crisis looms in coronavirus lockdown

Research shows 20m Brits have already had to dip into their savings as a result of the crisis, after seeing their income hit.

A survey of 2,002 adults in the UK by AJ Bell shows that younger people have been hit the hardest, with more having to dip into their savings or take on debt just to make ends meets, when compared to older people.

SIGNIFICANT AGE DIVIDE

Overall 30% of people have had to use their savings to pay bills, rent and mortgage and other essentials so far in the crisis. But within this there is a significant age divide, with 44% of those aged 18 to 34 having to use their savings compared to 18% of those over the age of 55.

Many younger people work in industries that have been harder hit by the lockdown and business closures, such as retail, hospitality, the arts and freelance work.

Two-fifths of people have seen their finances hit in the current coronavirus crisis, with the most common reason being that they’ve been furloughed in their job – and so seen their income fall.

Of the 40% of people who have seen a drop in income, where people could pick more than one answer, just over a third say it’s because they’ve been furloughed while a fifth have had to take a pay cut.

A third of those who’ve seen their income hit say it’s because their income from investments or pensions have reduced, with men more likely to be affected by this than women – 40% of men say this has impacted them compared to 23% of women.

INCOME CHALLENGE AS DIVIDEND CUTS BITE

Another one in 10 people says they have reduced their pension withdrawals as a result of the crisis. Income payouts from companies have dropped, hitting income-seeking investors and those reliant on the income to fund their lifestyle, while market falls means people are wary of taking large capital sums from their pensions.

Almost two-fifths of people who’ve seen their income fall say they have seen their income cut as a result of being self-employed or owning their own business and have lost earnings as a result of the crisis, while 11% of people say they’ve lost their job. Another 4% say they have lost income due to other reasons, predominantly that their partner or spouse has seen their income fall.

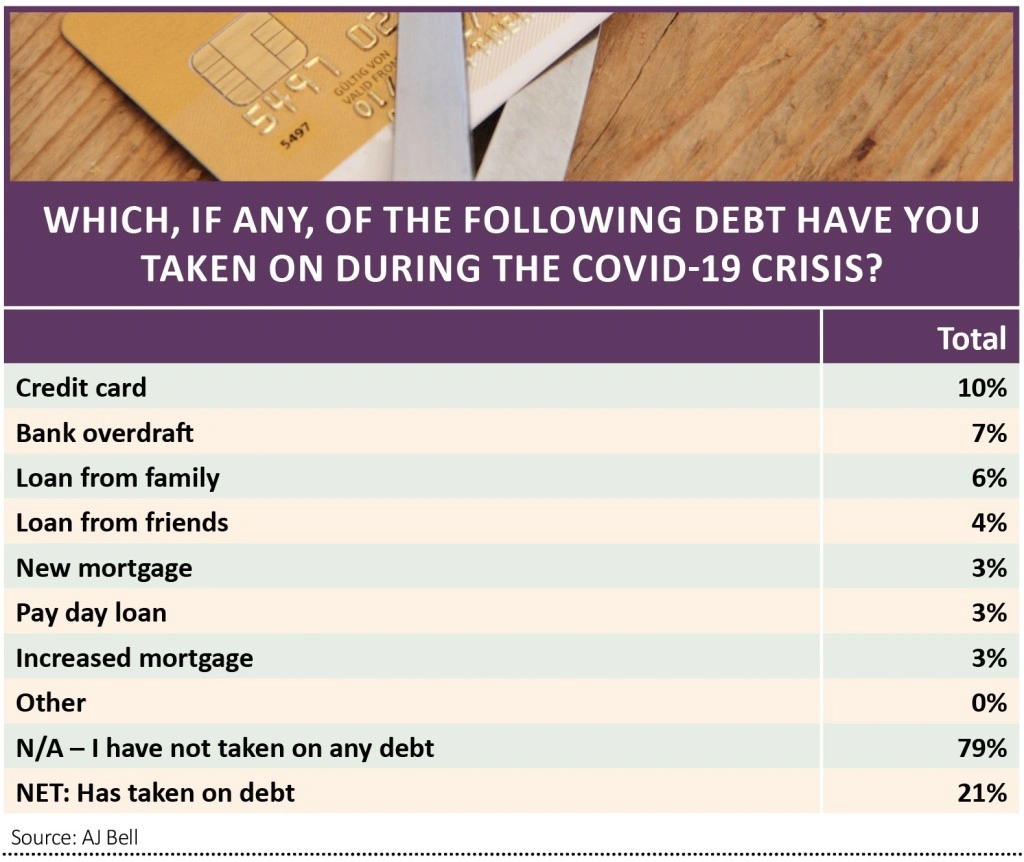

Lots of people don’t have money to fall back on should they see a drop in income. A large number of households have no emergency savings, meaning one fifth of the population has already taken on debt in order to pay their bills and for other essentials.

TURNING TO DEBT

So far 10% of people have put more debt on their credit cards, while another 10% have taken a loan from family or friends and 7% have taken on more overdraft debt. These figures are likely to soar in the coming months as people get their first reduced pay cheques since being furloughed and more people lose their job or see their incomes cut.

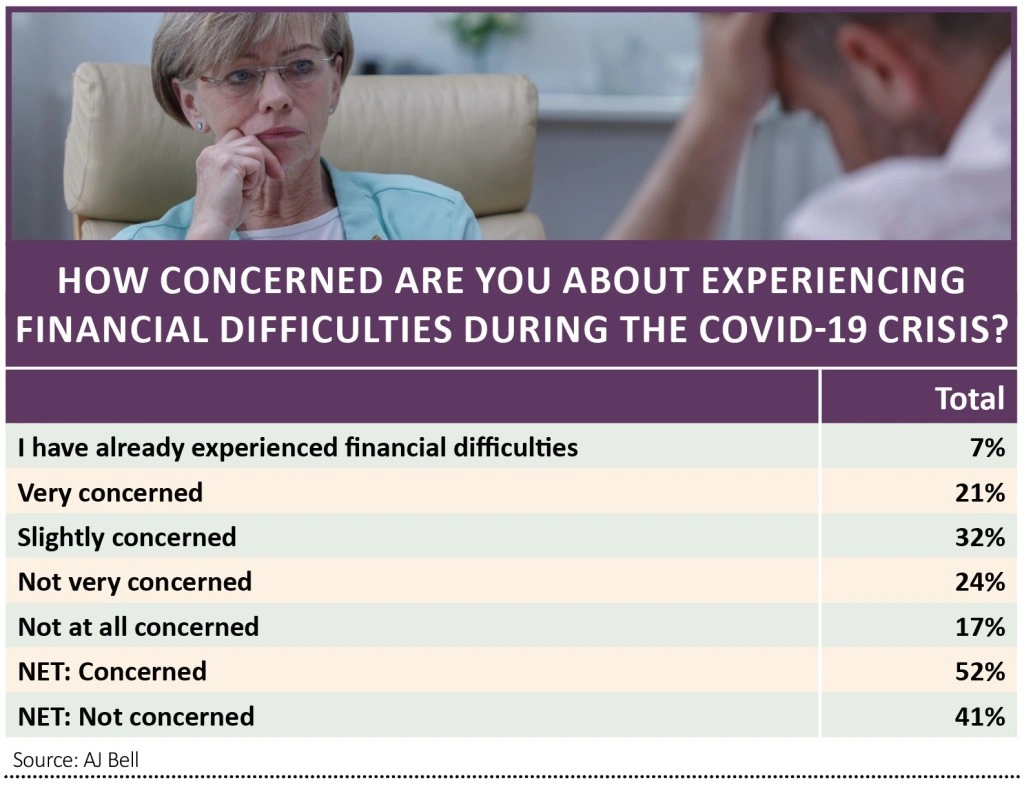

People are also braced for more financial hits as a result of the pandemic, suggesting that the numbers accessing their savings or taking on debt might rise. More than half of respondents say they are concerned about getting into financial difficulties in the current crisis, while more than a quarter have already seen a hit or are ‘very concerned’.

Again, younger people are more likely to be worried, as they tend to have lower savings to fall back on and are in more precarious job roles, with two-thirds of 18 to 34-year-olds saying they are worried about future financial difficulties compared to 35% of those aged 55 or over.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

Money Matters

News

- Exit charge lowered on Lifetime ISA as a temporary measure

- Companies will need to start quantifying Covid-19 impact

- Investors need to be prepared for terrible second quarter results

- Why these stocks have just hit all-time highs

- Orbis seeing ‘most exceptional discounts’ since the credit crunch

- Could we see a return of M&A due to the crisis?

- Berkshire Hathaway builds cash to record levels, sell airline stocks